Contact Information: Media Contact: Michelle Sabolich Atomic PR for Clear Capital (415) 402-0230

Clear Capital Reports 7.3% U.S. Home Price Gains, Softening REO Influences

National Price Gains Continue Positive Climb; Real Estate Owned (REO) Saturation Rates Decline; Los Angeles and Fresno Markets Show Positive Quarterly Price Gains for the First Time Since 2006; and Chicago Achieves Its Largest Quarterly Gain This Decade

| Source: Clear Capital

TRUCKEE, CA--(Marketwire - September 3, 2009) - Clear

Capital™ (www.clearcapital.com), a premium provider of data and

solutions for real estate asset valuation, investment and risk assessment,

today released its Home Data

Index™ (HDI) Market

Report. Patent pending rolling quarter technology significantly reduces the

multi-month lag time associated with other indices to help investors, loan

servicers and individual buyers and sellers make more informed, timely and

profitable decisions. This month's report features data compiled through

August 25, 2009.

Key report highlights include:

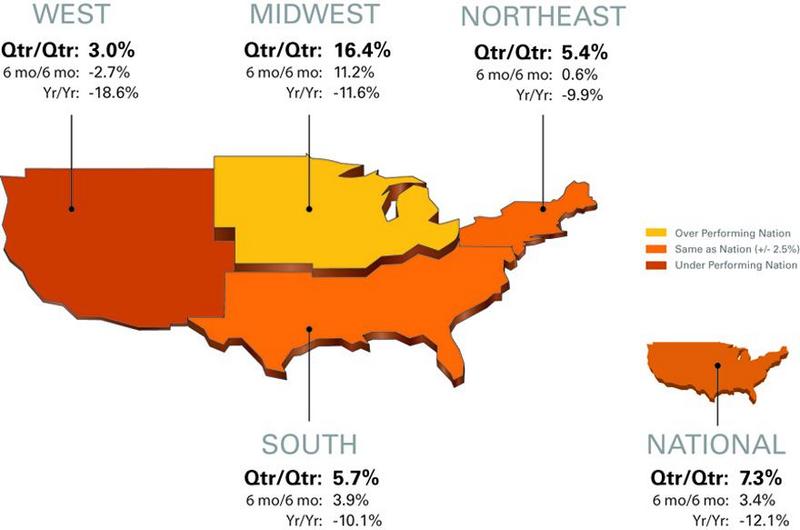

-- National / Four Region Overview: National quarterly price gains reach

7.3 percent, with the Midwest (16.4), South (5.7), Northeast (5.4), and

West (3.0) regions all continuing to post gains. The national REO

saturation rate (percentage of REOs sold to all properties sold in the last

rolling quarter) dropped more than three points since last month's report

to 30.1 percent.

-- Metropolitan Statistical Area (MSA) drilldown: REO saturation

levels decline with 28 of the 30 major markets improving over last month's

rates. Los Angeles and Fresno return first positive quarterly price gains

since mid-2006, while REO properties make up a smaller portion of

California sales.

-- Micro Market Analysis: Up from record lows, the Chicago MSA achieves its

largest quarterly gain this decade (19.9%).

The Clear Capital HDI Market Report offers the industry, investors and

lenders a near real-time look at pricing conditions not only at the

national and metropolitan level, but within local markets. Clear Capital

data is built on the most recent data available from recorder/assessor

offices, and then further enhanced by adding the Company's proprietary

market data for the most comprehensive geographic coverage available.

"The price changes in this month's highest and lowest performing markets

lists speak to the extremely positive summer home buying season -- more

than what can be attributed to seasonality," said Kevin Marshall,

President of Clear Capital.

"While we do expect more REO inventory to hit the market as we close 2009,

this dramatic seasonal price and volume increase in sales of non-REO homes

could create positive momentum going into the normally slow fall and winter

seasons," said Marshall. "Buyers are getting nervous that they are missing

the bottom of the market, so they're choosing to get in the market now.

These factors greatly increase the chances of a springtime recovery next

year."

National/Four Region Market Overview (July 27, 2008 - Aug. 25, 2009)

Distressed sales have outpaced the inflow of new REOs over the

last quarter, softening the downward pressures introduced by REOs and

aiding recent price gains. This reduction in the REO saturation rate

improves the chances short term price gains could extend to robust,

longer-term price stabilization.

The national price gains of 7.3 percent for the most recent rolling quarter

along with this month's 3.2 point drop in REO saturation rates to 30.1

percent suggest improved conditions.

