VANCOUVER, BRITISH COLUMBIA--(Marketwire - Aug. 14, 2012) - Deans Knight Income Corporation (the "Company") (TSX:DNC) is pleased to release its interim Financial Statements and Management Report of Fund Performance for the period ended June 30, 2012.

These documents can be found on SEDAR at www.sedar.com or the Company's website: www.dkincomecorp.com.

Forward-Looking Statements

This press release contains forward-looking statements. More particularly, this press release contains forward-looking statements concerning the Company's corporate objectives, the investment of the Company's proceeds from the sale of investments previously made, availability of tax losses and deductions, the anticipated total return to the Company's shareholders and the Company's intention to pay out earned income in the form of monthly dividends. Although the Company believes that the expectations reflected in these forward-looking statements are reasonable, undue reliance should not be placed on them because the Company can give no assurance that they will prove to be correct since forward-looking statements address future events and conditions and by their very nature, involve inherent risks and uncertainties. The forward-looking statements contained in this press release are made as of the date hereof and the Company disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

INTERIM MANAGEMENT REPORT

OF FUND PERFORMANCE

For the period from

January 1, 2012 to June 30, 2012

This interim management report of fund performance (the "Report") contains financial highlights of Deans Knight Income Corporation (the "Company"). This Report should be read in conjunction with the interim financial statements of the Company for the six month period ending June 30, 2012 (the "Financial Statements"), which, if not included with this Report, can be obtained at your request, at no cost by emailing info@dkincomecorp.com, visiting our website at www.dkincomecorp.com for contact details or on SEDAR at www.sedar.com. Shareholders may also contact us to request a free copy of the Company's proxy voting policies and procedures, proxy voting disclosure record or quarterly portfolio disclosure.

A Note on Forward-Looking Statements

This Report contains certain forward-looking statements. These statements relate to future events or future performance, including the Company's targeted dividend payout, investment strategy, behaviour of financial markets and reflect the Company's expectations regarding the growth, results of operations, performance and business prospects and opportunities of the Company and its investments. Such forward-looking statements reflect the Company's current beliefs and are based on information currently available to the Company. In some cases, forward-looking statements can be identified by terminology such as "may", "will", "should", "expect", "plan", "anticipate", "believe", "estimate", "predict", "potential", "continue" or the negative of these terms or other comparable terminology. With respect to such forward-looking statements, the Company has made assumptions regarding, among other things, what type of debt securities will be included in its investment portfolio. A number of factors could cause actual events or results to differ materially from the results discussed in the forward-looking statements. In evaluating these statements, prospective investors should specifically consider various factors, including the risks outlined under "Risk Factors" in the AIF (as defined herein), which may cause actual results to differ materially from any forward-looking statement. Although the forward-looking statements contained in the AIF are based upon what the Company believes to be reasonable assumptions, the Company cannot assure investors that actual results will be consistent with these forward-looking statements. Forward-looking statements are made as of the date of this Report and, other than as required by applicable law, the Company assumes no obligation to update or revise them to reflect new events or circumstances.

This Report also contains certain financial and operational information obtained from public sources in respect of certain companies included in the Company's investment portfolio. While management believes this data to be reliable, such information is subject to variations and cannot be verified due to limits on the availability and reliability of data inputs, the nature of the data gathering process and other limitations and uncertainties inherent in such information. Accordingly, the accuracy, currency and completeness of this information cannot be guaranteed. The Company has not independently verified any of the data from third party sources referred to in this Report or ascertained the underlying assumptions relied upon by such sources.

Investment Objective and Strategies

The Company is a closed-end, non-redeemable investment company focused on investing in corporate debt securities. The Company's assets are actively managed by Deans Knight Capital Management Ltd. ("Deans Knight"), a respected British Columbia-based investment firm focused on managing high income and growth mandates for high net worth individuals. Deans Knight, formed in 1992, has an experienced management team and a long history of successful investing in corporate debt securities.

