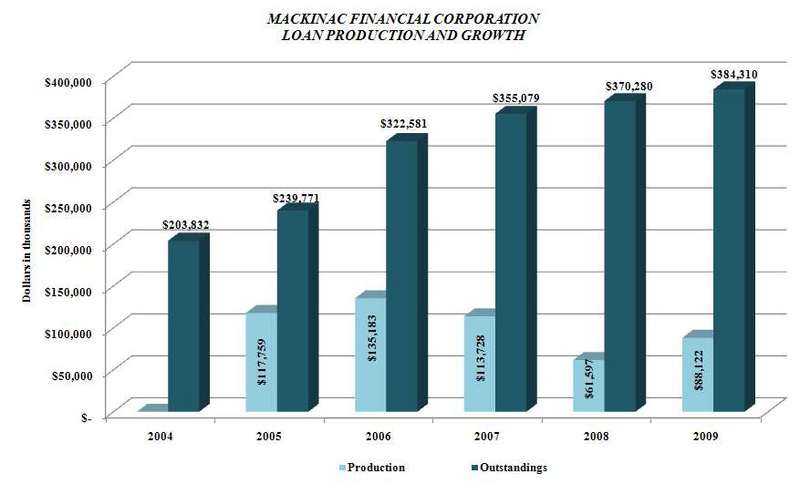

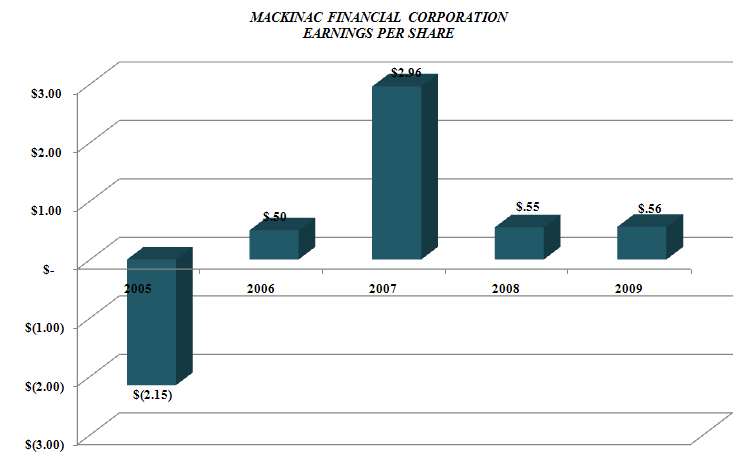

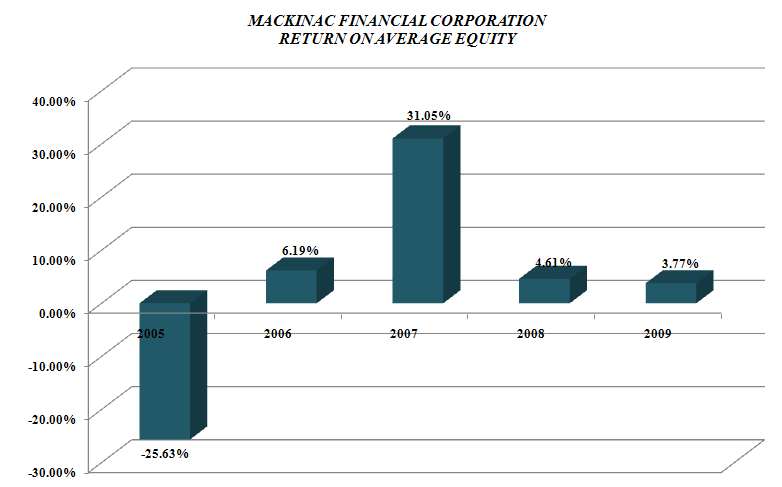

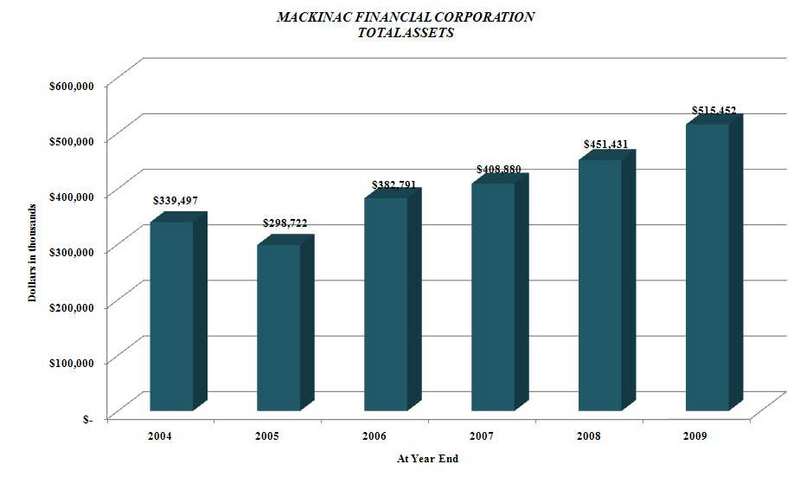

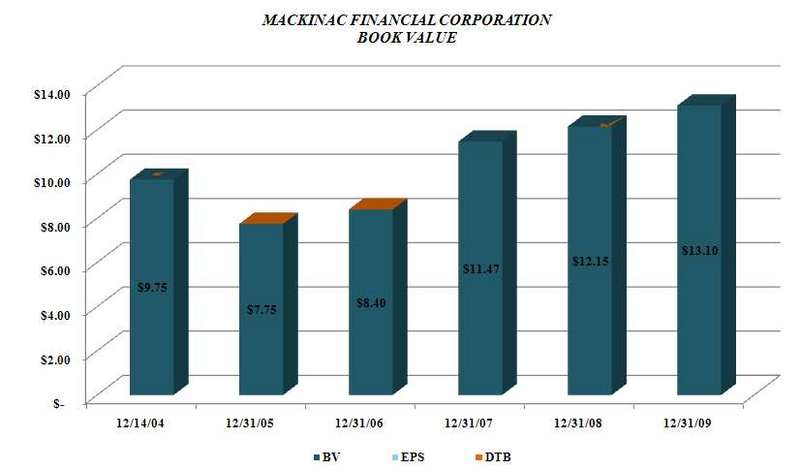

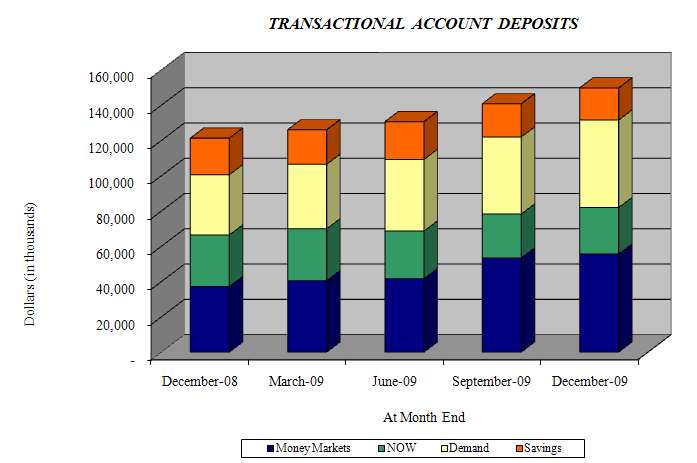

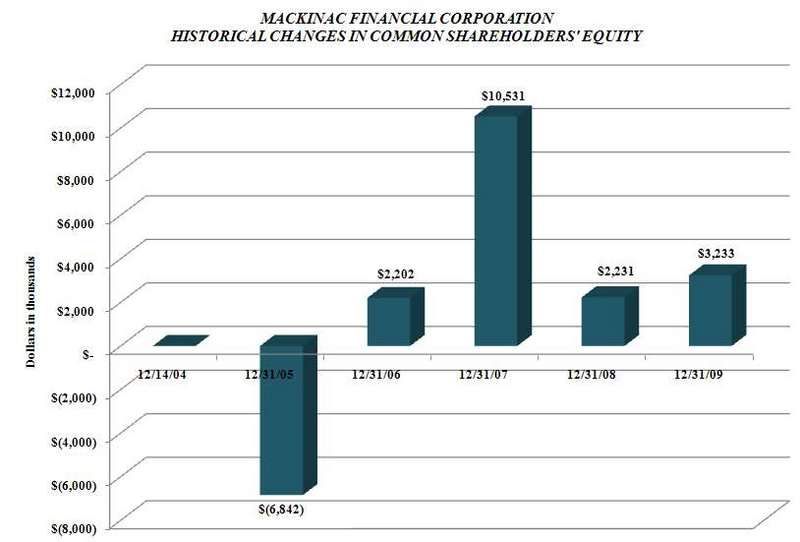

-- In 2009 book value per share increased by $.95 to $13.10. This marks the fourth consecutive year of increased shareholder value and a cumulative book value increase of $3.35 per share since the December 2004 recapitalization at $9.75 per share. -- We grew bank deposits by $26 million, net after the sale of two branch offices with $30 million in core deposits. We experienced deposit growth in all of our markets, with $26 million in Northern Lower Michigan, $20 million in Southeast Michigan and $10 million in the Upper Peninsula. Most of our 2009 deposit growth occurred in low cost transactional accounts which grew by $41 million. -- We continued to experience good loan demand with approximately $88 million of new loan production with a $14 million increase in loans outstanding, after reductions for amortization and payoffs. We were successful in producing loans in all of our markets but were less aggressive in Southeast Michigan where the recession is severe. Loan production totaled $44 million in the Upper Peninsula, $35 million in Northern Lower Michigan and $9 million in Southeast Michigan. -- In 2009 mBank was recognized as the top SBA loan originator in the Upper Peninsula with 27 SBA transactions, totaling $7.4 million. mBank totals equated to seventh overall for the State of Michigan with 36 transactions and $13.2 million. -- We improved our net interest margin from 3.20% in the fourth quarter of 2008 to 3.74% in 2009's fourth quarter. -- We continued to focus on enhancing our core earnings by controlling noninterest expense, increasing noninterest income and margin improvement. The combination of these three factors resulted in a decrease in our efficiency ratio from 86% in 2008 to 73% in 2009. -- We had an increase in nonperforming assets from $7 million at 2008 year end to $21 million at the end of 2009. Despite the appearance of this increase, we do not have systematic loan issues. The increase for 2009 included three large credit relationships totaling $10 million, for which we believe we are adequately reserved. The nonperforming assets by region