VANCOUVER, BRITISH COLUMBIA--(Marketwire - July 7, 2011) - Anfield Nickel Corp. (TSX VENTURE:ANF) ("Anfield") is pleased to announce the results of the preliminary economic assessment ("PEA") on its 100% owned Mayaniquel nickel project located in northeastern Guatemala (the "Project"). The results of the PEA indicate that a ferronickel operation at Mayaniquel has favourable economic potential and the Project should be advanced to a prefeasibility study. Highlights of the study are as follows (all dollar figures in US dollars):

Highlights

- Robust project economics driven by a low strip ratio (0.35:1), excellent metallurgy, good existing infrastructure, a large mineral resource and amenability of ore to physical upgrading to increase nickel grades of plant feed.

- Base case net present value ("NPV") of $606 million, at an 8% discount rate, and an internal rate of return ("IRR") of 14.1%.

- The base case assumes a long term nickel price of $8.25/lb, an 8% real discount rate, a $0.19/lb contained iron credit, $0.08/Kwh power cost and $100/tonne long term coal price (including freight) (the "Base Case").

- The PEA was completed on only the mineral resources contained within Anfield's Sechol and Tres Juanes deposits. These two deposits comprise approximately 63% of the indicated mineral resources and 52% of the inferred mineral resources,above a 1.0% nickel cutoff, defined to date at the Project.

- Average nickel in ferronickel production of 19,900 tonnes per year for 29.5 years with an average nickel in ferronickel grade of 22.5%.

- Capital payback in 5.2 years.

- C-1 life of mine ("LOM") cash costs (net of iron credits) estimated to average $3.14 per pound of nickel sold.

- The Project may generate approximately 700 permanent jobs and 800 direct jobs during the three year construction period and potentially $1.8 billion in taxes and government royalties payable to the Guatemalan government.

The salient details of the PEA are summarized in the table below (all dollar figures are in US dollars):

| NPV ($8.25/lb Ni, 8% discount rate) | $606 million |

| IRR | 14.1% |

| Initial Capital Expenditure | $1,227 million |

| Sustaining Capital Expenditure | $199 million |

| LOM C-1 Cash Costs (net by-product credits) | $3.14/lb Ni sold |

| Rotary Kiln Furnace Capacity | 80MW |

| Annual Ore to Plant | 1.33 million tonnes |

| Strip Ratio (excluding sorting plant rejects) | 0.35:1 |

| Mine Life | 29.5 years |

| Ore Grade Upgrading | 29% |

| Average grade of Mineral Resources delivered to plant | 1.68% Ni |

| LOM average annual nickel in ferronickel production | 19,900 tonnes |

Anfield will host a conference call on Thursday July 7th, 2011 at 11:00 am (Pacific) or 2:00 pm (Eastern) to discuss these results. Call-in information is provided at the bottom of this news release.

The PEA was supervised by William Rose, P.E. and Principal of WLR Consulting, Inc., a qualified person. Mr. Rose has reviewed and approved the contents of this news release. The PEA was managed by MTB Project Management Professionals, Inc. (project management, infrastructure, ancillary capital and operating costs and cash flow modeling) and comprised several studies prepared by: SIM Geological Inc. and BD Resource Consulting, Inc. (resource estimate and model, quality assurance quality control program); WLR Consulting, Inc.,(mining, production schedule, and mining capital and operating costs); Dr. Nic Barcza, PrEng., (metallurgical consultant); Mintek (metallurgical testwork); Laser Analytical Systems & Automation GmbH (ore sorting testwork); Tenova Pyromet (Pty) Ltd. (process engineering, infrastructure, plant capital and operating costs);MineSense Technologies (ore upgrading); Ausenco Vector (geotechnical facilities, port facilities, and barge unloading facility and capital and operating costs); Gochnour & Associates, Inc. (baseline environmental studies); and Social Capital Group (socioeconomic studies). The following consultants will serve as qualified persons for their respective sections of the technical report:

- Robert Sim, P. Geo. of SIM Geological Inc.

- Bruce Davis, FAusIMM of BD Consulting, Inc.

- Dr. Nic Barcza, HLF SAIMM

- William Rose, P.E. of WLR Consulting, Inc.

The National Instrument 43-101 compliant technical report summarizing the results of the PEA and the updated mineral resource estimate previously announced on June 9, 2011 will be available on the Company's website (www.anfieldnickel.com) and SEDAR (www.sedar.com) by July 22, 2011.

Project Economics

MTB Project Management Professionals, Inc. developed a cash flow valuation model on the Project based upon the geological and engineering work completed to date. The Base Case was developed using a long term forecast nickel price of $8.25/lb. This price forecast is significantly lower than the current price of approximately $10.50/lb nickel and the model takes into consideration a decline in the nickel price from current levels over the first four years of the mine's life to the forecast long term average price. In addition, a by-product credit of $0.19/lb iron contained within the ferronickel product has been included in the Base Case.

