CHICAGO, IL--(Marketwire - May 24, 2011) - A new TransUnion study revealed that consumers who only defaulted on their mortgage during the economic recession were far better risks than those consumers who went delinquent on multiple credit accounts, e.g. credit cards and auto loans. This was evident across all credit scoring ranges.

The results showed that consumers with mortgage-only defaults performed better on new loans than those with multiple delinquencies.

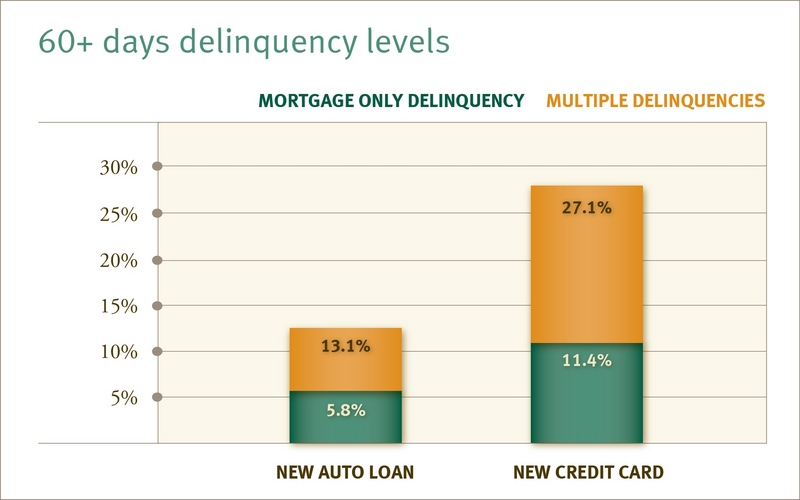

60+ days delinquency levels -- new auto loan:

- 5.8 percent -- mortgage-only delinquency

- 13.1 percent -- multiple delinquencies

60+ days delinquency levels -- new credit card:

- 11.4 percent -- mortgage-only delinquency

- 27.1 percent -- multiple delinquencies

The study did not find any strong evidence supporting the widely accepted "excess liquidity theory," which suggests consumers who stopped paying their mortgage loans during the recent recession had an increased cash flow in the short term, and therefore could repay other debts. In fact, consumers in the foreclosure process performed similarly, if not better, on certain accounts when they opened them further in the foreclosure process.

"There appears to be a pocket of opportunity among mortgage-only defaulters that is not the result of excess liquidity, but rather the unique circumstances of the recent recession," said Steve Chaouki, group vice president in TransUnion's financial services business unit. "This new market segment that the recession created is an important one for lenders to understand. They have the potential, today, to be stronger and more reliable customers."

Additional evidence suggesting the "excess liquidity theory" was not in effect during the recession was witnessed when comparing consumers who were 120 days past due on their mortgages, but opened new auto loans at various times after their delinquency. The percentage of consumers delinquent on those auto loans decreased as more time passed.

60+days delinquency levels

- Opened within six months -- 10.4 percent delinquent

- Opened within seven to 11 months -- 9.7 percent delinquent

- Opened 12 or more months later -- 9.3 percent delinquent

"This recession was unique in that certain consumers who defaulted on mortgages would otherwise be good credit risks. It appears their actions were driven more by difficult economic circumstances than by any inherent inability to manage debt," said Ezra Becker, vice president of research and consulting in TransUnion's financial services business unit. "Also, these results are well-aligned with our past research into the reversal of the payment hierarchy dynamic. Bottom line -- consumers prioritize their payments based on product preference when they find themselves constrained financially. In that sense, loan defaults have always been strategic."

A noteworthy exception was seen in credit cards where a slight increase in delinquencies occurred when consumers delayed the opening of the new tradeline. The delinquency changes were minimal between accounts opened seven to 11 months later (18.5 percent) and 12 or more months later (18.7 percent). "While we do not discount these results, we do not consider them conclusive given the remainder of the findings," said Chaouki.

"This study is critical in that it sheds more light on consumer behavior in a challenging economy," said Becker. "The analysis of consumer preferences between products and how they manage and prioritize them is important information lenders need to leverage to effectively manage their customer relationships. This study affords lenders greater insight into consumer performance, hopefully leading to a more mutually profitable, long-term relationship between lender and borrower."

Study Methodology:

The study reviewed data from a random sample of five million consumers with an open mortgage trade in January 2008. From this sample, TransUnion looked at a subset that had at least one non-mortgage trade open as of December 2007, went 120+ days delinquent on the mortgage trade between January 2008 and June 2009 and opened at least one additional trade after the mortgage went delinquent. This left the final sample size of approximately 129,000 new accounts for analysis. The sample was studied through a performance window of 12-17 months.

TransUnion evaluated the product mix of these consumers post-foreclosure, calculated each consumer's VantageScore in the month prior to the new tradeline opening and evaluated the delinquency rates of those new trades with 12-17 months of performance through August 2010.

About TransUnion

As a global leader in credit and information management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering comprehensive data and advanced analytics and decisioning. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion has employees in more than 25 countries on five continents.

www.transunion.com/business

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail

Telephone (312) 972-6646