are as follows; $13 million in Southeast Michigan, $6 million in Northern Lower Michigan and $2 million in the Upper Peninsula.Following is more detailed information concerning our 2009 results. We have also included, as a part of this release a "Five Year Overview" which illustrates the progress of MFNC in terms of key shareholder metrics, since the recapitalization which occurred in December 2004. As this overview depicts, throughout the national and state specific economic challenges over the past several years, we have continued to improve the core operating platform of MFNC. In April of 2009, the Corporation, in an abundance of caution, decided to participate in the TARP program and issued $11 million of preferred stock. In order to offset the cost of the preferred, we infused a portion of the TARP proceeds, $3 million, into the Bank and leveraged this excess capital by purchasing approximately $40 million of investment securities. We funded the purchase of these investments by issuing brokered deposits. In December, we began the process of deleveraging this position in anticipation of narrowing spreads and recognized a fourth quarter security gain of $.827 million. This strategy has resulted in overall security gains in excess of $1 million. The net income of $1.907 million, $.56 per share, along with an increase in the unrealized value of securities held for sale contributed to the 2009 overall increase in common shareholders' equity of $3.233 million, or 7.8%. Paul Tobias, Chairman of MFNC, commenting on the overall results for 2009, stated, "Although our results in 2009 were stymied by a worsening national economy and the severe deterioration that occurred in the automotive industry and Michigan real estate markets, we still made significant progress to increase our franchise value. We were able to absorb increases in loan loss provisions, FDIC insurance premiums, and costs associated with higher levels of nonperforming assets and still post an overall increase in common shareholders' equity which equated to $.95 per share." At 2009 year-end, the Corporation's loans stood at $384.310 million, an increase of $14.030 million, or 3.79%, from 2008 year-end balances of $370.280 million. Total loan originations in 2009 amounted to $88.122 million. Loan amortization and principal payoffs totaled $60.415 million. A good portion of these payoffs