The following table shows the NPV of the Base Case at various discount rates:

| Discount Rate (Real) | NPV |

| 0% | $3,706 million |

| 4% | $1,551 million |

| 6% | $989 million |

| 8% | $606 million |

| 10% | $337 million |

| 12% | $146 million |

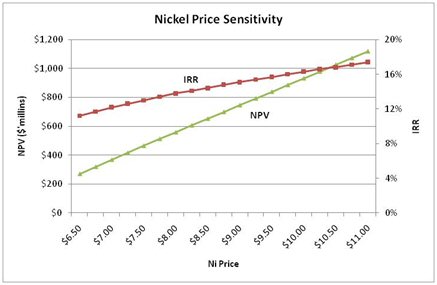

Please visit the following link to view a chart that shows the sensitivity of the Base Case's NPV (8% real discount rate) and IRR to changes in the nickel price: http://media3.marketwire.com/docs/anf707a.jpg.

{kind=link}

Mineral Resources

WLR Consulting, Inc. used the mineral resource estimate completed by Sim Geological Inc. and BD Resource Consulting, Inc. for the Sechol and Tres Juanes deposits, as disclosed in Anfield's June 9, 2011 news release, and the corresponding block model, to develop a mine plan and production schedule for the Project. That mineral resource estimate, at a 1.0% nickel cutoff grade, determined transition and saprolite indicated mineral resources of 17.2 million tonnes grading 1.62% nickel and inferred mineral resources of 23.3 million tonnes grading 1.44% nickel; and limonite indicated mineral resources of 7.5 million tonnes grading 1.20% nickel and inferred mineral resources of 7.0 million tonnes grading 1.17% nickel.

Floating cone analyses were used to determine the extent of laterite mining areas for each deposit and the best sequence for economic development. The floating cone analysis,based on a nickel price of $5.00/lb,defined the maximum economic extents of mineable mineralization, which were subsequently adjusted to conform to current concession boundaries. The resulting pit limits were then used to estimate, at a 0.8% nickel cutoff, contained indicated mineral resources of 27.7 million tonnes, contained inferred mineral resources of 31.2 million tonnes and total waste of 20.8 million tonnes in determining the mine plan and production schedule. This mine plan resulted in a LOM stripping ratio of 0.35:1. The mineral resource cutoff grade was reduced to 0.8% nickel due to the recoveries and economics associated with the ore sorting plant. Of the 58.9 million tonnes of contained mineral resources, approximately 20.0 million tonnes will be rejected in the sorting plant as a part of the ore upgrading process.

Note: Mineral resources that are not mineral reserves do not have demonstrated economic viability. The PEA is preliminary in nature and includes the use of inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. Thus, there is no certainty that the preliminary economic assessment will be realized. Actual results may vary, perhaps materially.

Mining & Processing

The Project will utilize conventional open pit mining methods and production is scheduled to deliver 3,600 tonnes per day (1.33 million tonnes per year) of lateritic ore to the plant for 29.5 years. Nineteen percent of the mined ore will be delivered directly to the processing plant, while the remaining mined material (1.61 million tonnes per year) will be sent to the upgrading plant, where low nickel grade and high iron material will be rejected, thereby providing the processing plant with a total average feed grade of 1.68% nickel. The plant feed will be sent to a single line rotary kiln where it will be dried and calcined with coal added prior to being fed into the 80MW furnace and subsequent refining furnace to produce the ferronickel product. The processing plant is forecast to produce approximately 88,300 tonnes per year of ferronickel over the mine's life containing approximately 19,900 tonnes of nickel at an average grade of 22.5% nickel.

Capital Costs

Tenova Pyromet (Pty) Ltd, MTB Project Management Professionals, Inc., Ausenco Vector, MineSense Technologies and WLR Consulting, Inc. developed capital cost estimates for the proposed mining and ferronickel operation. The following table summarizes the capital cost estimates in the PEA for the Project:

| Direct Capital Costs | $805.1 million |

| Indirect Capital Costs | $92.5 million |

| Owner Direct and Indirect Capital Costs | $169.6 million |

| Contingency (15%) | $160.0 million |

| Total (Base Case) | $1,227.2 million |

| Upfront Working Capital | $4.2 million |

| LOM Sustaining Capital Costs | $199.4 million |

The capital cost estimates have been compiled with an accuracy level of -15% to +35%.

