TRUCKEE, CA--(Marketwire - May 6, 2010) - Clear Capital (www.clearcapital.com), a premium provider of data and solutions for real estate asset valuation, investment and risk assessment, today released its Home Data Index™ (HDI) Market Report. Patent pending rolling quarter technology significantly reduces the multi-month lag time associated with other indices to help investors, loan servicers and individual buyers and sellers make more informed, timely and profitable decisions.

Report highlights include:

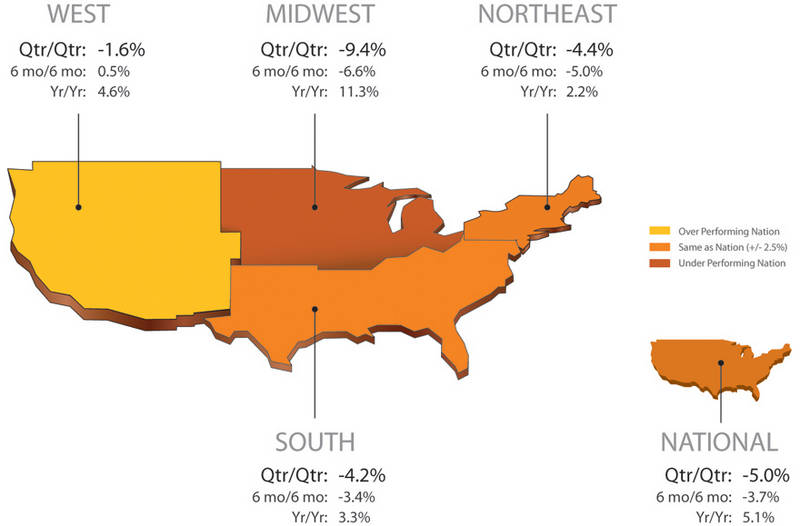

- National / Four Region Overview: All four regions see continued, yet slowing, declines in quarterly prices from last month; while the national year-over-year gains remain stable at 5.1 percent. The increase in the Nation's real estate owned (REO) saturation rate slowed in April, rising less than one percentage point to 29.6 percent.

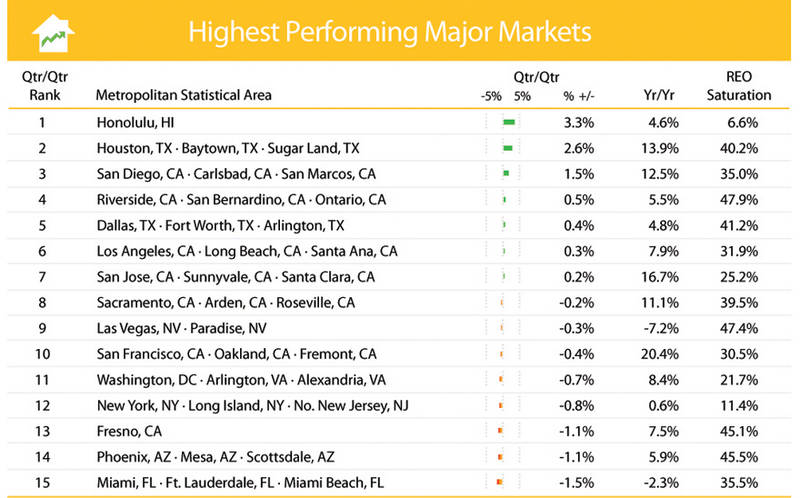

- Metropolitan Statistical Area (MSA) drilldown: The best performing markets manage to post positive gains in the face of tax credits that ended in April. Honolulu, Hawaii saw quarterly prices rise to 3.3 percent, pushing it to the number one position on the list this month. The 15 lowest performing markets post comparatively steep price declines -- averaging an -11.1 percent price change.

