TORONTO, ONTARIO--(Marketwired - Jan. 12, 2015) - Argonaut Gold Inc. (TSX:AR) ("Argonaut", "Argonaut Gold" or the "Company") is pleased to provide updates its Magino and San Agustin projects. Argonaut has received results of the metallurgical test work on three rounds of column testing at various crushing methods and sizes on its 100% owned Magino project located in Ontario, Canada completed by Kappes Cassiday and Associates ("KCA") of Reno, Nevada. Argonaut has also received the results of a Preliminary Economic Assessment ("PEA") for its 100% owned San Agustin gold project, located in Durango, Mexico completed by KCA; Resource Modeling Inc. ("RMI") of Stites, Idaho and Argonaut Gold's management team. Argonaut will file a full technical report in support of the PEA work within 45 days of this announcement. All amounts are in US Dollars unless otherwise stated.

Magino Metallurgical Highlights

KCA conducted three separate series of column leach tests to examine the feasibility of heap leaching Magino lower grade gold mineralization. Bulk samples were tested from stockpiled material remaining from historic underground operations. In addition, a number of composites were prepared from split drill core collected from various locations throughout the resource volume. Column test work conducted at the KCA laboratories provided the following results:

- August 2013 column leach test work on materials varying from run-of-mine ("ROM") size to a crush size of 9.5mm. This resulted in recoveries ranging from 38% on the coarser fraction to 68% on the finer material.

- February 2014 column leach test work on crushed materials ranging from 31.5mm to 12mm resulted in recoveries varying from 40% on the coarser fraction to 61% on the finer crushed material.

- December 2014 column leach test work comparing conventionally crushed material versus high pressure grinding roll (HPGR) crushed material at minus 9.5mm size resulted in recoveries ranging from 62% to 66% for the conventionally crushed material and 68% to 71% on the HPGR material.

McClelland Laboratories Inc. ("MLI") conducted a test program aimed at optimizing the cyanide concentration in leach in order to minimize cyanide consumption. Three sample composites were prepared from split core representing from multiple intervals within the Magino deposit. The three composites selected represent shallow, mid-level and deep mineralization.

- Metallurgical testing on milled material resulted in improved cyanide consumption with a nearly a one third decrease in usage. This should reduce operating costs as cyanide accounted for over 23% of plant operating costs assumed in the previously released January 30, 2014 Magino project pre-feasibility study (the "Prefeasibility Study" or "PFS").

Bob Rose, Vice-President of Technical Services, "We are encouraged by the results from the heap leach and cyanide optimization test work that has been completed on material from the Magino project. Because of these favorable results, we hope to be able to consider different process methods, throughputs and alternatives for this project that may enable us to unlock additional economic potential. The cyanide optimization test work indicates that we can expect a reduction in cyanide consumption on the order of 30%, as compared to what was assumed in the PFS. An even greater reduction in cyanide consumption may be possible by utilizing oxygen sparging during leaching. Given the fact that cyanide represented approximately 23% of the $9.55/t milling cost estimated in the PFS, the importance to the project economics of optimizing the cyanide consumption cannot be understated. These metallurgical test results along with the upcoming drill campaign on the land to be acquired from Richmont Mines Inc. ("Richmont"), may allow us to further optimize the potential of this deposit as we move forward."

For additional information, the complete tables and explanation of methodologies of leach column and cyanide optimization test work can be accessed on the Company's website using the following link: www.argonautgold.com.

Path Forward

Argonaut plans to commence an 8,000 metre drill campaign in January 2015 to both test the extension of the Webb Lake mineralization easterly on the adjacent property to be acquired from Richmont. Drilling will also include testing select portions of the main resource body to fill-in areas where historical drilling was excluded from the most recent resource that was published in December of 2013. This work together with the updated metallurgical results will form the basis for an updated resource estimate which is planned to be released during the second half of 2015.

San Agustin Project PEA Highlights using $1200/ounce gold and $17/ounce silver

- Pre-tax Net Present Value ("NPV") of $101 million using a 5% discount rate

- After tax NPV of $70.2 million using a 5% discount rate.

- After tax Internal Rate of Return ("IRR") of 22%.