pertained to loan relationships that no longer met our pricing or credit standards. Loan growth was primarily from the Upper Peninsula markets where the economy is more stable. Total assets of the Corporation at December 31, 2009 were $515.377 million, an increase of $63.946 million, or 14.17% from total assets of $451.431 million reported at December 31, 2008. Total deposits grew from $371.097 million at December 31, 2008, to $421.389 million at December 31, 2009, an increase of $50.292 million, or 13.55%. This increase is composed of an increase in wholesale brokered deposits of $24.288 million and an increase in bank deposits of $26.004 million. During 2009, we increased investment securities which were funded primarily with wholesale deposits that were priced lower than in-market deposits. In August of 2009 we completed the sale of $30 million in deposits including the bank facilities of two branch offices in Upper Michigan which resulted in a $1.208 million gain. Kelly George, President and Chief Executive Officer of mBank, commenting on the deposit growth and branch sales, stated, "The sale of these branches tightened up our existing footprint in the Upper Peninsula and will allow us to concentrate on markets with higher growth potential, in addition to enabling the Corporation to strategically transition the Bank's footprint into 'commercial hubs' of the Upper Peninsula to better allocate personnel resources and management time. We continue to focus our efforts on growing transactional accounts and were successful in growing demand, money market and NOW accounts in total from $121.413 million at 2008 year-end to $149.875 million at 2009 year-end." Net interest income for the year ended December 31, 2009 was $16.287 million compared to $12.864 million for the year ended December 31, 2008, an increase of $3.423 million. The margin percentage for 2009 was 3.59% compared to 3.23% in 2008 and 3.60% in 2007. We recognize the importance of cost control, especially in times of economic slowdown. In 2009 our total noninterest expense was $13.802 million compared to $12.558 million in 2008 and $12.100 million in 2007. The increase in 2009 was primarily attributable to costs associated with higher levels of nonperforming assets and increased FDIC insurance premiums. Salaries and benefits were reduced from $6.886 million in 2008 to $6.583 million in 