The Midwest, Northeast and South have similar yearly losses, which further

highlight the disparity still present in the REO-saturated West. However,

the West did continue to expand its quarterly price gain to 3.0 percent,

while reducing its quarterly REO saturation rate to 41.9 percent -- a 3.4

point reduction from last month.

Metro Markets (July 27, 2008 - Aug. 25, 2009)

Once again Cleveland earned the highest price gains driven by a shift in

its market's composition. Cleveland's REO saturation rates plummeted from a

late winter record of 58.5 percent to the current level of 35.2 percent.

This reflects a decline in REO sales volume (-29.9%) accompanied by an

82.5% increase in the number of fair market sales when compared to last

rolling quarter. In addition, combined sale volumes grew by 16.6 percent;

and the median sale price jumped from $50,000 to $97,500 over the same

period.

The magnitude of price gains among the rest of the highest performing

markets continues to climb as well. These gains represent a distinct shift

away from the consistently poor market conditions over the past several

years and place many of these markets within striking distance of returning

year-over-year gains.

All but one (St. Louis) of the markets on this month's list saw declining

REO saturation rates over last month's figures, indicating improved

conditions are spreading beyond the REO segment of the market.

Chicago (the subject of this month's micro market analysis) returned to REO

saturation levels the city saw last summer, which is nearly a ten percent

improvement over its peak of 42.3 percent last winter. Similar improvement

in pricing conditions placed Chicago in sixth position among the highest

performing major markets.

The number of major markets on the list with positive quarter-over-quarter

price gains grew to eleven this month. It's important to note that both the

Los Angeles and Fresno markets experienced quarterly gains for the first

time since mid-2006. The REO saturation rates for both of these California

markets also improved 3.1 and 4.1 percent over last month, respectively.

Phoenix, the focus of last month's micro market analysis and among the

longtime leaders of price declines, did not make this month's list with a

4.1 percent price gain for the quarter, and a 3.1 percent drop in REO

saturation to 58.5 percent.

The lowest performing major markets also saw all fifteen markets experience

flat or improving REO saturation rates. The continued growth of positive

price gains might indicate the start of the long process of eroding the

stronghold REO properties have had in many of these markets.

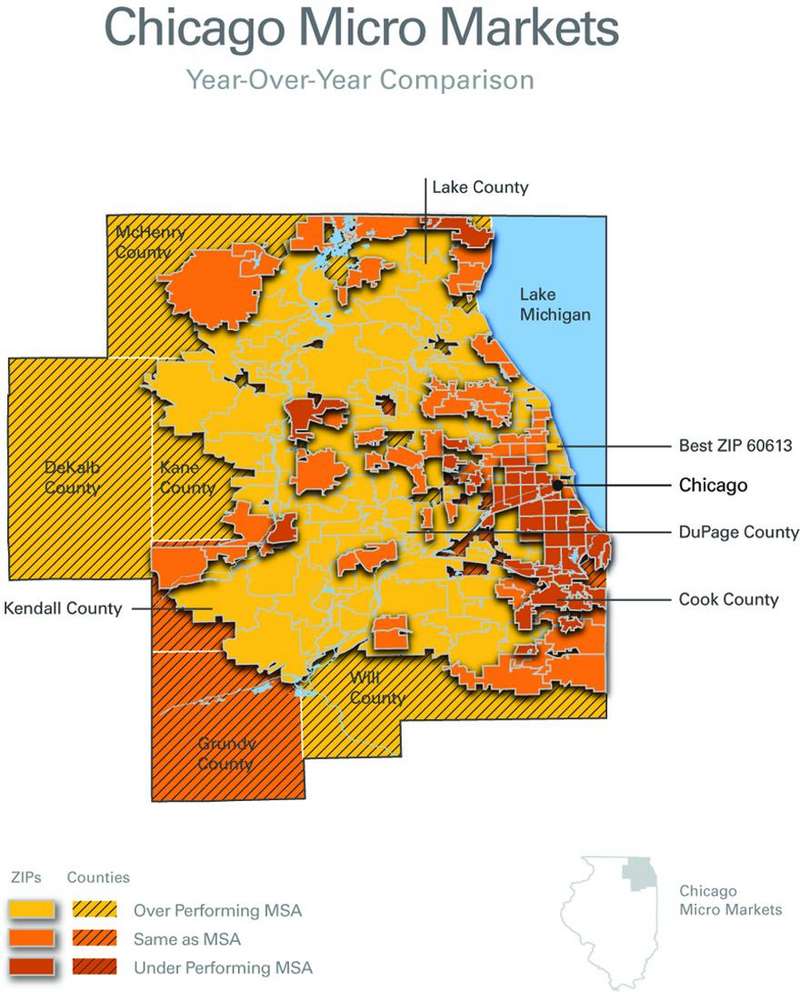

Micro Markets (July 27, 2008 - Aug. 25, 2009)

This section highlights a single market every month with a deeper dive into

how the micro- and macro-markets relate to each other.