- Project has additional upside potential; the phase II drilling information was not incorporated in the current resource used in the PEA.

- Initial estimated $67 million capital expenditure investment including $11.4 million in contingency.

- Very low mine development costs due to the out-cropping deposit.

- Low life-of-mine ("LOM") strip ratio anticipated of 0.4:1 mineralized material to waste.

| San Agustin PEA Results1 | |||||

| LOM (years) | 10.5 | ||||

| Indicated GEO recovered (000's)2 | 541.0 | ||||

| Cash cost per GEO | $ | 670 | |||

| Capital costs: (millions)3 | |||||

| Initial | $ | 67.0 | |||

| Sustaining | $ | 23.4 | |||

| After tax NPV | |||||

| @ 5% discount rate (millions)4 | $ | 70.2 | |||

| After tax Internal Rate of Return ("IRR")4 | 22 | % | |||

| 1 PEA incorporating work by KCA, RMI and Argonaut Gold to be filed within 45 days of this release. | |||||

| 2 Gold equivalent ounces production was calculated at 71:1 conversion using $1,200/oz gold and $17/oz silver | |||||

| 3 Initial capital costs of $67 million including $11.4 million in contingency and $2.7 million in EPCM, as well as $0.5 million in mine development costs and $0.2 million in pre-production costs for the project. | |||||

| 4 NPV and IRR calculations are based on after tax expectations with a long term gold price of $1,200 and silver price of $17.The PEA is preliminary in nature, and there is no certainty that the PEA will be realized. | |||||

Production Specifications

- Total proposed Indicated Resource to be processed includes 72.4 million tonnes containing 746,000 ounces of gold with an average grade of 0.32 grams per tonne ("g/t") and 24.6 million ounces of silver with an average grade of 10.6 g/t.

- No inferred resources were included in the mine or production plan.

- Total contemplated production of 488,000 ounces of gold and 3.8 million ounces of silver from the Indicated Resource.

- Average yearly production of 50,400 gold equivalent ounces during the initial ten years of the mine life.

- Throughput estimate of an average of nearly 7 million tonnes per year from an open-pit mine, with 6 million tonnes processed via two stage crushing and 1 million tonnes via one stage crushing and a recovery process using cyanide heap leaching and carbon adsorption.

| Production Statistics: | |||

| Life of mine (years) | 10.5 | ||

| Total Indicated Resource tonnes processed (000's) | 72,400 | ||

| Total tonnes waste (000's) | 28,600 | ||

| Life of mine strip ratio (waste: mineralized material) | 0.4 | ||

| Overall average gold grade (g/t) | 0.32 | ||

| Overall average silver grade (g/t) | 10.6 | ||

| Overall average gold recovery - 2-stage crushed material | 66 | % | |

| Overall average gold recovery -1-stage crushed material | 57 | % | |

| Overall average silver recovery - 2-stage crushed material | 16 | % | |

| Overall average silver recovery -1-stage crushed material | 9 | % | |

| Gold ounces recovered (000's) | 488 | ||

| Silver ounces recovered (000's) | 3,804 | ||

| Average annual production GEOs (yrs 1-10) | 50,400 | ||

The proposed potential production mine plan utilizes an in-pit resource at a $1,150/ ounce gold price.