2009. Nonperforming assets increased in 2009 as the economy continued to weaken, especially in Southeast Michigan. Nonperforming loans totaled $15.237 million, or 3.96% of total loans at December 31, 2009. Nonperforming assets at December 31, 2009 were $21.041 million, 4.08% of total assets, compared to $7.076 million or 1.57% of total assets at December 31, 2008. Kelly George commented, "The elevated level of nonperforming assets, while still below peers and manageable, does concern us given the challenges throughout the state. We do not have a systematic problem with our overall loan portfolio, with over 58%, $8.8 million, of our problem loans stemming from two credit relationships in Southeast Michigan that we continue to devote significant attention to in order to reduce nonperformers in a timely manner and with minimal income statement impact. In retrospect, these large loans appeared sound and adequately collateralized at inception; however, as the economy worsened and real estate values declined, the borrowers have not been able to weather the storm. This in turn has led to a very cautious approach in all markets, but particularly in Southeast Michigan, which includes an emphasis on smaller loans and very conservative collateral valuations. We continue to focus on early identification and resolution of all our problem credits to minimize carrying costs, collateral deterioration and incremental loss." Shareholders' equity totaled $55.299 million at December 31, 2009, compared to $41.552 million at the end of 2008, an increase of $13.747 million. This increase includes $10.5 million of preferred stock that was issued by MFNC as a TARP recipient, consolidated net income of $1.907 million, the capital contribution impact of stock options and also the increase in equity due to the increase in the market value of held-for-sale investments, which amounted to $.648 million. Mr. Tobias concluded, "We will continue to consider all business combination options that would create shareholder value, but we have built our business plan on resolving the existing asset quality problems, building core deposits and managing costs. We believe that our book value growth has been significant and franchise value will be recognized by the market when the perception of Michigan and the confidence in the asset quality component of banking improves." Mackinac Financial