The Company's investment objectives are to: (i) maximize the total return for Shareholders, consisting of dividend income and capital appreciation; and (ii) provide Shareholders (as defined herein) with monthly dividends, which have, to date, been set at $0.0583 per month. The Company intends to achieve these objectives by investing primarily in corporate debt securities rated BBB or below by Standard & Poor's Rating Services or an equivalent rating by another nationally recognized statistical rating organization. The Company may also invest in investment grade debt securities rated above BBB and non-rated debt securities from time to time.

The Company believes there are attractive investment opportunities today in owning corporate debt of businesses with tangible assets, strong cash flows and reasonable leverage.

When evaluating bonds to purchase for the Company, Deans Knight focuses on the following:

- amount of security or collateral within a business to offset the value of the bonds;

- the position of the debt in the capital structure;

- covenants;

- liquidity;

- the business's ability to reduce or refinance the debt; and

- the overall term of the debt and yield to bondholders.

Deans Knight employs the above credit-based analysis to identify corporate debt for inclusion in the Company's investment portfolio with attractive valuations in order to maintain its targeted dividend payment.

Risk

The overall risks of the Company are as described in its annual information form dated March 9, 2012 (the "AIF"). The Company does not believe there have been any changes over the financial period that have affected the overall level of risk associated with an investment in the Company.

Prior to the reorganization and change in business, as discussed in the notes of the Financial Statements, the Company had generated significant tax losses and other tax attributes as a result of its prior businesses and research activities. The Company has recorded, as a tax asset, the full amount of the potential tax benefit of such items to the extent of its projected taxable income. There is no guarantee that the tax authorities will allow the Company to deduct some or all of the tax losses and other attributes. Should the Company be denied the deductions, the recorded amount of the tax assets, as well as such amounts claimed to date, would be recorded as a charge to income. The total tax assets recognized and tax losses and other attributes claimed to date, which are subject to uncertainty, amount to $20,100,000 representing $1.91 per common share at June 30, 2012.

Given the type of investments made by the Company, an investment in the Company may be considered to be speculative. An investment in the Company is generally suitable for investors who are looking to receive income, yet who are willing to tolerate volatility in the value of their investment.

Results of Operations

As per the financial statements, the net assets of the Company at June 30, 2012 were $136,765,643, or $12.98 per common share, compared to $141,539,920, or $13.43 per common share at December 31, 2011. The net assets of the Company consisted of the following components:

| June 30, 2012 | ||||||

| Per common | ||||||

| $ | share(1 | ) | % | |||

| Investments(2) | 127,400,378 | 12.09 | 93.1 | |||

| Cash and short-term deposits | 3,878,758 | 0.37 | 1.8 | |||

| Accrued income | 2,031,791 | 0.19 | 1.3 | |||

| Prepaid expenses | 136,918 | 0.01 | 0.0 | |||

| Future income tax asset(3) | 4,050,000 | 0.38 | 4.1 | |||

| Accounts payable and accrued liabilities | (732,202 | ) | (0.06 | ) | (0.3 | ) |

| 136,765,643 | 12.98 | 100.0 | ||||

| (1) | Based on 10,537,263 common shares, including 10,191,592 voting common shares and 345,671 non-voting common shares, as outlined in the notes to the Financial Statements. |

| (2) | The details of the investments are outlined in the Summary of Investment Portfolio below. |

| (3) | Refer to the Taxation note to the Financial Statements for more detail. |

| December 31, 2011 | ||||||

| Per common | ||||||

| $ | share(1 | ) | % | |||

| Investments(2) | 129,918,543 | 12.33 | 91.8 | |||

| Cash and short-term deposits | 4,997,715 | 0.47 | 3.5 | |||

| Accrued income | 2,339,751 | 0.22 | 1.7 | |||

| Prepaid expenses | 73,151 | 0.01 | 0.0 | |||

| Future income tax asset(3) | 4,920,000 | 0.47 | 3.5 | |||

| Accounts payable and accrued liabilities | (709,240 | ) | (0.07 | ) | (0.5 | ) |

| 141,539,920 | 13.43 | 100.0 | ||||

| (1) | Based on 10,537,263 common shares, including 10,191,592 voting common shares and 345,671 non-voting common shares, as outlined in the notes to the Financial Statements. |

| (2) | The details of the investments are outlined in the Summary of Investment Portfolio below. |

| (3) | Refer to the Taxation note to the Financial Statements for more detail. |