Chicago's current quarterly gain is its first in three years. The magnitude

(19.9%) of the gain was large enough to wipe out the losses of last winter,

returning home prices to 2008 holiday season levels. This was Chicago's

second largest quarterly price swing of the decade only surpassed by last

fall's price change of -20.3 percent. This gain is somewhat muted, however,

when put in perspective with Chicago's market at the beginning of this year

when it reached its peak price decline since 2006 (-54.1%). This month's

price increase moved the market 9.1 points in a positive direction to -45.0

percent.

Chicago's yearly losses have generally radiated from the city center out to

the suburbs, mostly avoiding the shores of Lake Michigan. DuPage County

experienced a price change of -13.6 percent over the last year, beating out

neighboring Cook County's -34.8 percent change.

Cook County's Lakeview area that surrounds Wrigley field (ZIP 60613) turned

in a 2.3 percent yearly gain -- the best in the Chicago metropolitan area.

In addition, Lakeview is currently experiencing a modest REO saturation

rate of 5.1 percent. Aside from appealing to sports fans, Lakeview's

quality homes, numerous retail and social locations, and close proximity to

the downtown business core have sustained home prices far better (-2.7%)

than the Chicago MSA (-45.0%) since the market's peak in 2006.

Clear Capital Home Data Index™ Methodology

The Clear Capital Home Data Index (HDI) provides weighted paired sales, and

price-per-square-foot index models that use multiple sale types, including

single-family homes, multi-family homes and condominiums. These models are

combined with an address-level cascade to provide sale-type-specific

analysis for thousands of geographic areas across the country. The indices

include both fair market and institutional (real estate owned)

transactions. They also provide indicators of REO activity such as REO

discount rates, REO days on market and REO saturation. The Clear Capital

HDI generates indices in patent pending rolling quarter intervals that

compare the most recent four months to the previous three months. The

rolling quarters have no fixed start date and can be used to generate

indices as data flows in, or at any arbitrary time period.

About Clear Capital

Clear Capital (www.clearcapital.com) is a premium provider of data and

solutions for real estate asset valuation and risk assessment for large

financial services companies. Our products include appraisals, broker-price

opinions, property condition inspections, value reconciliations, and home

data indices. Clear Capital's combination of progressive technology, high

caliber in-house staff and a well-trained network of more than 40,000 field

experts sets a new standard for accurate, up-to-date and well documented

valuation data and assessments. The Company's customers include 75 percent

of the largest U.S. banks, investment firms and other financial

organizations.

Legend

Address Level Cascade - Provides the most granular market data available.

From the subject property, progressively steps out from the smallest market

to larger markets until data density and statistical confidence are

sufficient to return a market trend.

Home Data Index (HDI) - Major intelligence offering that provides

contextual data augmenting other, human-based valuation tools. Clear

Capital's multi-model approach combines address-level accuracy with the

most current proprietary home pricing data available.

Metropolitan Statistical Area (MSA) - Geographic entities defined by the

U.S. Office of Management and Budget (OMB) for use by Federal statistical

agencies in collecting, tabulating, and publishing Federal statistics.

Paired Sales Model - Weighted linear model based on repeat sales of same

property over time.

Price Per Square Foot (PPSF) Model - Median price movement of sale prices

divided by square footage over a period of time -- most commonly a quarter.

Real Estate Owned (REO) Saturation - Calculates the percentage of REOs sold

as compared to all properties sold in the last rolling quarter.

Rolling Quarters - Patent pending rolling quarters compare the most recent

four months to the previous three months.

The information contained in this report is based on sources that are

deemed to be reliable; however no representation or warranty is made as to

the accuracy, completeness, or fitness for any particular purpose of any

information contained herein. This report is not intended as investment

advice, and should not be viewed as any guarantee of value, condition, or

other attribute.