- Micro Market Analysis: Home prices in the District of Columbia area averaged a gain of 8.4 percent this past year -- ending a price decline of 42.8 percent since its peak in mid 2006. While the D.C. market as a whole have seen REO activity fall more than 17 percentage points since early 2009 to 21.7 percent, local micro markets have experienced dramatic variability in the timing of peak REO sales activity.

The Clear Capital HDI Market Report offers the industry, investors and lenders a timely look at pricing conditions, not only at the national and metropolitan level, but within local markets as well. Clear Capital data is built on the most recent data available from recorder/assessor offices, and then further enhanced by adding the Company's proprietary market data for the most comprehensive geographic coverage available.

"An interesting dynamic we're observing is the clear distinction between markets that are resilient to increased levels of bank owned properties and those which continue to be highly sensitive," said Dr. Alex Villacorta, Senior Statistician, Clear Capital.

"For example, the highest performing metro areas have seen prices remain relatively flat over the last quarter despite REO saturation rates averaging just above 33 percent. Contrast this with the lowest performing areas which have seen prices drop dramatically with average declines of more than 10 percent and average REO saturation rate less than those in the highest performing areas."

"This paradox suggests that price trends are not wholly dependent on distressed sale volume, and re-enforces the need to understand local market trends," added Villacorta.

National/Four Region Market Overview (April 2009 - April 2010)

Quarter-over-quarter home prices continue to slide across all four regions of the nation. Nationally, the 5.0 percent price decline represents a further 1.1 percentage point reduction from the quarterly decline reported last month. On a positive note, this is a marked slowdown in the rate of decline compared to the 3.9 percentage point drop seen between the reports released in early March and April of this year.

The falling quarterly prices are sufficient enough to halt the recent growth in year-over-year gains for the center regions of the nation. The Midwest reached an 11.3 percent gain for the year, down from last month's 12.8 percent. Similarly, the South (3.3%) is down from last month's 3.4 percent yearly gain. The two coastal regions, while maintaining quarterly declines, still managed to add to their yearly gains. The West (4.6%) added a 2.0 percent price increase, while the Northeast (2.2%) added 0.1 percent over last month.

Nationally, the 5.1 percent year-over-year price change remained unchanged from last month's report. The increase in the Nation's REO saturation rate slowed this month, rising less than one percentage point to 29.6 percent. These slowing trends indicate the recent and rapid deterioration in the housing market may have been short-lived, ending as spring draws near. However, even if quarterly price gains are experienced during this spring and summer, pressure will remain on the year-over-year comparisons as prices are compared relative to the price correction of mid-2009.

Metro Markets (April 2009 - April 2010)

Honolulu, Hawaii saw quarterly prices rise to 3.3 percent, pushing it to the number one position on the highest performing major markets list for this month's rolling quarter. The San Francisco, Calif. MSA continues to lead the group in yearly price gains (20.4%), while maintaining a nearly flat quarterly price change of -0.4 percent. Overall, the growth in the number of markets with quarterly price declines and increased REO saturation rates was slowed. Eight markets managed to improve their quarterly numbers over last month's report and twelve saw decreased REO saturation rates. Decreasing REO saturation is typically seen as a positive sign, in terms of price, as home sellers compete with fewer bank owned properties, which are frequently listed at a discount.

Year-over-year price gains continued to improve among the set, including a 5.0 percentage point price change in the Las Vegas, Nev. MSA -- the market with the largest yearly decline in the group. This leaves Las Vegas with a yearly price change of -7.2 percent. Overall, home prices in the highest performing markets have remained flat through the winter months, averaging quarterly gains of 0.2 percent, while yearly gains have averaged 7.4 percent.

If the federal tax credit from last fall is any indication, the end of the tax credit on April 30 suggests a let-down in home prices could follow in subsequent months. However, this timing coincides with the start of the spring home-buying season, providing reason to believe many of these markets will transition smoothly into the summer months. With REO sale volumes down nearly fifty percent from their peak in early 2009, and an expected springtime uptick in sale volumes at hand, there may be room in many of these markets to improve upon the minimal gains of winter.