Corporation is a registered bank holding company formed under the Bank Holding Company Act of 1956 with assets in excess of $500 million and whose common stock is traded on the NASDAQ stock market as "MFNC." The principal subsidiary of the Corporation is mBank. Headquartered in Manistique, Michigan, mBank has 10 branch locations; six in the Upper Peninsula, three in the Northern Lower Peninsula and one in Oakland County, Michigan. The Company's banking services include commercial lending and treasury management products and services geared toward small to mid-sized businesses, as well as a full array of personal and business deposit products and consumer loans. Forward-Looking Statements This release contains certain forward-looking statements. Words such as "anticipates," "believes," "estimates," "expects," "intends," "should," "will," and variations of such words and similar expressions are intended to identify forward-looking statements: as defined by the Private Securities Litigation Reform Act of 1995. These statements reflect management's current beliefs as to expected outcomes of future events and are not guarantees of future performance. These statements involve certain risks, uncertainties and assumptions that are difficult to predict with regard to timing, extent, likelihood, and degree of occurrence. Therefore, actual results and outcomes may materially differ from what may be expressed or forecasted in such forward-looking statements. Factors that could cause a difference include among others: changes in the national and local economies or market conditions; changes in interest rates and banking regulations; the impact of competition from traditional or new sources; and the possibility that anticipated cost savings and revenue enhancements from mergers and acquisitions, bank consolidations, branch closings and other sources may not be fully realized at all or within specified time frames as well as other risks and uncertainties including but not limited to those detailed from time to time in filings of the Company with the Securities and Exchange Commission. These and other factors may cause decisions and actual results to differ materially from current expectations. Mackinac Financial Corporation undertakes no obligation to revise, update, or clarify forward-looking statements to reflect events or conditions after the date of this release.

