MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

SELECTED FINANCIAL HIGHLIGHTS

For The Years Ended

December 31,

(Dollars in thousands,except per share data) 2007 2006

----------- -----------

(Unaudited) (Audited)

Selected Financial Condition Data (at end of

period):

Total assets $ 408,880 $ 382,791

Total loans 355,079 322,581

Total deposits 320,827 312,421

Borrowings and subordinated debentures 45,949 38,307

Total shareholders' equity 39,321 28,790

Selected Statements of Income Data:

Net interest income $ 13,417 $ 11,593

Income before taxes 2,923 1,216

Net income 10,163 1,716

Income per common share - Basic 2.96 .50

Income per common share - Diluted 2.96 .50

Selected Financial Ratios and Other Data:

Performance Ratios:

Net interest margin 3.60% 3.51%

Efficiency ratio 79.46 93.95

Return on average assets 2.59 .49

Return on average equity 31.05 6.19

Average total assets $ 392,313 $ 347,927

Average total shareholders' equity 32,731 27,744

Average loans to average deposits ratio 104.94% 99.77%

Common Share Data at end of period:

Market price per common share $ 8.98 $ 11.50

Book value per common share $ 11.47 $ 8.40

Common shares outstanding 3,428,695 3,428,695

Weighted average shares outstanding 3,428,695 3,428,695

Other Data at end of period:

Allowance for loan losses $ 4,146 $ 5,006

Non-performing assets $ 5,234 $ 2,965

Allowance for loan losses to total loans 1.17% 1.55%

Non-performing assets to total assets 1.28% .77%

Number of:

Branch locations 12 13

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in thousands, except per share data) December 31,

2007 2006

----------- -----------

(Unaudited) (Audited)

ASSETS

Cash and due from banks $ 6,196 $ 4,865

Federal funds sold 166 5,841

----------- -----------

Cash and cash equivalents 6,362 10,706

Interest-bearing deposits in other financial

institutions 1,810 856

Securities available for sale 21,597 32,769

Federal Home Loan Bank stock 3,794 3,794

Loans:

Commercial 288,839 255,780

Mortgage 62,703 63,960

Installment 3,537 2,841

----------- -----------

Total loans 355,079 322,581

Allowance for loan losses (4,146) (5,006)

----------- -----------

Net loans 350,933 317,575

Premises and equipment 11,609 12,453

Other real estate held for sale 1,226 26

Other assets 11,549 4,612

----------- -----------

TOTAL ASSETS $ 408,880 $ 382,791

=========== ===========

LIABILITIES AND SHAREHOLDERS' EQUITY

Liabilities:

Non-interest-bearing deposits $ 25,557 $ 23,471

Interest-bearing deposits

NOW and Money Market 81,160 73,188

Savings 12,485 13,365

CDs < $100,000 80,607 89,585

CDs > $100,000 22,355 23,645

Brokered 98,663 89,167

----------- -----------

Total deposits 320,827 312,421

Borrowings

Short-term 7,710

Long-term 38,239 38,307

Other liabilities 2,783 3,273

----------- -----------

Total liabilities 369,559 354,001

Shareholders' equity:

Preferred stock - No par value:

Authorized 500,000 shares, no shares

outstanding - -

Common stock and additional paid in capital -

No par value

Authorized - 18,000,000 shares Issued and

outstanding - 3,428,695 shares 42,841 42,722

Retained earnings (3,580) (13,745)

Accumulated other comprehensive income (loss) 60 (187)

----------- -----------

Total shareholders' equity 39,321 28,790

----------- -----------

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY $ 408,880 $ 382,791

=========== ===========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in thousands, except per

share data) For The Years Ended December 31,

2007 2006 2005

----------- ----------- -----------

Interest income: (Unaudited) (Audited) (Audited)

Interest and fees on loans:

Taxable $ 26,340 $ 21,239 $ 13,862

Tax-exempt 533 753 928

Interest on securities:

Taxable 1,100 1,186 1,455

Tax-exempt - 87 167

Other interest income 722 787 564

----------- ----------- -----------

Total interest income 28,695 24,052 16,976

----------- ----------- -----------

Interest expense:

Deposits 13,224 10,575 5,259

Borrowings 2,054 1,884 1,937

----------- ----------- -----------

Total interest expense 15,278 12,459 7,196

----------- ----------- -----------

Net interest income 13,417 11,593 9,780

Provision for loan losses 400 (861) -

----------- ----------- -----------

Net interest income after provision

for loan losses 13,017 12,454 9,780

----------- ----------- -----------

Other income

Service fees 688 547 586

Net gains on sale of secondary

market loans 498 197 49

Proceeds from settlement of

lawsuit 470 - -

Other 350 239 476

----------- ----------- -----------

Total other income 2,006 983 1,111

----------- ----------- -----------

Other expenses:

Salaries and employee benefits 6,757 6,132 6,090

Occupancy 1,272 1,264 1,053

Furniture and equipment 678 631 560

Data processing 785 691 1,720

Accounting, legal and consulting

fees 532 1,425 886

Loan and deposit 285 392 852

Telephone 228 210 271

Advertising 370 346 814

Penalty on prepayment of FHLB

borrowings - - 4,320

Other 1,193 1,130 1,689

----------- ----------- -----------

Total other expenses 12,100 12,221 18,255

----------- ----------- -----------

Income (loss) before provision for

income taxes 2,923 1,216 (7,364)

Provision for (benefit of) income

taxes (7,240) (500) -

----------- ----------- -----------

Net income (loss) $ 10,163 $ 1,716 $ (7,364)

----------- ----------- -----------

Income (loss) per common share:

Basic $ 2.96 $ .50 $ (2.15)

=========== =========== ===========

Diluted $ 2.96 $ .50 $ (2.15)

=========== =========== ===========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

LOAN PORTFOLIO AND CREDIT QUALITY

(Dollars in thousands)

Loan Portfolio Balances (at end of period):

December 31,

2007 2006

----------- -----------

Commercial Loans

Real estate - operators of nonresidential buildings $ 41,597 $ 44,308

Hospitality and tourism 37,604 30,826

Real estate agents and managers 29,571 25,071

New car dealers 10,569 10,086

Other 130,546 115,426

----------- -----------

Total Commercial Loans 249,887 225,717

1-4 family residential real estate 57,613 58,014

Consumer 3,537 2,841

Construction

Consumer 5,090 5,946

Commercial 38,952 30,063

----------- -----------

Total Loans $ 355,079 $ 322,581

=========== ===========

Credit Quality (at end of period):

December 31,

2007 2006

----------- ----------

Nonperforming Assets

Nonaccrual loans (1) $ 3,298 $ 2,899

Loans past due 90 days or more 710 40

---------- ----------

Total nonperforming loans 4,008 2,939

Other real estate owned (2) 1,226 26

---------- ----------

Total nonperforming assets $ 5,234 $ 2,965

========== ==========

Nonperforming loans as a % of loans 1.13% .91%

---------- ----------

Nonperforming assets as a % of assets 1.28% .77%

---------- ----------

Reserve for Loan Losses:

At period end $ 4,146 $ 5,006

---------- ----------

As a % of loans 1.17% 1.55%

---------- ----------

As a % of nonperforming loans 103.42% 170.33%

---------- ----------

As a % of nonaccrual loans 125.71% 172.68%

========== ==========

Charge-off Information:

Average loans $ 333,415 $ 278,953

---------- ----------

Net charge-offs $ 1,261 $ 241

---------- ----------

Charge-offs as a % of average loans .38% .09%

---------- ----------

(1) Nonaccrual loans at December 31, 2007 include loans totaling $2.036

million with specific reserves of $.741 million that were originated

before the recapitalization. Nonaccrual loans originated after the

recapitalization total $1.262 million and have specific reserves of

$.478 million.

(2) Most recently appraised at $1.533 million

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

QUARTERLY FINANCIAL HIGHLIGHTS

QUARTER ENDED

-----------------------------------------------------

(Unaudited)

-----------------------------------------------------

December September June March December

31, 30, 30, 31, 31,

2007 2007 2007 2007 2006

--------- --------- --------- --------- ---------

BALANCE SHEET

(Dollars in

thousands)

Total loans $ 355,079 $ 344,149 $ 338,896 $ 318,421 $ 322,581

Allowance for loan

losses (4,146) (5,022) (4,920) (4,975) (5,006)

--------- --------- --------- --------- ---------

Total loans, net 350,933 339,127 333,976 313,446 317,575

Intangible assets 124 143 163 182 205

Total assets 408,880 401,213 393,319 375,644 382,791

Core deposits 199,809 218,638 211,773 201,529 199,609

Noncore deposits (1) 121,018 102,733 109,473 102,883 112,812

--------- --------- --------- --------- ---------

Total deposits 320,827 321,371 321,246 304,412 312,421

Total borrowings 45,949 38,239 38,307 38,307 38,307

Total shareholders'

equity 39,321 38,697 30,485 29,932 28,790

Total shares

outstanding 3,428,695 3,428,695 3,428,695 3,428,695 3,428,695

AVERAGE BALANCES

(Dollars in

thousands)