With the best of the highest performing major markets only returning slight quarterly gains this winter, the lowest performing markets posted comparatively steep price declines. As a group, the fifteen markets on this month's list averaged a -11.1 percent price decline for the recent rolling quarter.

However, the short term picture for these markets has improved somewhat from last month, and while prices continue to fall, their drop is less dramatic than that of previous months. This provides an early indication that prices might be searching for a bottom, rather than starting a steeper decline, especially with the arrival of the spring buying season.

While quantifying the impact that increased sale volumes might have on prices is yet to be seen, it's clear that spring and summer mark the arrival of better conditions to the housing market, making it easier to move inventory. This is evident by increased sale volumes (averaging 30 percent off winter lows), throughout the steep declines of the last three years.

Compared to the highest performing major markets list which is largely made up of markets in the South and West regions, the lowest performing major markets are dominated by markets in the Midwest.

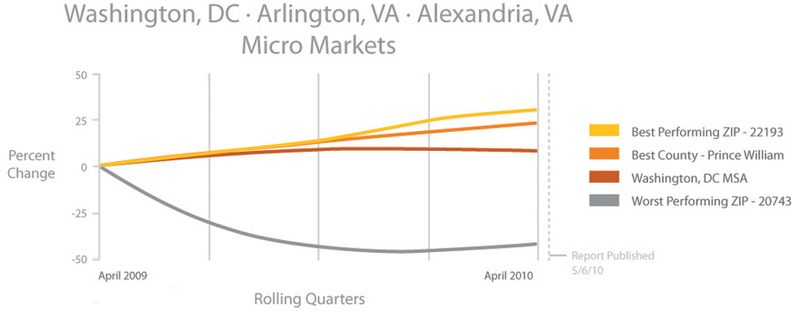

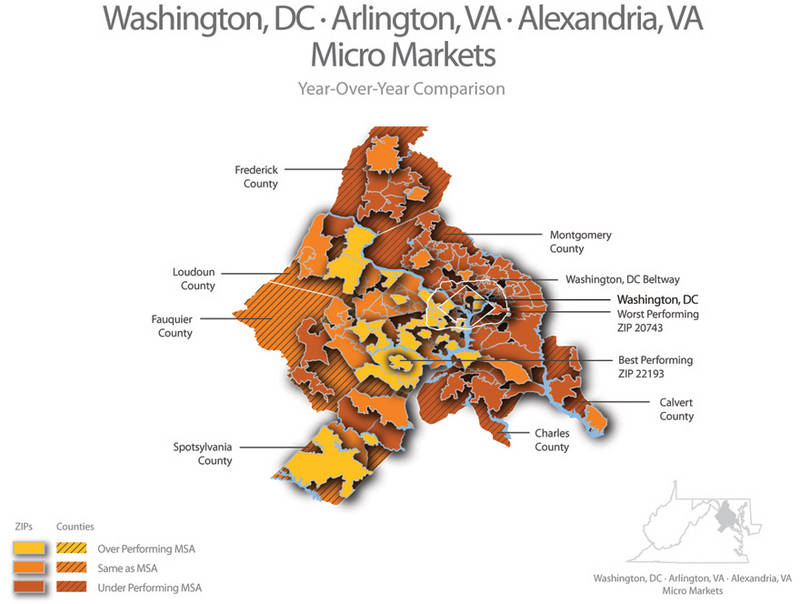

Micro Markets (April 2009 - April 2010)

This section highlights a single market every month with a deeper dive into how the micro- and macro-markets relate to each other.

Home prices in the District of Columbia (D.C.). area gained on average 8.4 percent over the last year. These gains ended what had been, by early 2009, a price decline of 42.8 percent since the market's peak in mid 2006. While the market as a whole has seen REO activity fall more than 17 percentage points from its peak of 39 percent in early 2009, local micro markets have experienced dramatic variability in the timing of peak REO sales activity -- and subsequently, price declines.

