MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

SELECTED FINANCIAL HIGHLIGHTS

(Dollars in thousands, except per share data)

For The Period Ended

------------------------------------------

March 31, December 31, March 31,

2010 2009 2009

------------ ------------ ------------

(Unaudited) (Unaudited) (Unaudited)

Selected Financial Condition

Data (at end of period):

Assets $ 502,427 $ 515,377 $ 466,375

Loans 377,311 384,310 370,776

Investment securities 36,841 46,513 51,071

Deposits 405,212 421,389 385,757

Borrowings 36,140 36,140 36,210

Shareholders' Equity 58,722 55,299 41,864

Selected Statements of Income

Data:

Net interest income $ 4,022 $ 16,287 $ 3,495

Income before taxes and

preferred dividend 300 3,536 97

Net income 3,526 1,907 90

Income per common share - Basic 1.03 .56 .03

Income per common share -

Diluted 1.03 .56 .03

Weighted average shares

outstanding 3,419,736 3,419,736 3,419,736

Selected Financial Ratios and

Other Data:

Performance Ratios:

Net interest margin 3.51% 3.59% 3.35%

Efficiency ratio 78.12 73.37 82.36

Return on average assets 2.81 .39 .08

Return on average equity 25.95 3.77 .87

Average total assets $ 508,495 $ 493,652 $ 454,741

Average total shareholders'

equity 55,109 50,531 41,813

Average loans to average

deposits ratio 92.93% 92.99% 99.54%

Common Share Data (at end of

period):

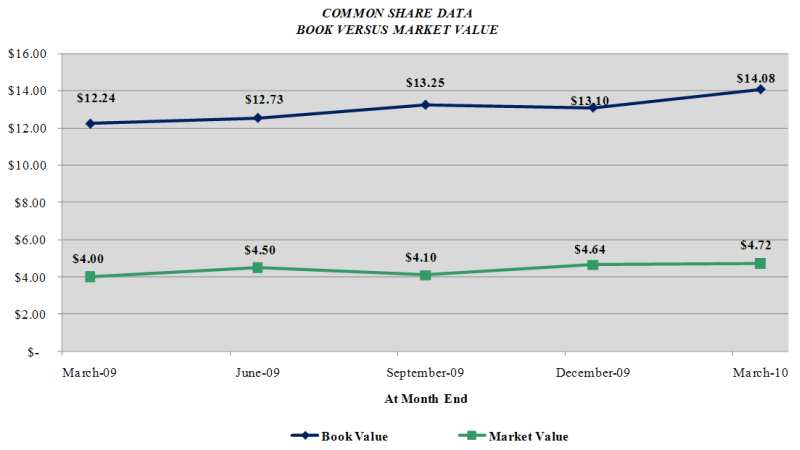

Market price per common share $ 4.72 $ 4.64 $ 4.00

Book value per common share $ 14.08 $ 13.10 $ 12.24

Common shares outstanding 3,419,736 3,419,736 3,419,736

Other Data (at end of period):

Allowance for loan losses $ 4,737 $ 5,225 $ 4,793

Non-performing assets $ 17,619 $ 21,041 $ 15,252

Allowance for loan losses to

total loans 1.26% 1.36% 1.29%

Non-performing assets to total

assets 3.51% 4.08% 3.27%

Number of:

Branch locations 10 10 13

FTE Employees 103 100 101

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

March 31, December 31, March 31,

(Dollars in thousands) 2010 2009 2009

------------ ------------ ------------

(unaudited) (unaudited)

ASSETS

Cash and due from banks $ 19,359 $ 18,433 $ 21,394

Federal funds sold 36,000 27,000 -

------------ ------------ ------------

Cash and cash equivalents 55,359 45,433 21,394

Interest-bearing deposits in

other financial institutions 700 678 569

Securities available for sale 36,841 46,513 51,071

Federal Home Loan Bank stock 3,794 3,794 3,794

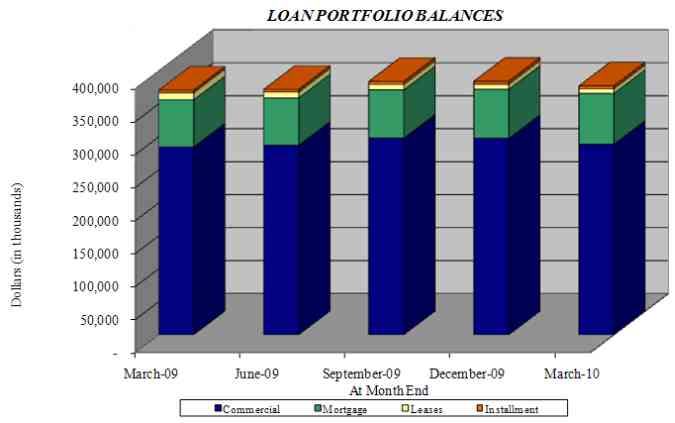

Loans:

Commercial 296,271 305,670 295,595

Mortgage 76,996 74,350 71,554

Installment 4,044 4,290 3,627

------------ ------------ ------------

Total Loans 377,311 384,310 370,776

Allowance for loan

losses (4,737) (5,225) (4,793)

------------ ------------ ------------

Net loans 372,574 379,085 365,983

Premises and equipment 10,060 10,165 11,134

Other real estate held for sale 7,723 5,804 2,199

Other assets 15,376 23,905 10,231

------------ ------------ ------------

TOTAL ASSETS $ 502,427 $ 515,377 $ 466,375

============ ============ ============

LIABILITIES AND SHAREHOLDERS'

EQUITY

LIABILITIES:

Deposits:

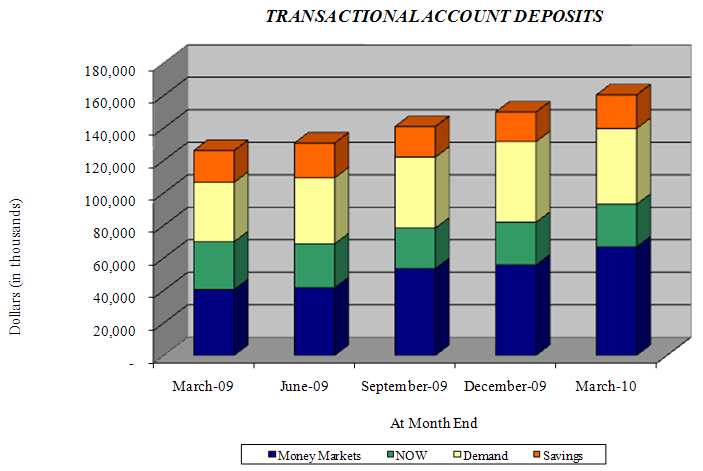

Noninterest bearing deposits $ 30,356 $ 35,878 $ 31,541

NOW, money market, checking 109,374 95,790 75,026

Savings 20,675 18,207 19,585

CDs < $100,000 75,822 59,953 70,708

CDs > $100,000 30,173 36,385 26,886

Brokered 138,812 175,176 162,011

------------ ------------ ------------

Total deposits 405,212 421,389 385,757

Borrowings:

Federal Home Loan Bank 35,000 35,000 -

Other 1,140 1,140 36,210

------------ ------------ ------------

Total borrowings 36,140 36,140 36,210

Other liabilities 2,353 2,549 2,544

------------ ------------ ------------

Total liabilities 443,705 460,078 424,511

Shareholders' equity:

Preferred stock - No par

value:

Authorized 500,000 shares,

11,000 shares issued and

outstanding 10,562 10,514 -

Common stock and additional

paid in capital - No par

value

Authorized - 18,000,000

shares

Issued and outstanding -

3,419,736 shares 43,502 43,493 42,833

Accumulated earnings

(deficit) 3,724 199 (1,618)

Accumulated other

comprehensive income 934 1,093 649

------------ ------------ ------------

Total shareholders'

equity 58,722 55,299 41,864

------------ ------------ ------------

TOTAL LIABILITIES AND

SHAREHOLDERS' EQUITY $ 502,427 $ 515,377 $ 466,375

============ ============ ============

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

Three Months Ended

March 31,

---------------------------

(Dollars in thousands except per share data) 2010 2009

------------ -------------

(Unaudited) (Unaudited)

INTEREST INCOME:

Interest and fees on loans:

Taxable $ 5,191 $ 5,002

Tax-exempt 52 90

Interest on securities:

Taxable 397 459

Tax-exempt 7 1

Other interest income 40 2

------------ -------------

Total interest income 5,687 5,554

------------ -------------

INTEREST EXPENSE:

Deposits 1,457 1,778

Borrowings 208 281

------------ -------------

Total interest expense 1,665 2,059

------------ -------------

Net interest income 4,022 3,495

Provision for loan losses 900 550

------------ -------------

Net interest income after provision for loan

losses 3,122 2,945

------------ -------------

OTHER INCOME:

Service fees 223 243

Net security gains 215 -

Net gains on sale of secondary market

loans 316 58

Other 53 90

------------ -------------

Total noninterest income 807 391

------------ -------------

OTHER EXPENSE:

Salaries and employee benefits 1,720 1,597

Occupancy 345 378

Furniture and equipment 194 189

Data processing 189 220

Professional service fees 173 153

Loan and deposit 395 136

FDIC insurance assessment 222 125

Telephone 47 43

Advertising 72 78

Other 272 320

------------ -------------

Total noninterest expense 3,629 3,239

------------ -------------

Income before provision for income taxes 300 97

Provision for income taxes (3,411) 7

------------ -------------

NET INCOME 3,711 90

------------ -------------

Preferred dividend and accretion of discount 185 -

------------ -------------

NET INCOME AVAILABLE TO COMMON SHAREHOLDERS 3,526 90

============ =============

INCOME PER COMMON SHARE:

Basic $ 1.03 $ .03

============ =============

Diluted $ 1.03 $ .03

============ =============

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

LOAN PORTFOLIO AND CREDIT QUALITY

(Dollars in thousands)

Loan Portfolio Balances (at end of period):

March 31, December 31, March 31,

2010 2009 2009

------------- ------------- -------------

Commercial Loans

Real estate - operators of

nonresidential buildings $ 49,753 $ 48,689 $ 40,457

Hospitality and tourism 44,820 45,315 35,224

Real estate agents and managers 21,529 24,242 28,012

Operators of nonresidential

buildings 13,170 12,619 13,512

Other 138,964 150,214 151,732

------------- ------------- -------------

Total Commercial Loans 268,236 281,079 268,937

1-4 family residential real

estate 70,087 67,232 65,792

Consumer 4,044 4,290 3,627

Construction

Commercial 28,035 24,591 26,658

Consumer 6,909 7,118 5,762

------------- ------------- -------------

Total Loans $ 377,311 $ 384,310 $ 370,776

============= ============= =============

Credit Quality (at end of period):

March 31, December 31, March 31,

2010 2009 2009

------------ ------------ ------------

Nonperforming Assets:

Nonaccrual loans $ 9,027 $ 14,368 $ 12,461

Loans past due 90 days or more - - -

Restructured loans 869 869 592

------------ ------------ ------------

Total nonperforming loans 9,896 15,237 13,053

Other real estate owned 7,723 5,804 2,199

------------ ------------ ------------

Total nonperforming assets $ 17,619 $ 21,041 $ 15,252

============ ============ ============

Nonperforming loans as a % of

loans 2.62% 3.96% 3.52%

------------ ------------ ------------

Nonperforming assets as a % of

assets 3.51% 4.08% 3.27%

------------ ------------ ------------

Reserve for Loan Losses:

At period end $ 4,737 $ 5,225 $ 4,793

------------ ------------ ------------

As a % of loans 1.26% 1.39% 1.29%

------------ ------------ ------------

As a % of nonperforming loans 47.87% 34.29% 36.72%

------------ ------------ ------------

As a % of nonaccrual loans 52.48% 36.37% 38.46%

============ ============ ============

Charge-off Information (year to

date):

Average loans 384,640 374,796 370,943

------------ ------------ ------------

Net charge-offs 1,389 2,752 34

------------ ------------ ------------

Charge-offs as a % of

average loans .36% .73% .01%

------------ ------------ ------------

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES QUARTERLY FINANCIAL

HIGHLIGHTS

QUARTER ENDED

-------------------------------------------------------------

(Unaudited)

-------------------------------------------------------------

March 31, December 31, September 30, June 30, March 31,

2010 2009 2009 2009 2009

--------- ------------ ------------- --------- ---------

BALANCE

SHEET

(Dollars in

thousands)

Total loans $ 377,311 $ 384,310 $ 384,100 $ 372,004 $ 370,776

Allowance

for loan

losses (4,737) (5,225) (4,081) (4,119) (4,793)

--------- ------------ ------------- --------- ---------

Total

loans,

net 372,574 379,085 380,019 367,885 365,983

Intangible

assets - - - 6 26

Total assets 502,427 515,377 513,180 506,304 466,375

Core

deposits 236,227 209,828 200,541 202,892 196,860

Noncore

deposits

(1) 168,985 211,561 218,040 210,260 188,897

--------- ------------ ------------- --------- ---------

Total

deposits 405,212 421,389 418,581 413,152 385,757

Total

borrowings 36,140 36,140 36,140 36,210 36,210

Total

shareholders'

equity 58,722 55,299 55,766 53,939 41,864

Total shares

outstanding 3,419,736 3,419,736 3,419,736 3,419,736 3,419,736

AVERAGE

BALANCES

(Dollars in

thousands)

Assets $ 508,495 $ 514,102 $ 513,687 $ 491,205 $ 454,740

Loans 384,640 386,203 370,310 371,609 370,943

Deposits 413,897 418,280 419,102 401,510 372,669

Equity 55,109 55,665 54,594 49,855 41,813

INCOME

STATEMENT

(Dollars in

thousands)