| Modeled Operating Costs | ||||

| Cost / Tonne Mineralized Material | $ | 5.01 |

||

| Mining | $ | 1.52 | ||

| Processing | $ | 3.14 | ||

| G&A | $ | 0.35 | ||

| Cash Cost Per GEO | $ | 670 | ||

| Modeled Capital Costs (millions) | |||

| Mine | $ | 4.7 | |

| Process | $ | 37.0 | |

| Infrastructure | $ | 7.7 | |

| Total Capital | $ | 49.4 | |

| Contingency, EPCM, owner & indirect costs | 17.6 | ||

| Total Initial Capital | $ | 67.0 | |

| Sustaining Capital | 23.4 | ||

| Total Life of Mine Capital | $ | 90.4 | |

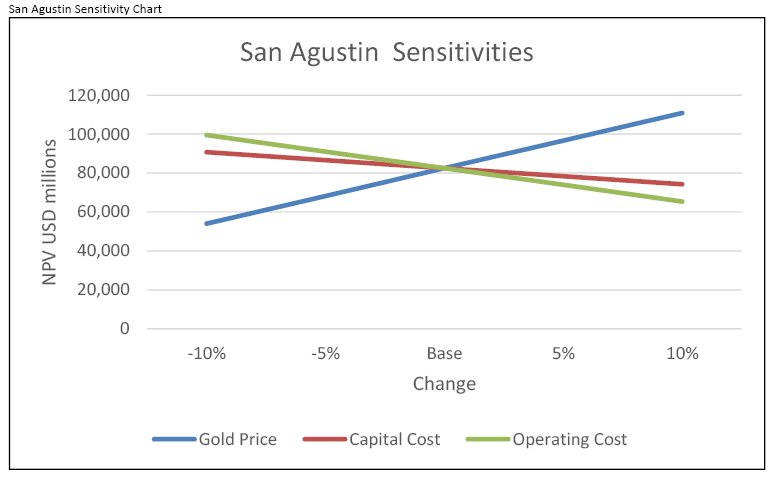

The project sensitivities indicate the project is most sensitive to gold price, followed by operating costs and is less sensitive to changes in capital costs. Additionally, a change in gold price to consensus long-term price of $1,300 per ounce results in an increase in the NPV at a 5% discount rate of $23 million as referenced in the table below.

To view the San Agustin Sensitivity Chart, visit the following link: http://media3.marketwire.com/docs/SanAgustinSensitivityChart.jpg

{kind=link}

| Sensitivity Table (values in USD 000's) | |||||

| -10% | -5% | Base | 5% | 10% | |

| Gold Price | 42,811 | 56,502 | 70,193 | 83,870 | 97,534 |

| Capital Cost | 76,579 | 73,386 | 70,193 | 67,000 | 63,807 |

| Operating Cost | 87,277 | 78,741 | 70,193 | 61,640 | 53,087 |

| Base case uses gold, capital and operating costs as reported in the PEA and this release | |||||

| Sensitivities to Gold Price | ||||||

| NPV1 | IRR | |||||

| Gold price $/oz | $ | 1,100 | $ | 47.4 | 17 | % |

| $ | 1,150 | $ | 58.8 | 19 | % | |

| $ | 1,200 | $ | 70.2 | 22 | % | |

| $ | 1,250 | $ | 81.6 | 24 | % | |

| $ | 1,300 | $ | 93.0 | 27 | % | |

| 1 NPV is stated in millions of US dollars |

Peter Dougherty, President and CEO of Argonaut Gold stated:

"I am pleased with the results achieved in less than one year since acquiring the San Agustin project. We have a project that the PEA show may work in the current challenging environment. The continuity of the deposit speaks to the quality of the project as nearly 90% of the mineralization identified was included in the proposed mine plan. Furthermore, we have drilled over 30,000 metres and have only included roughly 22,000 of those metres in this PEA. We continue to test the extent of the deposit and have identified significant expansion potential for nearly 1.5 kilometres to the northwest of the currently recognized resource. We hope that the close proximity of San Agustin to our El Castillo project should lead to further reductions in capital and operating costs as we seek to share existing infrastructure and personnel. The low proposed strip ratio of the project should allow us to balance fleet requirements and maximize use of existing equipment. We will continue to look at various ways to sensibly grow this project as new drill results become available. We now have an economic assessment that shows a healthy at the gold price that we are currently experiencing. At a gold price of $1,200 per ounce, the project has an IRR of 22% and an after tax NPV of $70.2 million. Of note is that a return to long-term estimated gold price of $1300 per ounce increase the NPV by 35%. The positive economics coupled with the proximity to the El Castillo mine, should allow us to leverage our existing operations and knowledge which should protect us on the downside and provide leverage to any increases in the gold price."

National Instrument 43-101 ("NI 43-101") Preliminary Economic Assessment Report

This PEA is based on the Canadian NI 43-101 mineral resource estimate generated by RMI effective as of July 8, 2014, and presented in a National Instrument 43-101 Technical Report dated October 3, 2014, for Argonaut's San Agustin project which shows an Indicated resource of 845,000 gold ounces and 28,263,000 ounces of silver, based on over 22,000 metres of drilling in 230 holes of drilling contained within 82.2 million tonnes of mineralized material at an average grade of 0.32 grams per tonne gold and 10.7 grams per tonne silver.