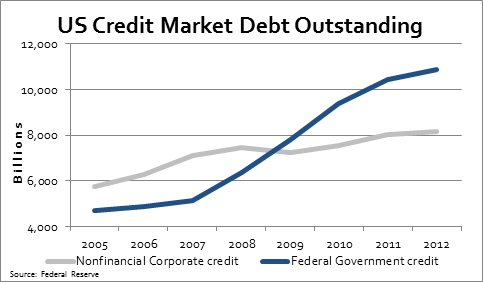

While it is certainly a difficult environment, especially in Europe, the Company strongly believes that corporate bonds will provide attractive future returns. Governments and individuals are saddled with too much debt, and too little tax revenue/income to support that debt. Corporations, on the other hand, have kept debt relatively flat since the financial crisis of 2008/2009, as government balance sheets continue to grow. The graph below shows the increase in U.S. government credit versus corporate credit from 2005 - 2012, as measured by the Federal Reserve. As you will note, corporate credit grew until 2008 and has since tapered off while government debt continues to grow, in fact doubled.

To view the "US Credit Market Debt Outstanding" graph, please visit the following link: http://media3.marketwire.com/docs/814dnc4.jpg.

{kind=link}

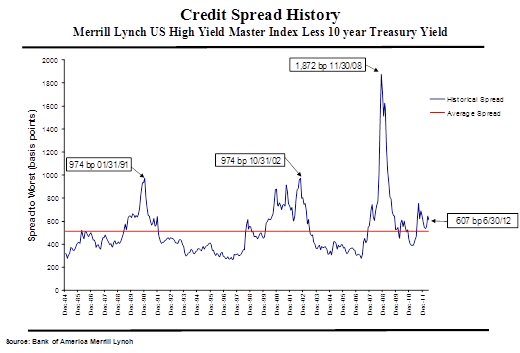

Good management teams understand they are in a difficult environment and have adjusted their cost structures to offset weak growth. Corporations are also de-leveraging or extending the maturity on their debt to provide more financial flexibility in case of a prolonged slow down. In contrast, politicians around the world have failed to make any headway in balancing their budgets, as attempts at reducing spending have so far been fruitless. Despite these facts, spreads between corporate credits and ten-year US treasuries are actually above the long term average.

To view the "Credit Spread History" graph, please visit the following link: http://media3.marketwire.com/docs/814dnc5.jpg.

{kind=link}

With yields on government bonds as low as they are, the Company believes investors are not being compensated for the risk.

With individual companies, the visibility is much clearer. As a corporate debt holder, your main concern is the investee's ability to meet its coupon payments and pay back the principal at maturity. Between the time of issue and maturity, high yield bond prices can fluctuate based on individual company financial results and market sentiment. The Company has no control over this. What we do have control over is ensuring we have invested in businesses that can pay the principal back and if they cannot, we are compensated with adequate collateral. The goal is to provide maximum income to the shareholders with a minimum level of risk. Based on the June 30th share price the dividend yield is 5.5%, from a diversified portfolio consisting of corporate bonds (78.9%), private debt financings (15.2%), and an equity position in Whitecap Resources (5.3%).

The portfolio consists of corporate debt in businesses with good management teams, tangible assets as collateral, strong cash flows and reasonable leverage. Deans Knight uses their credit knowledge and experience in structuring debt securities to evaluate the trust indentures to ensure the Company's interests are protected. The majority of the holdings remained relatively flat so far in 2012. The portfolio was negatively impacted, we believe temporarily, by a few holdings, three of which are discussed below.

