MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

SELECTED FINANCIAL HIGHLIGHTS

(Dollars in thousands, except per share data)

For The Period Ended

-------------------------------------

September December September

30, 31, 30,

2007 2006 2006

----------- ----------- -----------

(Unaudited) (Unaudited)

Selected Financial Condition Data

(at end of period):

Total assets $ 401,213 $ 382,791 $ 363,191

Total loans 344,149 322,581 292,614

Total deposits 321,371 312,421 293,494

Borrowings and subordinated

debentures 38,239 38,307 38,307

Total shareholders' equity 38,697 28,790 28,226

Selected Statements of Income Data

(nine months and year ended):

Net interest income $ 10,007 $ 11,593 $ 8,566

Income before taxes 2,136 1,216 878

Net income 9,636 1,716 1,378

Income per common share - Basic 2.81 .50 .40

Income per common share - Diluted 2.81 .50 .40

Three Months Ended:

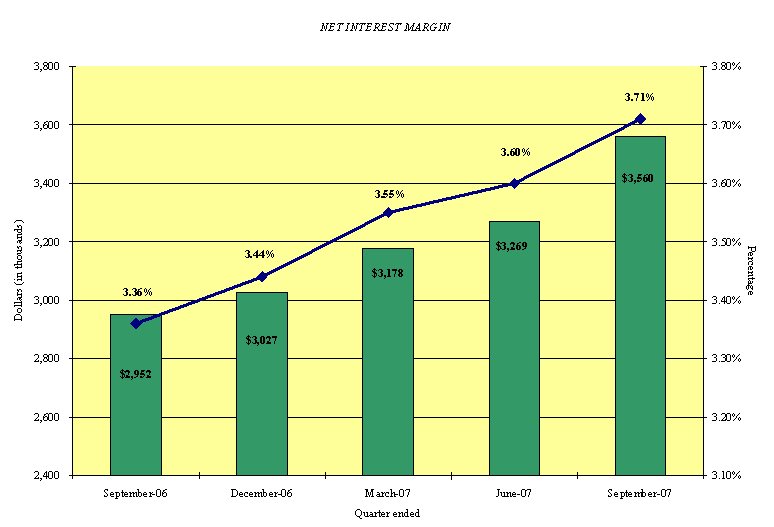

Net interest income $ 3,560 $ 3,027 $ 2,952

Income before taxes 555 338 190

Net income 8,055 338 690

Income per common share - Basic 2.35 .10 .20

Income per common share - Diluted 2.35 .10 .20

Selected Financial Ratios and Other

Data (nine months and year ended):

Performance Ratios:

Net interest margin 3.62% 3.51% 3.53%

Efficiency ratio 79.94 93.95 93.83

Return on average assets 3.32 .49 .54

Return on average equity 42.07 6.19 6.71

Average total assets $ 387,597 $ 347,927 $ 341,646

Average total shareholders' equity $ 30,627 $ 27,744 $ 27,440

Average loans to average deposits

ratio 103.89% 99.77% 98.86%

Common Share Data (at end of

period):

Market price per common share $ 8.75 $ 11.50 $ 10.56

Book value per common share $ 11.29 $ 8.40 $ 8.23

Common shares outstanding 3,428,695 3,428,695 3,428,695

Weighted average shares outstanding 3,428,695 3,428,695 3,428,695

Other Data (at end of period):

Allowance for loan losses $ 5,022 $ 5,006 $ 5,316

Non-performing assets $ 3,623 $ 2,965 $ 2,091

Allowance for loan losses to total

loans 1.46% 1.55% 1.82%

Non-performing assets to total

assets .90% .77% .58%

Number of:

Branch locations 13 13 13

FTE Employees 105 99 97

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

September December September

30, 31, 30,

2007 2006 2006

----------- ----------- -----------

(unaudited) (unaudited)

ASSETS

Cash and due from banks $ 7,364 $ 4,865 $ 5,537

Federal funds sold 947 5,841 11,949

----------- ----------- -----------

Cash and cash equivalents 8,311 10,706 17,486

Interest-bearing deposits in other

financial institutions 6,995 856 889

Securities available for sale 17,973 32,769 36,129

Federal Home Loan Bank stock 3,794 3,794 4,152

Loans:

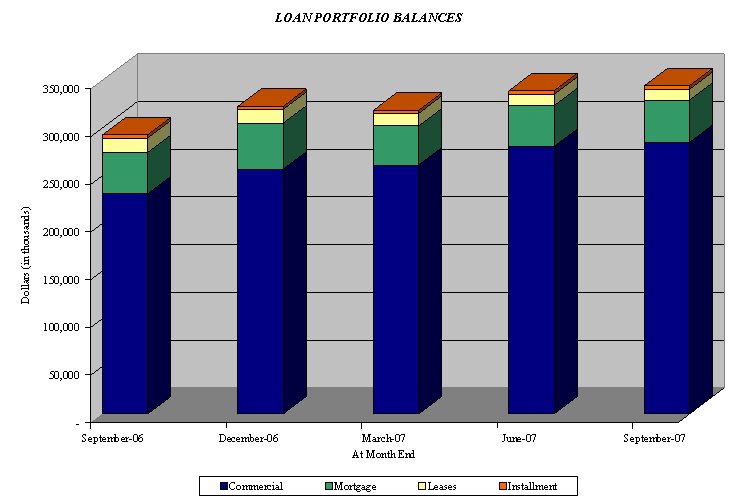

Commercial 285,680 261,726 238,481

Mortgage 54,962 58,014 51,341

Installment 3,507 2,841 2,792

----------- ----------- -----------

Total Loans 344,149 322,581 292,614

Allowance for loan losses (5,022) (5,006) (5,316)

----------- ----------- -----------

Net loans 339,127 317,575 287,298

Premises and equipment 12,733 12,453 12,643

Other real estate held for sale 451 26 26

Other assets 11,829 4,612 4,568

----------- ----------- -----------

TOTAL ASSETS $ 401,213 $ 382,791 $ 363,191

=========== =========== ===========

LIABILITIES AND SHAREHOLDERS' EQUITY

Liabilities:

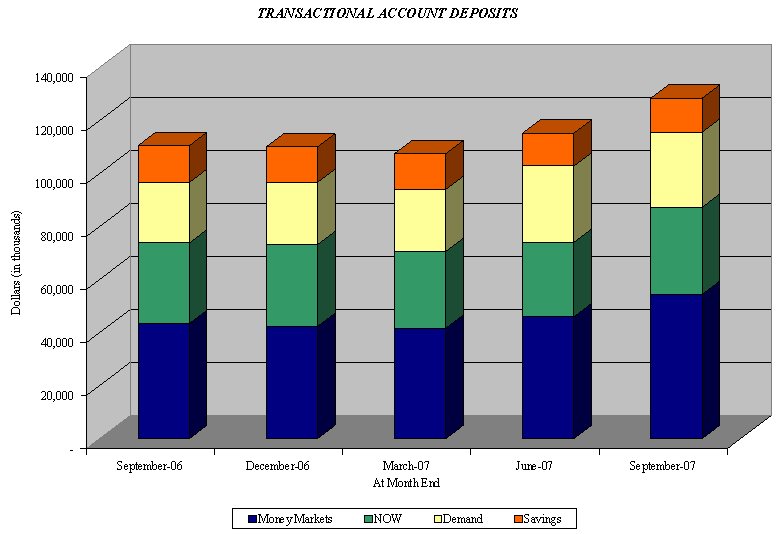

Non-interest-bearing deposits $ 28,325 $ 23,471 $ 22,826

Interest-bearing deposits:

NOW and Money Market 87,262 73,188 73,797

Savings 12,831 13,365 13,915

CDs < $100,000 90,220 89,585 85,236

CDs > $100,000 24,432 23,645 20,305

Brokered 78,301 89,167 77,415

----------- ----------- -----------

Total deposits 321,371 312,421 293,494

Borrowings 38,239 38,307 38,307

Other liabilities 2,906 3,273 3,164

----------- ----------- -----------

Total liabilities 362,516 354,001 334,965

Shareholders' equity:

Preferred stock - No par value:

Authorized 500,000 shares, no

shares outstanding

Common stock and additional paid

in capital - No par value

Authorized - 18,000,000 shares

Issued and outstanding -

3,428,695 shares 42,810 42,722 42,646

Accumulated deficit (4,107) (13,745) (14,083)

Accumulated other comprehensive

(loss) (6) (187) (337)

----------- ----------- -----------

Total shareholders' equity 38,697 28,790 28,226

----------- ----------- -----------

TOTAL LIABILITIES AND SHAREHOLDERS'

