MUNICH, GERMANY--(Marketwire - Sep 26, 2011) - Companies from developed economies have improved their value-creation performance vis-à-vis their emerging-market rivals, according to a new report by The Boston Consulting Group (BCG). The report, Risky Business: Value Creation in a Volatile Economy, is the thirteenth annual report in BCG's Value Creators series.

Starting from a database of more than 9,000 companies worldwide, the report presents detailed analyses of the total shareholder return (TSR) at 941 companies across 19 major industries for the five-year period from 2006 through 2010. It also identifies the top ten value creators overall, for a subset of large-cap companies, and in each of the industries studied. Among the key findings:

- Of the 192 companies included in this year's global and industry rankings, slightly less than half (46 percent) are located in developing economies -- down from 57 percent last year.

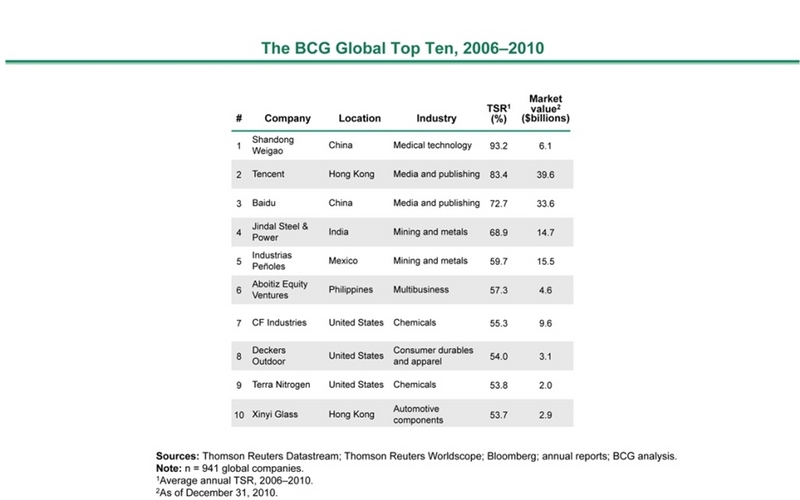

- Seven out of the top ten value creators in the 941-company sample are listed on emerging-market stock exchanges -- four (including the top three companies) in China and Hong Kong, and one each in India, Mexico, and the Philippines. However, whereas last year, all ten of the top value creators were from Asia, this year three U.S. companies join the list: fertilizer manufacturers CF Industries and Terra Nitrogen, and designer and producer of branded footwear and accessories Deckers Outdoor. (See the exhibit "The BCG Global Top Ten, 2006-2010.")

- When it comes to the world's largest companies with market valuations of at least $35 billion, the ratio is reversed, with six out of the top ten large-cap value creators hailing from developed economies -- three from the United States, two from Europe, and one from Canada. (See the exhibit "The BCG Large-Cap Top Ten, 2006-2010.")

Trends in Value Creation

The report also discusses other findings from BCG's analysis of this year's Value Creators database.

- The weighted average annual return for the 941 companies in our sample was 5.9 percent, considerably below the long-term historical average of about 10 percent. Although all 19 industry sectors in our sample delivered positive TSR during the period studied, only 7 were able to meet or beat the sample average. This suggests that while the economic recovery has spread to all sectors, its major impact has been on only a relatively small number of them.

- The big industry winner in this year's rankings is the mining and metals sector, with a weighted average annual TSR of 15.7 percent. This performance is a function of the rise in commodity prices during the 2006-2011 time period, driven in part by rapid development in emerging markets. In second and third place are the machinery industry and consumer nondurables.

- The leading companies in our sample substantially outpaced not only their own industry average but also the total sample average. For example, the average annual TSR of the global top ten (69.8 percent) was more than ten times greater than that of the sample as a whole. The top ten companies in each industry outpaced their industry averages by between 11.4 percentage points (in telecommunications) and 33.3 percentage points (in chemicals). And in every industry we studied, the top ten companies also did substantially better than the overall sample average -- by at least 8.2 percentage points of TSR.

"The lesson for executives is clear," said coauthor Frank Plaschke, a partner in BCG's Munich office. "Coming from a sector with below-average market performance is no excuse. No matter how bad an industry's average performance is relative to other sectors and to the market as a whole, it is still possible for companies in that industry to deliver superior shareholder returns."

The Impact of a Volatile Economy on Value Creation

In addition to analyzing TSR rankings, Risky Business also explores the implications for value creation of increased uncertainty and risk in global equity markets. "High volatility in the macroeconomic environment and in global equity markets is wreaking havoc with established value-creation strategies at many companies," said Daniel Stelter, a senior partner in BCG's Berlin office and a coauthor of the report. "Uncertainty about the evolution of the world economy has thrown into question traditional assumptions about how best to create value."

Risky Business helps senior executives navigate today's complex environment:

- Describing the steps essential for resetting their value-creation strategy in order to take into account new economic and market conditions

- Introducing a thorough but flexible process for translating that strategy into realistic TSR targets and business plans for a company's operating units

- Profiling techniques for managing uncertainty and minimizing risk at a time when more and more investors are looking to invest in companies that deliver low risk and consistent returns

To download a copy of the report, please go to the Publications section of www.bcg.com at: http://www.bcg.com/expertise_impact/publications/default.aspx.

To arrange an interview with one of the authors, please contact Eric Gregoire at +1 617 850 3783 or gregoire.eric@bcg.com.

About The Boston Consulting Group

The Boston Consulting Group (BCG) is a global management consulting firm and the world's leading advisor on business strategy. We partner with clients in all sectors and regions to identify their highest-value opportunities, address their most critical challenges, and transform their businesses. Our customized approach combines deep insight into the dynamics of companies and markets with close collaboration at all levels of the client organization. This ensures that our clients achieve sustainable competitive advantage, build more capable organizations, and secure lasting results. Founded in 1963, BCG is a private company with 74 offices in 42 countries. For more information, please visit www.bcg.com.