Assets $ 406,308 $ 400,105 $ 382,065 $ 380,403 $ 366,566

Loans 350,050 340,391 324,721 318,072 301,508

Deposits 324,194 327,293 309,469 309,619 294,755

Equity 38,973 32,184 30,412 29,254 28,646

INCOME STATEMENT

(Dollars in

thousands)

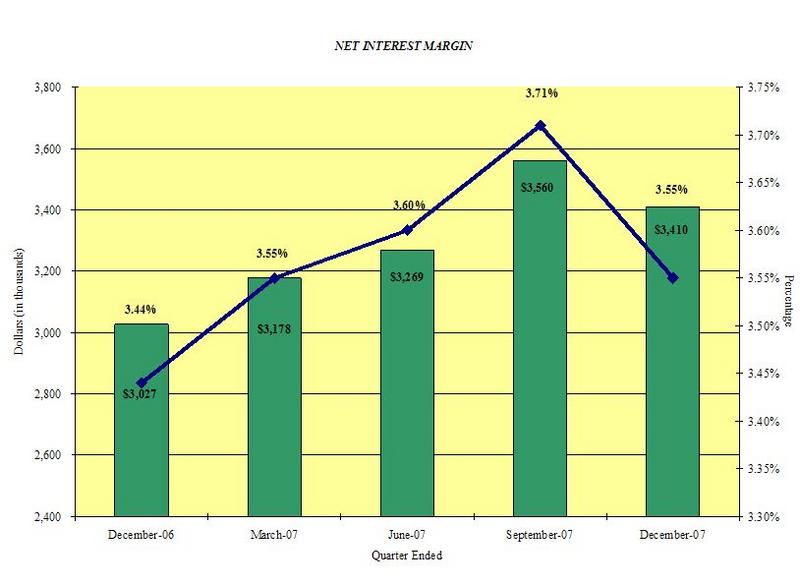

Net interest income $ 3,410 $ 3,560 $ 3,269 $ 3,178 $ 3,027

Provision for loan

losses - 400 - - (261)

--------- --------- --------- --------- ---------

Net interest

income after

provision 3,410 3,160 3,269 3,178 3,288

Total noninterest

income 355 396 342 913 276

Total noninterest

expense 2,978 3,001 3,065 3,056 3,226

--------- --------- --------- --------- ---------

Income before taxes 787 555 546 1,035 338

Provision for income

taxes 260 (7,500) - - -

--------- --------- --------- --------- ---------

Net income $ 527 $ 8,055 $ 546 $ 1,035 $ 338

========= ========= ========= ========= =========

PER SHARE DATA

Earnings - basic $ .15 $ 2.35 $ .16 $ .30 $ .10

Earnings - diluted .15 2.35 .16 .30 .10

Book value 11.47 11.29 8.89 8.73 8.40

Market value,

closing price 8.98 8.75 9.45 9.26 11.50

ASSET QUALITY RATIOS

Nonperforming

loans/total loans 1.13% .92% 1.49% 1.53% .91%

Nonperforming

assets/total assets 1.28 .90 1.30 1.33 .77

Allowance for loan

losses/total loans 1.17 1.46 1.45 1.56 1.55

Allowance for loan

losses/nonperformi-

ng loans 103.42 158.32 97.45 102.32 170.33

PROFITABILITY RATIOS

Return on average

assets .51% 7.99% .57% 1.10% .37%

Return on average

equity 5.36 99.30 7.20 14.35 4.68

Net interest margin 3.55 3.71 3.60 3.55 3.44

Efficiency ratio 78.02 74.71 83.18 82.39 94.60

Average

loans/average

deposits 107.98 104.00 104.93 102.73 102.29

CAPITAL ADEQUACY

RATIOS

Tier 1 leverage

ratio 8.05% 8.03% 7.97% 7.85% 7.85%

Tier 1 capital to

risk weighted

assets 8.97 9.03 8.85 9.16 8.77

Total capital to

risk weighted

assets 10.13 10.28 10.10 10.41 10.02

Average

equity/average

assets 9.59 8.04 7.96 7.69 7.81

Tangible

equity/tangible

assets, period end 9.59 9.61 7.71 7.92 7.47

(1) Noncore deposits includes Internet CDs, brokered deposits and CDs

greater than $100,000

Contact Information: Contact: Investor Relations (888) 343-8147 Website: www.bankmbank.com