EQUITY $ 401,213 $ 382,791 $ 363,191

=========== =========== ===========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

Three Months Ended Nine Months Ended

September 30, September 30,

---------------------- ----------------------

2007 2006 2007 2006

---------- ---------- ---------- ----------

INTEREST INCOME:

Interest and fees on

loans:

Taxable $ 6,929 $ 5,635 $ 19,610 $ 15,316

Tax-exempt 118 189 432 575

Interest on securities

Taxable 263 306 857 852

Tax-exempt - 5 - 87

Other interest 209 268 575 631

---------- ---------- ---------- ----------

Total interest income 7,519 6,403 21,474 17,461

---------- ---------- ---------- ----------

INTEREST EXPENSE:

Deposits 3,443 2,951 9,932 7,540

Borrowings 516 500 1,535 1,355

---------- ---------- ---------- ----------

Total interest expense 3,959 3,451 11,467 8,895

---------- ---------- ---------- ----------

Net interest income 3,560 2,952 10,007 8,566

Provision for loan losses 400 - 400 (600)

---------- ---------- ---------- ----------

Net interest income after

provision for loan losses 3,160 2,952 9,607 9,166

---------- ---------- ---------- ----------

OTHER INCOME:

Service fees 169 133 515 365

Net gains on sale of

secondary market loans 165 66 364 149

Proceeds from settlement

of lawsuit - - 470 -

Other 62 41 302 193

---------- ---------- ---------- ----------

Total other income 396 240 1,651 707

---------- ---------- ---------- ----------

OTHER EXPENSE:

Salaries and employee

benefits 1,695 1,487 5,106 4,577

Occupancy 322 333 983 943

Furniture and equipment 178 159 501 470

Data processing 196 176 577 512

Professional service

fees 78 341 403 955

Loan and deposit 63 78 214 305

Telephone 68 55 185 155

Advertising 97 70 280 247

Other 304 303 873 831

---------- ---------- ---------- ----------

Total other expense 3,001 3,002 9,122 8,995

---------- ---------- ---------- ----------

Income before income taxes 555 190 2,136 878

Provision for (benefit of)

income taxes (7,500) (500) (7,500) (500)

---------- ---------- ---------- ----------

NET INCOME $ 8,055 $ 690 $ 9,636 $ 1,378

========== ========== ========== ==========

INCOME PER COMMON SHARE:

Basic $ 2.35 $ .20 $ 2.81 $ .40

========== ========== ========== ==========

Diluted $ 2.35 $ .20 $ 2.81 $ .40

========== ========== ========== ==========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

LOAN PORTFOLIO AND CREDIT QUALITY

(Dollars in thousands)

Loan Portfolio Balances (at end of period):

September 30, December 31, September 30,

2007 2006 2006

------------- ------------- -------------

Commercial Loans

Real estate - operators of

nonresidential buildings $ 43,422 $ 44,308 $ 35,965

Hospitality and tourism 37,479 30,826 37,287

Real estate agents and managers 25,662 25,071 19,744

Offices of holding companies 10,831 4,989 1,496

Other 122,460 120,523 110,894

------------- ------------- -------------

Total Commercial Loans 239,854 225,717 205,386

1-4 family residential real

estate 54,962 58,014 51,341

Construction 45,826 36,009 33,095

Consumer 3,507 2,841 2,792

------------- ------------- -------------

Total Loans $ 344,149 $ 322,581 $ 292,614

============= ============= =============

Average loans for the period $ 327,810 $ 278,953 $ 271,351

============= ============= =============

Credit Quality (at end of period):

September 30, December 31, September 30,

2007 2006 2006

------------- ------------- -------------

Nonperforming Assets :

Nonaccrual loans $ 3,136 $ 2,899 $ 2,065

Loans past due 90 days or more 36 40 -

Restructured loans - - -

------------ ------------ ------------

Total nonperforming loans 3,172 2,939 2,065

Other real estate owned 451 26 26

------------ ------------ ------------

Total nonperforming assets $ 3,623 $ 2,965 $ 2,091

============ ============ ============

Nonperforming loans as a % of

loans .92% .91% .71%

------------ ------------ ------------

Nonperforming assets as a % of

assets .90% .77% .58%

------------ ------------ ------------

Reserve for Loan Losses:

At period end $ 5,022 $ 5,006 $ 5,316

------------ ------------ ------------

As a % of loans 1.46% 1.55% 1.82%

------------ ------------ ------------

As a % of nonperforming loans 158.32% 170.33% 257.43%

------------ ------------ ------------

As a % of nonaccrual loans 160.14% 172.68% 257.43%

------------ ------------ ------------

Net charge-offs as a % of average

loans .12% .08% .07%

============ ============ ============

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

QUARTERLY FINANCIAL HIGHLIGHTS

QUARTER ENDED

(Unaudited)

-----------------------------------------------------

September June March December September

30, 30, 31, 31, 30,

2007 2007 2007 2006 2006

--------- --------- --------- --------- ---------

BALANCE SHEET

(Dollars in

thousands)

Total loans $ 344,149 $ 338,896 $ 318,421 $ 322,581 $ 292,614

Allowance for loan

losses (5,022) (4,920) (4,975) (5,006) (5,316)

--------- --------- --------- --------- ---------

Total loans, net 339,127 333,976 313,446 317,575 287,298

Intangible assets 143 163 182 205 237

Total assets 401,213 393,319 375,644 382,791 363,191

Core deposits 218,638 211,773 201,529 199,609 195,774

Noncore deposits (1) 102,733 109,473 102,883 112,812 97,720

--------- --------- --------- --------- ---------

Total deposits 321,371 321,246 304,412 312,421 293,494

Total borrowings 38,239 38,307 38,307 38,307 38,307

Total shareholders'

equity 38,697 30,485 29,932 28,790 28,226

Total shares

outstanding 3,428,695 3,428,695 3,428,695 3,428,695 3,428,695

AVERAGE BALANCES

(Dollars in

thousands)

Assets $ 400,105 $ 382,065 $ 380,403 $ 366,566 $ 362,632

Loans 340,391 324,721 318,072 301,508 289,210

Deposits 327,293 309,469 309,619 294,755 296,608

Equity 32,184 30,412 29,254 28,646 28,041

INCOME STATEMENT

(Dollars in

thousands)

Net interest income $ 3,560 $ 3,269 $ 3,178 $ 3,027 $ 2,952

Provision for loan

losses 400 - - (261) -

--------- --------- --------- --------- ---------

Net interest

income after

provision 3,160 3,269 3,178 3,288 2,952

Total noninterest

income 396 342 913 276 240

Total noninterest

expense 3,001 3,065 3,056 3,226 3,002

--------- --------- --------- --------- ---------

Income before taxes 555 546 1,035 338 190

Provision for income

taxes (7,500) - - - (500)

--------- --------- --------- --------- ---------

Net income $ 8,055 $ 546 $ 1,035 $ 338 $ 690

========= ========= ========= ========= =========

PER SHARE DATA

Earnings - basic $ 2.35 $ .16 $ .30 $ .10 $ .20

Earnings - diluted 2.35 .16 .30 .10 .20

Book value 11.29 8.89 8.73 8.40 8.23

Market value,

closing price 8.75 9.45 9.26 11.50 10.56

ASSET QUALITY RATIOS

Nonperforming

loans/total loans .92% 1.49% 1.53% .91% .71%

Nonperforming

assets/total assets .90 1.30 1.33 .77 .58

Allowance for loan

losses/total loans 1.46 1.45 1.56 1.55 1.82

Allowance for loan

losses/nonperformi-

ng loans 158.32 97.45 102.32 170.33 257.43

PROFITABILITY RATIOS

Return on average

assets 7.99% .57% 1.10% .37% .75%

Return on average

equity 99.30 7.20 14.35 4.68 9.76

Net interest margin 3.71 3.60 3.55 3.44 3.36

Efficiency ratio 74.71 83.21 82.40 94.60 91.17

Average

loans/average

deposits 104.00 104.93 102.73 102.29 97.51

CAPITAL ADEQUACY

RATIOS

Tier 1 leverage

ratio 8.03% 7.97% 7.85% 7.85% 7.81%

Tier 1 capital to

risk weighted

assets 9.03 8.85 9.16 8.77 9.36

Total capital to

risk weighted

assets 10.28 10.10 10.41 10.02 10.62

Average

equity/average

assets 8.04 7.96 7.69 7.81 7.73

Tangible

equity/tangible

assets, period end 9.61 7.71 7.92 7.47 7.71

(1) Noncore deposits includes Internet CDs, brokered deposits and CDs

greater than $100,000

Contact Information: Contact: Investor Relations (888) 343-8147 Website: www.bankmbank.com