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

SELECTED FINANCIAL HIGHLIGHTS

For The Years Ended

December 31,

(Dollars in thousands, except per share data) 2009 2008

------------ ------------

(Unaudited) (Unaudited)

Selected Financial Condition Data (at end of

period):

Assets $ 515,377 $ 451,431

Loans 384,310 370,280

Investment securities 46,513 47,490

Deposits 421,389 371,097

Borrowings 36,140 36,210

Shareholders' equity 55,299 41,552

Selected Statements of Income Data:

Net interest income $ 16,287 $ 12,864

Income before taxes and preferred dividend 3,535 2,659

Net income 1,907 1,872

Income per common share - Basic .56 .55

Income per common share - Diluted .56 .55

Weighted average shares outstanding 3,419,736 3,422,012

Selected Financial Ratios and Other Data:

Performance Ratios:

Net interest margin 3.59% 3.23%

Efficiency ratio 73.37 85.51

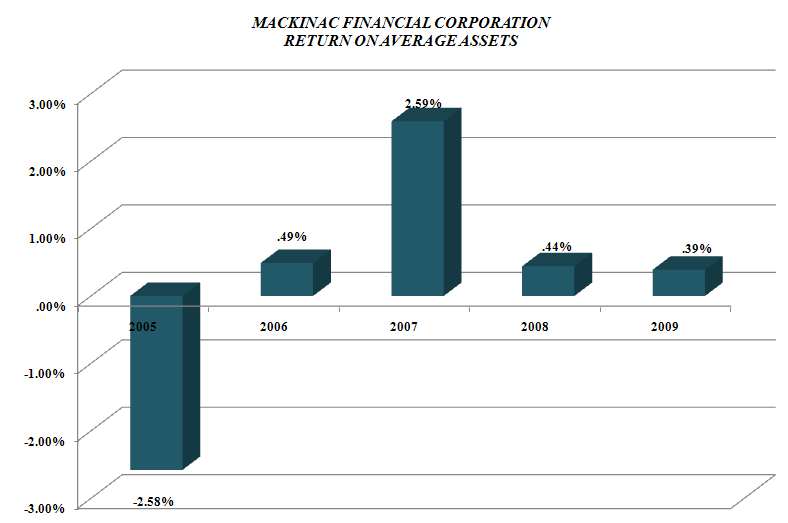

Return on average assets .39 .44

Return on average equity 3.77 4.61

Average total assets $ 493,652 $ 425,343

Average total shareholders' equity 50,531 40,630

Average loans to average deposits ratio 92.99% 105.61%

Common Share Data at end of period:

Market price per common share $ 4.64 $ 4.40

Book value per common share $ 13.10 $ 12.15

Common shares outstanding 3,419,736 3,419,736

Other Data at end of period:

Allowance for loan losses $ 5,225 $ 4,277

Non-performing assets $ 21,041 $ 7,076

Allowance for loan losses to total loans 1.36% 1.16%

Non-performing assets to total assets 4.08% 1.57%

Number of:

Branch locations 10 12

FTE Employees 100 100

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

December 31, December 31,

(Dollars in thousands) 2009 2008

------------- -------------

(unaudited) (audited)

ASSETS

Cash and due from banks $ 18,433 $ 10,112

Federal funds sold 27,000 -

------------- -------------

Cash and cash equivalents 45,433 10,112

Interest-bearing deposits in other financial

institutions 678 582

Securities available for sale 46,513 47,490

Federal Home Loan Bank stock 3,794 3,794

Loans:

Commercial 305,670 296,088

Mortgage 74,350 70,447

Installment 4,290 3,745

------------- -------------

Total Loans 384,310 370,280

Allowance for loan losses (5,225) (4,277)

------------- -------------

Net loans 379,085 366,003

Premises and equipment 10,165 11,189

Other real estate held for sale 5,804 2,189

Other assets 23,905 10,072

------------- -------------

TOTAL ASSETS $ 515,377 $ 451,431

============= =============

LIABILITIES AND SHAREHOLDERS' EQUITY

Liabilities:

Non-interest-bearing deposits $ 35,878 $ 30,099

Interest-bearing deposits:

NOW, Money Market, Checking 95,790 70,584

Savings 18,207 20,730

CDs < $100,000 59,953 73,752

CDs > $100,000 36,385 25,044

Brokered 175,176 150,888

------------- -------------

Total deposits 421,389 371,097

Borrowings:

Federal funds purchased - -

Short-term 15,000 -

Long-term 21,140 36,210

------------- -------------

Total borrowings 36,140 36,210

Other liabilities 2,549 2,572

------------- -------------

Total liabilities 460,078 409,879

Shareholders' equity:

Preferred stock - No par value:

Authorized 500,000 shares, no shares

outstanding 10,514 -

Common stock and additional paid in

capital - No par value

Authorized - 18,000,000 shares

Issued and outstanding - 3,419,736

shares 43,494 42,815

Accumulated deficit 198 (1,708)

Accumulated other comprehensive income

(loss) 1,093 445

------------- -------------

Total shareholders' equity 55,299 41,552

------------- -------------

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY $ 515,377 $ 451,431

============= =============

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in thousands, except per

share data) For The Years Ended December 31,

2009 2008 2007

----------- ----------- ----------

INTEREST INCOME: (unaudited) (audited) (audited)

Interest and fees on loans:

Taxable $ 20,521 $ 22,555 $ 26,340

Tax-exempt 292 404 533

Interest on securities:

Taxable 2,783 1,293 1,100

Tax-exempt 19 5 -

Other interest income 93 305 722

----------- ----------- ----------

Total interest income 23,708 24,562 28,695

----------- ----------- ----------

INTEREST EXPENSE:

Deposits 6,431 10,115 13,224

Borrowings 990 1,583 2,054

----------- ----------- ----------

Total interest expense 7,421 11,698 15,278

----------- ----------- ----------

Net interest income 16,287 12,864 13,417

Provision for loan losses 3,700 2,300 400

----------- ----------- ----------

Net interest income after provision

for loan losses 12,587 10,564 13,017

----------- ----------- ----------

OTHER INCOME:

Service fees 1,023 838 688

Net security gains 1,471 64 (1)

Net gains on sale of secondary

market loans 830 120 498

Proceeds from settlement of

lawsuits - 3,475 470

Other 1,427 156 351

----------- ----------- ----------

Total other income 4,751 4,653 2,006

----------- ----------- ----------

OTHER EXPENSES:

Salaries and employee benefits 6,583 6,886 6,757

Occupancy 1,385 1,374 1,272

Furniture and equipment 805 771 678

Data processing 862 844 785

Professional service fees 603 508 532

Loan and deposit 1,772 569 285

Telephone 187 170 228

Advertising 322 305 370

Other 1,283 1,131 1,193

----------- ----------- ----------

Total other expenses 13,802 12,558 12,100

----------- ----------- ----------

Income before provision for income

taxes 3,536 2,659 2,923

Provision for (benefit of) income

taxes 1,120 787 (7,240)

----------- ----------- ----------

----------- ----------- ----------

NET INCOME $ 2,416 $ 1,872 $ 10,163

----------- ----------- ----------

Preferred dividend expense 509 - -

----------- ----------- ----------

NET INCOME AVAILABLE TO COMMON

SHAREHOLDERS $ 1,907 $ 1,872 $ 10,163

=========== =========== ==========

INCOME PER COMMON SHARE

Basic $ .56 $ .55 $ 2.96

=========== =========== ==========

Diluted $ .56 $ .55 $ 2.96

=========== =========== ==========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

LOAN PORTFOLIO AND CREDIT QUALITY

(Dollars in thousands)

Loan Portfolio Balances (at end of period):

December 31, December 31,

2009 2008

------------- -------------

(unaudited) (unaudited)

Commercial Loans:

Real estate - operators of nonresidential

buildings $ 48,689 $ 41,299

Hospitality and tourism 45,315 35,086

Real estate agents and managers 24,242 29,292

Operators of nonresidential buildings 12,619 13,467

Other 150,214 145,831

------------- -------------

Total Commercial Loans 281,079 264,975

1-4 family residential real estate 67,232 65,595

Consumer 4,290 3,745

Construction

Commercial 24,591 31,113

Consumer 7,118 4,852

------------- -------------

Total Loans $ 384,310 $ 370,280

============= =============

Credit Quality (at end of period):

December 31, December 31,

2009 2008

------------ ------------

(unaudited) (unaudited)

Nonperforming Assets :

Nonaccrual loans $ 14,368 $ 4,887

Loans past due 90 days or more - -

Restructured loans 869

------------ ------------

Total nonperforming loans 15,237 4,887

Other real estate owned 5,804 2,189

------------ ------------

Total nonperforming assets $ 21,041 $ 7,076

============ ============

Nonperforming loans as a % of loans 3.96% 1.32%

------------ ------------

Nonperforming assets as a % of assets 4.08% 1.57%

------------ ------------

Reserve for Loan Losses:

At period end $ 5,225 $ 4,277

------------ ------------

As a % of average loans 1.39% 1.18%

------------ ------------

As a % of nonperforming loans 34.29% 87.52%

------------ ------------

As a % of nonaccrual loans 36.37% 87.52%

============ ============

Charge-off Information (year to date):

Average loans $ 374,796 $ 361,324

------------ ------------

Net charge-offs $ 2,752 $ 2,169

------------ ------------

Charge-offs as a % of average loans .73% .60%

------------ ------------

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

QUARTERLY FINANCIAL HIGHLIGHTS

QUARTER ENDED

-----------------------------------------------------

(Unaudited)

-----------------------------------------------------

December September June March December

31, 30, 30, 31, 31,

2009 2009 2009 2009 2008

--------- --------- --------- --------- ----------

BALANCE SHEET

(Dollars in

thousands)