Operating Costs

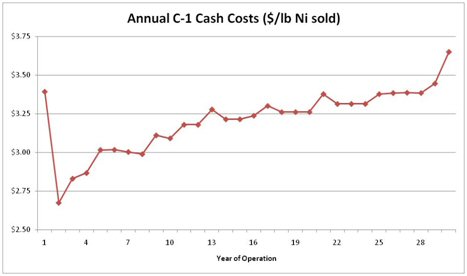

The results of the PEA show that a mine at the Project will be a low cost operation, with operating costs potentially averaging in the lower half of the industry cost curve(1). The Project benefits significantly from the low strip ratio, relatively easy terrain, excellent metallurgy, amenability of material to physical upgrading and close proximity to major infrastructure. Based upon a comprehensive study of future power supply in Guatemala that has estimated long term power costs of between $0.06 and $0.09/Kwh, the Base Case has assumed a long term power cost of $0.08/Kwh. In addition, long term coal prices used in the Base Case were assumed to be $100/tonne (including freight). The PEA estimates that the C-1 cash costs (net of iron credits) over the life of the mine will average $3.14 per pound of nickel sold. C-1 cash costs include at-mine cash operating costs, royalties (BHP Billiton and government), mine reclamation and closure costs, and ferronickel transportation and freight costs.

To see a graph of the C-1 cash costs, please visit the following link: http://media3.marketwire.com/docs/anf707b.jpg.

{kind=link}

Infrastructure

Substantial regional infrastructure is in place within the vicinity of the Project. The Project is located within 70 kilometers of the Caribbean Sea and 167 kilometers by road from the largest port in Guatemala, Santo Tomas,thus facilitating the exportation of ferronickel and importation of coal and other consumables. In addition, major power infrastructure is within two kilometres of the Project. The local labour force is large and while not versed in mining and nickel processing, provisions have been made in the capital cost estimate to train the local labour force, with the assumption that labour drawn from within Guatemala will ultimately manage and operate the mine and plant facilities.

Environmental

The Project has been designed to meet World Bank Guidelines for social and environmental management practices. Preliminary baseline studies completed to date have included surface water quality, meteorological, archaeological, social context analysis, stakeholder mapping, community health, biological (flora and fauna) and re-vegetation studies. As the nickel deposits are largely soil based, mine waste material will be largely overlying topsoil and low grade limonitic soils. Provisions have been made within the mine plan and operating costs to account for the storage of both the topsoil and low grade limonitic soils and the recontouring and re-vegetation of mined areas with these soils once the deposits have been mined.It is expected that this process will allow the mined areas to largely return to its pre-mined state of vegetation.

Next Steps

An infill drilling program at the Sechol and Tres Juanes deposits is ongoing and will form the basis upon which a prefeasibility study is expected to be completed in 2012. In addition, Anfield has received an extension to its Chatala concession that will allow it to further explore and expand the Tres Juanes deposit. A pilot plant to further evaluate and refine the ore upgrading plant design is being designed and will be built within the next five months. In addition, a bulk sample of run of mine and upgraded feed materials will be processed through a rotary kiln electric furnace pilot plant in Brazil to further improve the process design and flowsheet.

Conference Call

Call in details for the conference call to be held on July 7 at 11:00am (Pacific Time) are:

North American toll-free: 1-888-789-9572

International: 1-416-695-7806

Participant Code: 1132147

A replay of this conference call will be available from Thursday, July 7 until Thursday July 21 and will be posted on Anfield's website at www.anfieldnickel.com. The replay numbers are:

North American toll-free: 1-800-408-3053

International: 1-905-694-9451

Pin: 7473353

Anfield Nickel Corp.

David Strang, Chairman

CAUTION REGARDING FORWARD LOOKING STATEMENTS: This news release may contain "forward-looking statements" within the meaning of the applicable Canadian securities legislation. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as "plans", "expects" or "does not expect", "is expected", "budget", "scheduled", "estimates", "forecasts" or "believes", or variations of such words and phrases or state that certain actions, events or results "may", "could", "would" or "will be taken" or "be achieved". Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of Anfield Nickel Corp. to be materially different from those expressed or implied by such forward-looking statements, including but not limited to: risks related to the exploration and potential development of the Company's projects, risks relating to whether the Guatemalan government will deny extensions and reapplications of exploration licenses or an application for an exploitation license, risks related to the loss of licenses, mineral resources and/or exploration licenses with resource targets on them, risks related to governmental expropriation, risks related to the uncertainty of timing of events including the timing scheduled for results of the prefeasibility study and construction of pilot plants for Anfield Nickel Corp.'s operations, risks related to international operations, the actual results of current exploration activities, conclusions of economic evaluations, changes in project parameters as plans continue to be refined, future prices of commodities, as well as those factors discussed in the sections relating to risk factors of our business filed in Anfield Nickel Corp.'s required securities filings on SEDAR. Although Anfield Nickel Corp. has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results to be materially different from those anticipated, described, estimated, assessed or intended.

There can be no assurance that any forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Anfield Nickel Corp. does not undertake to update any forward-looking statements that are incorporated by reference herein, except in accordance with applicable securities laws.

(1) Per nickel mining industry operating costs forecast for 2010 contained in Roskill's Information Services Ltd report - Nickel: Market Outlook to 2014 (Twelfth Edition, 2010).

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Contact Information:

David Strang

Chairman

+ 604 646 1899

+ 604 687 7041 (FAX)

dstrang@anfieldnickel.com

www.anfieldnickel.com