Following a steep run-up in prices that ended in the second quarter of 2006, the Woodbridge area near Dale City, Va. (ZIP code 22193) -- a suburb well south of the District -- saw prices fall 61.1 percent. Highly elevated REO activity, with nearly 60 percent of homes sold as bank owned, helped push prices to a bottom in early 2009. Since that time REO conditions have consistently improved (i.e. declined) with increasingly fast pick-up of bank owned properties. This rise in demand has helped push prices up 30.2 percent from their deep lows, representing the largest price gain in the metropolitan area for the year.

Just east of the District and inside the beltway, Capitol Heights, MD (ZIP code 20743) has seen home prices consistently lag the greater metropolitan area. Peak prices were not seen in this area until the third quarter of 2007, more than a year after the metropolitan area. Similarly, while the higher-priced Woodbridge area was experiencing declining REO activity by early 2009, Capitol Heights was on an opposite path with steadily growing REO saturation rates. Price declines in Capitol Heights didn't turn positive in this investor and rental-driven area until the price run-up of last fall, leaving the area with a yearly decline of 41.4 percent. With only a few months of price gains, REO saturation still near 60 percent and a longer foreclosure process in Maryland compared to Virginia, this market is positioned to continue to lag any recovery of the greater metropolitan area.

Clear Capital Home Data Index™ Methodology

The Clear Capital Home Data Index (HDI) provides weighted repeat sales, and price-per-square-foot index models that use multiple sale types, including single-family homes, multi-family homes and condominiums. These models are combined with an address-level cascade to provide sale-type-specific analysis for thousands of geographic areas across the country. The indices include both fair market and institutional (real estate owned) transactions. They also provide indicators of REO activity such as REO discount rates, REO days on market and REO saturation. The Clear Capital HDI generates indices in patent pending rolling quarter intervals that compare the most recent four months to the previous three months. The rolling quarters have no fixed start date and can be used to generate indices as data flows in, or at any arbitrary time period.

About Clear Capital

Clear Capital (www.clearcapital.com) is a premium provider of data and solutions for real estate asset valuation and risk assessment for large financial services companies. Our products include appraisals, broker-price opinions, property condition inspections, value reconciliations, and home data indices. Clear Capital's combination of progressive technology, high caliber in-house staff and a well-trained network of more than 40,000 field experts sets a new standard for accurate, up-to-date and well documented valuation data and assessments. The Company's customers include 75 percent of the largest U.S. banks, investment firms and other financial organizations.

Legend

Address Level Cascade - Provides the most granular market data available. From the subject property, progressively steps out from the smallest market to larger markets until data density and statistical confidence are sufficient to return a market trend.

Home Data Index (HDI) - Major intelligence offering that provides contextual data augmenting other, human-based valuation tools. Clear Capital's multi-model approach combines address-level accuracy with the most current proprietary home pricing data available.

Metropolitan Statistical Area (MSA) - Geographic entities defined by the U.S. Office of Management and Budget (OMB) for use by Federal statistical agencies in collecting, tabulating, and publishing Federal statistics.

Repeat Sales Model - Weighted linear model based on repeat sales of same property over time.

Price Per Square Foot (PPSF) Model - Median price movement of sale prices divided by square footage over a period of time -- most commonly a quarter.

Real Estate Owned (REO) Saturation - Calculates the percentage of REOs sold as compared to all properties sold in the last rolling quarter.

Rolling Quarters - Patent pending rolling quarters compare the most recent four months to the previous three months.

The information contained in this report is based on sources that are deemed to be reliable; however no representation or warranty is made as to the accuracy, completeness, or fitness for any particular purpose of any information contained herein. This report is not intended as investment advice, and should not be viewed as any guarantee of value, condition, or other attribute.

Contact Information:

Media Contact:

Michelle Sabolich

Atomic PR for Clear Capital

415.593.1400