Total loans $ 384,310 $ 384,100 $ 372,004 $ 370,776 $ 370,280

Allowance for loan

losses (5,225) (4,081) (4,119) (4,793) (4,277)

--------- --------- --------- --------- ----------

Total loans, net 379,085 380,019 367,885 365,983 366,003

Intangible assets - - 6 26 46

Total assets 515,377 513,180 506,304 466,375 451,431

Core deposits 209,828 200,541 202,892 196,860 195,165

Noncore

deposits (1) 211,561 218,040 210,260 188,897 175,932

--------- --------- --------- --------- ----------

Total deposits 421,389 418,581 413,152 385,757 371,097

Total borrowings 36,140 36,140 36,210 36,210 36,210

Total shareholders'

equity 55,299 55,766 53,939 41,864 41,552

Total shares

outstanding 3,419,736 3,419,736 3,419,736 3,419,736 3,419,736

AVERAGE BALANCES

(Dollars in

thousands)

Assets $ 514,102 $ 513,687 $ 491,205 $ 454,740 $ 441,583

Loans 386,203 370,310 371,609 370,943 366,077

Deposits 418,280 419,102 401,510 372,669 358,213

Equity 55,665 54,594 49,855 41,813 41,516

INCOME STATEMENT

(Dollars in

thousands)

Net interest

income $ 4,431 $ 4,310 $ 4,051 $ 3,495 $ 3,330

Provision for loan

losses 2,300 700 150 550 1,100

--------- --------- --------- --------- ----------

Net interest

income after

provision 2,131 3,610 3,901 2,945 2,230

Total noninterest

income 1,503 2,418 439 391 308

Total noninterest

expense 3,650 3,443 3,470 3,239 2,961

--------- --------- --------- --------- ----------

Income before taxes (16) 2,585 870 97 (423)

Provision for

income taxes (22) 864 271 7 (171)

--------- --------- --------- --------- ----------

Net income 6 1,721 599 90 (252)

--------- --------- --------- --------- ----------

Preferred dividend

expense 186 185 138 - -

--------- --------- --------- --------- ----------

Net income

available to

common

shareholders $ (180) $ 1,536 $ 461 $ 90 $ (252)

========= ========= ========= ========= ==========

PER SHARE DATA

Earnings $ (.05) $ .45 $ .13 $ .03 $ (.07)

Book value per

common share 13.10 13.25 12.73 12.24 12.15

Market value,

closing price 4.64 4.10 4.50 4.00 4.40

ASSET QUALITY

RATIOS

Nonperforming

loans/total loans 3.96% 3.00% 2.66% 3.52% 1.32%

Nonperforming

assets/total

assets 4.08 3.38 2.93 3.27 1.57

Allowance for loan

losses/total loans 1.36 1.06 1.11 1.29 1.16

Allowance for loan

losses/nonperform-

ing loans 34.29 35.40 41.71 36.72 87.52

PROFITABILITY

RATIOS

Return on average

assets (.14)% 1.19% .38% .08% (.23)%

Return on average

equity (1.28) 11.16 3.71 .87 (2.42)

Net interest margin 3.74 3.66 3.58 3.35 3.20

Efficiency ratio 71.03 70.09 76.55 82.36 80.30

Average

loans/average

deposits 92.33 88.36 92.55 99.54 102.20

CAPITAL ADEQUACY

RATIOS

Tier 1 leverage

ratio 9.75% 9.74% 9.65% 7.86% 8.01%

Tier 1 capital to

risk weighted

assets 11.92 12.18 11.94 9.31 9.25

Total capital to

risk weighted

assets 13.17 13.19 13.00 10.56 10.38

Average

equity/average

assets 10.83 10.63 10.15 9.19 9.40

Tangible

equity/tangible

assets 10.83 10.87 10.65 8.97 9.20

(1) Noncore deposits includes Internet CDs, brokered deposits and CDs

greater than $100,000

Contact Information: Contact: Investor Relations (888) 343-8147 Website: www.bankmbank.com