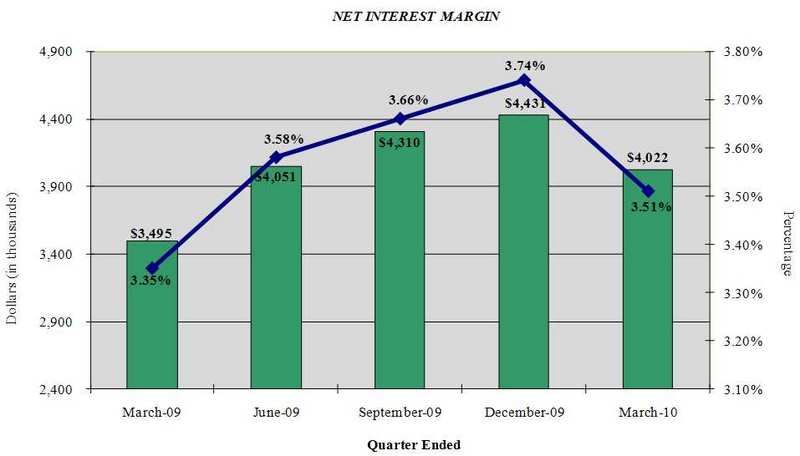

Net interest

income $ 4,022 $ 4,431 $ 4,310 $ 4,051 $ 3,495

Provision

for loan

losses 900 2,300 700 150 550

--------- ------------ ------------- --------- ---------

Net

interest

income

after

pro-

vision 3,122 2,131 3,610 3,901 2,945

Total

noninterest

income 807 1,503 2,418 439 391

Total

noninterest

expense 3,629 3,650 3,443 3,470 3,239

--------- ------------ ------------- --------- ---------

Income

before

taxes 300 (16) 2,585 870 97

Provision

for income

taxes (3,411) (22) 864 271 7

--------- ------------ ------------- --------- ---------

Net

income 3,711 6 1,721 599 90

--------- ------------ ------------- --------- ---------

Preferred

dividend

expense 185 186 185 138 -

--------- ------------ ------------- --------- ---------

Net income

available

to common

share-

holders $ 3,526 $ (180) $ 1,536 $ 461 $ 90

========= ============ ============= ========= =========

PER SHARE

DATA

Earnings $ 1.03 $ (.05) $ .45 $ .13 $ .03

Book value

per common

share 14.08 13.10 13.25 12.73 12.24

Market

value,

closing

price 4.72 4.64 4.10 4.50 4.00

ASSET

QUALITY

RATIOS

Nonperforming

loans/total

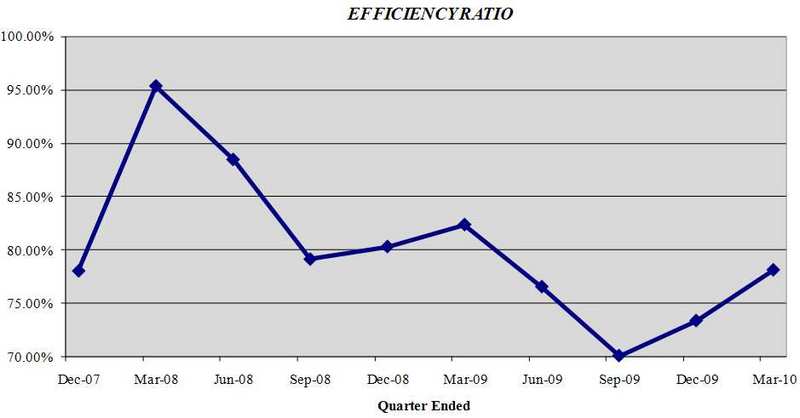

loans 2.62% 3.96 % 3.00% 2.66% 3.52%

Nonperforming

assets/total

assets 3.51 4.08 3.38 2.93 3.27

Allowance

for loan

losses/

total

loans 1.26 1.36 1.06 1.11 1.29

Allowance

for loan

losses/non-

performing

loans 47.87 34.29 35.40 41.71 36.72

PROFITABILITY

RATIOS

Return on

average

assets 2.81% (.14)% 1.19% .38% .08%

Return on

average

equity 25.95 (1.28) 11.16 3.71 .87

Net interest

margin 3.51 3.74 3.66 3.58 3.35

Efficiency

ratio 78.12 71.03 70.09 76.55 82.36

Average

loans/average

deposits 92.93 92.33 88.36 92.55 99.54

CAPITAL

ADEQUACY

RATIOS

Tier 1

leverage

ratio 9.85% 9.75 % 9.74% 9.65% 7.86%

Tier 1

capital to

risk

weighted

assets 12.48 11.92 12.18 11.94 9.31

Total

capital to

risk

weighted

assets 13.69 13.17 13.19 13.00 10.56

Average

equity/

average

assets 10.84 10.83 10.63 10.15 9.19

Tangible

equity/

tangible

assets 10.84 10.83 10.87 10.65 8.97

(1) Noncore deposits includes Internet CDs, brokered deposits and CDs

greater than $100,000

Contact Information: Contact: Investor Relations (888) 343-8147 Website: www.bankmbank.com