Mirabela Nickel Ltd. is a nickel producer with assets in Brazil. As Mirabela has ramped up production over 2011/2012, they have experienced higher than expected costs and, with the decline in nickel prices, their bonds have traded down on liquidity concerns. To ensure Mirabela had adequate liquidity, management raised over $120 million by issuing equity.

They now have $150 million in cash on hand and have successfully reduced cash costs by 18% during the second quarter to $6.03 per pound. Despite this, Mirabela bonds are still priced at a steep discount. At June 30th, Mirabela bonds were yielding 17.5%, an attractive yield given the quality of the mine and where the bonds stand on the capital structure. As such, the Company added to the position during the quarter.

North American Energy Partners ("NAEP") provides a wide range of heavy construction and mining, piling and pipeline installation services to customers in the Canadian oil sands, mineral mining, commercial and public construction and conventional oil and gas markets. NAEP has continued to grow revenue; however, margins were compressed, especially in their pipeline business, which was operating at a loss. New CEO, Martin Ferron, should be a benefit to NAEP as they re-focus the business plan, improving margins. In addition to the ongoing business, the bonds are supported by a valuable heavy equipment asset base. At a yield of 13.1%, we believe bondholders are being compensated for the risk.

We own an equity position in Whitecap Resources Inc., which resulted from the conversion of a private debt financing that Deans Knight designed and funded in September 2009 as part of Whitecap's first financing. Whitecap's common shares had increased in price from the portfolio's conversion cost of $2.88 to $8.29 at December 31 2011, as production grew from 275 barrels of oil equivalent per day ("boepd") at inception in 2009, to 14,500 boepd. The share price has since pulled back to $6.72 at June 30th, because of market anxiety about Europe, China and U.S. growth. Whitecap should grow production to 17,000 boepd by the end of 2012. This could generate more than $230 million in cash flow when the company is worth $1.1 billion today; an attractive valuation in our opinion. Furthermore, Whitecap's high netback, low decline assets lend themselves well to long-term growth regardless of what the oil price is. The Company will continue to hold its investment in Whitecap as we believe management will grow the business, adding shareholder value.

One does not know what will happen to high yield bond prices in the next few quarters or when prices of our investments in Mirabela and NAEP may recover. We do know, at June 30th, the Company's portfolio has a yield to maturity of approximately 8.75% which should be a good predictor of its return over the remaining term of the Company. Given the credit quality of the businesses in the portfolio the Company believes this offers a strong incentive for investors given other income opportunities such as treasury securities, currently yielding less than 1.0%1.

1 Merrill Lynch U.S. Treasury Master Index

Recent Developments

Comparison of net asset value and net assets

National Instrument 81-106 ("NI 81-106") permits investment companies to have two different net asset values: (i) one for financial statements, which will be prepared in accordance with Canadian Generally Accepted Accounting Principles ("GAAP") including Section 3855 (and referred to as "net assets", previously disclosed as "GAAP Net Assets"); and (ii) another for all other purposes, including unit pricing for investor transactions (referred to as "net asset value", previously referred to as "Pricing NAV"). The main difference in calculating net assets and net asset value is that GAAP requires bid price to be used in valuing securities traded in an active market where quoted prices are readily and regularly available, rather than the use of a price between the bid and the ask price currently used for determining net asset value. This difference results in a difference of approximately $0.05 per common share at June 30, 2012, as outlined in the notes to the Financial Statements.

International Financial Reporting Standards

The Company will be required to adopt international financial reporting standards ("IFRS"). The Canadian Accounting Standards Board (AcSB) previously announced January 1, 2011 as the date international financial reporting standards (IFRS) would replace current Canadian standards and interpretations as GAAP for publicly accountable enterprises, which include investment companies.

In December 2011, the AcSB issued a decision to defer adoption of IFRS for investment companies currently applying Accounting Guideline 18 - Investment Companies until years beginning on or after January 1, 2014.