Mineral Resource Summary of the San Agustin Project as of July 8, 2014.

| Material Type |

Class | Tonnes of Material (000s) |

Gold Equivalent Grade (g/t) 1,2,3 |

Gold Grade (g/t) |

Silver Grade (g/t) |

Gold Ounces Contained (000s) |

Silver Ounces Contained (000s) |

| Oxide | Indicated | 79,373 | 0.37 | 0.32 | 10.6 | 817 | 27,050 |

| Transition | Indicated | 2,837 | 0.37 | 0.31 | 13.3 | 28 | 1,213 |

| Total | Indicated | 82,210 | 0.37 | 0.32 | 10.7 | 845 | 28,263 |

| Oxide | Inferred | 6,800 | 0.34 | 0.29 | 10.6 | 63 | 2,317 |

| Transition | Inferred | 164 | 0.35 | 0.23 | 26.9 | 1 | 142 |

| Total | Inferred | 6,964 | 0.34 | 0.29 | 11.0 | 65 | 2,459 |

| 1 g/t refers to grams per tonne | |||||||

| 2 New resource based on a 0.18 g/t gold equivalent cut-off grade | |||||||

| 3 The gold equivalent grade for the conceptual pit uses a 65:1 gold equivalent ounce ratio along with the metal recovery ratios achieved in the preliminary metallurgical test work | |||||||

| Notes to Accompany Mineral Resource Table: | |||||||

| 1. Mineral resources are not mineral reserves and do not have demonstrated economic viability. | |||||||

| 2. Inferred mineral resources have a high degree of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. | |||||||

| 3. Mineral resources are reported as undiluted. | |||||||

| 4. Mineral resources are reported within a conceptual pit shell. | |||||||

| 5. The resources are contained within a Lerchs-Grossmann pit shell based on $1,300/oz gold price, $20/oz silver price, mining cost of $1.00 per tonne ("/t") of material mined, process and general and administrative expense cost of $4.22/t with gold recoveries of 68% and silver recoveries of 21%. | |||||||

| 6. Tonnes, grade values, and contained metal quantities may differ due to rounding. | |||||||

| 7. Gold equivalent grade for conceptual pit used gold and silver prices and recovery ratios. | |||||||

The stated Mineral Resources have been prepared in accordance with the CIM classifications of Canada's NI 43-101 Standards of Disclosure for Mineral Projects.

Path forward:

At San Agustin, Argonaut continues to prepare baseline and engineering plans in order to prepare the information required for permitting documentation. These efforts along with continuing to engage the communities, regulators, and various agencies are aimed towards developing a project that will benefit all stakeholders.

Technical Information

Mineral resources referenced herein are not mineral reserves and do not have demonstrated economic viability. Mineral resource estimates do not account for mineability, selectivity, mining loss and dilution. The mineral resource estimates include inferred mineral resources that are normally considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves. There is also no certainty that these inferred mineral resources will be converted to measured and indicated categories through further drilling, or into mineral reserves, once economic considerations are applied.

The Company cautions that a PEA is preliminary in nature and that it relies upon mineral resource estimates which have the considerations noted above applied to them. There is no certainty that the PEA will be realiexed or that any of the resources will ever be upgrated to reserves.

For further information on the San Agustín project please see the technical report titled "Oxide Resource Estimate, San Agustin Project, Durango, Mexico" with an effective date of July 8, 2014 and available on the Company's website or on www.sedar.com under the Company's profile.

For further information on the Magino project please see the "NI 43-101 Preliminary Feasibility Study on the Magino Gold Porject, Ontario, Canada", dated January 30, 2014, on the Company's website or on www.sedar.com under the Company's profile.

Mr. Michael Lechner of RMI located in Stites, Idaho who is an "Independent Qualified Person" as defined by NI 43-101 and the lead person responsible for completing the San Agustín resource has reviewed this press release as it relates to the San Agustín project.

Mr. Carl Defilippi of KCA located in Reno, Nevada who is an "Independent Qualified Person" as defined by NI 43-101 and the lead person responsible for completing the metallurgical work for the new San Agustín resource has reviewed this press release as it relates to the San Agustín project and has overseen the metallurgical and recovery methods, infrastructure, operating costs and capital costs. Mr. Defilippi is also responsible for reviewing the column test results for the Magino project and has reviewed this press release as it relates the to these processes for the Magino project.

Mr. Larry Buter of LBJ Mineral Services LLC located in Highlands Ranch, Colorado who is an "Independent Qualified Person" as defined by NI 43-101 and the lead person responsible for overseeing the cyanide optimization test work for the Magino project and has reviewed this press release as it relates to cyanide optimization results.

The release of this information was approved by Thomas Burkhart, Argonaut Gold's Vice President of Exploration and a Qualified Person under NI 43-101.

About Argonaut Gold

Argonaut is a Canadian gold company engaged in exploration, mine development and production activities. Its primary assets are the production-stage El Castillo Mine in the State of Durango, Mexico, the La Colorada Mine in the State of Sonora, Mexico, the advanced exploration stage San Agustin project in the State of Durango, Mexico, the advanced exploration stage San Antonio project in the State of Baja California Sur, Mexico, and the development stage Magino project located in Ontario, Canada.

Creating Value Beyond Gold

Cautionary Note Regarding Forward-looking Statements

This press release contains certain "forward-looking statements" and "forward-looking information" under applicable Canadian securities laws concerning the business, operations and financial performance and condition of Argonaut Gold Inc. ("Argonaut" or "Argonaut Gold"). Forward-looking statements and forward-looking information include, but are not limited to, statements with respect to estimation of mineral resources at mineral projects of Argonaut; ; the realization of mineral reserve estimates; the timing and amount of estimated future production; economics of production; success of exploration activities; estimated production and mine life of the various mineral projects of Argonaut; the future price of gold and silver; synergies and financial impact of completed acquisitions; the benefits of the development potential of the properties of Argonaut and currency exchange rate fluctuations. Except for statements of historical fact relating to Argonaut, certain information contained herein constitutes forward-looking statements. Forward-looking statements are frequently characterized by words such as "plan," "expect," "project," "intend," "believe," "anticipate", "estimate" and other similar words, or statements that certain events or conditions "may" or "will" occur. Forward-looking statements are based on the opinions and estimates of management at the date the statements are made, and are based on a number of assumptions and subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. Many of these assumptions are based on factors and events that are not within the control of Argonaut and there is no assurance they will prove to be correct.

Factors that could cause actual results to vary materially from results anticipated by such forward-looking statements include variations in metal grades, changes in market conditions, variations in recovery rates, risks relating to international operations, fluctuating metal prices and currency exchange rates, changes in project parameters, the possibility of project cost overruns or unanticipated costs and expenses, labour disputes and other risks of the mining industry, failure of plant, equipment or processes to operate as anticipated.

These factors are discussed in greater detail in Argonaut's most recent Annual Information Form and in the most recent Management Discussion and Analysis filed on SEDAR, which also provide additional general assumptions in connection with these statements. Argonaut cautions that the foregoing list of important factors is not exhaustive. Investors and others who base themselves on forward-looking statements should carefully consider the above factors as well as the uncertainties they represent and the risk they entail. Argonaut believes that the expectations reflected in those forward-looking statements are reasonable, but no assurance can be given that these expectations will prove to be correct and such forward-looking statements included in this press release should not be unduly relied upon. These statements speak only as of the date of this press release. Argonaut undertakes no obligation to update forward-looking statements if circumstances or management's estimates or opinions should change except as required by applicable securities laws.

Although Argonaut has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be anticipated, estimated or intended. Statements concerning mineral reserve and resource estimates may also be deemed to constitute forward-looking statements to the extent they involve estimates of the mineralization that will be encountered if the property is developed.

Contact Information:

Curtis Turner

Corporate Development Officer

(775) 284-4422 x 104

curtis.turner@argonautgoldinc.com

www.argonautgoldinc.com