Under the above noted decision, the Company's first set of financial statements to be reported on under IFRS would be for the semi-annual period ending June 30, 2014. These statements would include corresponding comparative financial information for 2013, including an opening statement of net assets as at January 1, 2013. However, the Company has a termination date of April 30, 2014, and as such will not be required to issue statements reported on under IFRS. The Company will continue to monitor any further AcSB decisions that may affect the Company's requirement to adopt IFRS.

Harmonized Sales Tax

The Company is subject to non-recoverable Harmonized Sales Tax on its expenses. The BC Government has announced that the Harmonized Sales Tax will be replaced by the Federal Goods and Services Tax and a Provincial Sales Tax in 2013; however, the legislation has not yet been announced. Accordingly, until further information becomes available the impact cannot be quantified.

Related Party Transactions

The officers, and certain directors, of the Company are also employees of the Investment Advisor, Deans Knight Capital Management Ltd. These officers, and directors, are not paid by the Company. Deans Knight provides investment management services to the Company, as well as administration, financial reporting and other ancillary services required by a publicly listed company. Management fees, for the services outlined above, are computed and paid quarterly, at an annual rate of 1.5% of the net asset value plus applicable taxes, and adjusted for certain non-investment related assets.

For the six month period ended June 30, 2012, management fees totaled $1,147,216 (2011 - $1,165,607). In calculating the amount, the net asset value was reduced by the value of the future income tax asset included in the statement of net assets.

A director of the Company is a partner at a law firm that provides legal services to the Corporation. During the six month period ended June 30, 2012, the Corporation incurred $11,098 (2011 - $17,895) in legal services and disbursements received from this related party. At June 30, 2012, accounts payable and accrued liabilities include $nil (December 31, 2011 - $1,532) to the law firm for legal fees and disbursements, which have not been billed.

Financial Highlights

The following tables show selected key financial information about the Company and are intended to help you understand the Company's financial performance since it began operating its new business of investing in corporate debt in March 2009.

The Company's Net Assets per Common Share (1)

| Period | ||||||||

| March 17 to | ||||||||

| Six months | Year ended | December | ||||||

| ended | December 31, | 31, | ||||||

| June 30, | ||||||||

| 2012 | 2011 | 2010 | 2009 | |||||

| $ | $ | $ | $ | |||||

| Net assets, beginning of period (2)(3) | 13.43 | 13.60 | 12.21 | 9.12 | ||||

| Increase (decrease) from operations(3) | ||||||||

| Total revenue | 0.57 | 1.10 | 0.95 | 0.62 | ||||

| Total expenses | (0.13 | ) | (0.26 | ) | (0.25 | ) | (0.20 | ) |

| Realized gains (losses) for the period | 0.04 | 0.36 | 1.82 | 1.25 | ||||

| Unrealized (losses) gains for the period | (0.50 | ) | (0.52 | ) | (0.27 | ) | 1.21 | |

| Provision for future income taxes | (0.08 | ) | (0.15 | ) | (0.16 | ) | 0.62 | |

| Total (decrease) increase from operations | (0.10 | ) | 0.53 | 2.09 | 3.50 | |||

| Dividends from income (4) | (0.35 | ) | (0.70 | ) | (0.70 | ) | (0.41 | ) |

| Net assets, end of period (5) | 12.98 | 13.43 | 13.60 | 12.21 | ||||

| (1) | The information is derived from the Company's audited annual and unaudited interim financial statements. Common shares outstanding are 10,537,263, including 10,191,592 voting common shares and 345,671 non-voting common shares |

| (2) | Net assets, beginning of the period for 2009 reflect the net assets in the Company at March 17, 2009, after giving effect to the conversion of the convertible debenture and interest owing thereon and the issuance of common shares on the Company's initial public offering less total share issue expenses |

| (3) | Net assets and dividends are based on the actual number of shares outstanding at the relevant time. The increase/decrease from operations is based on the weighted average number of shares outstanding over the period.. |

| (4) | Dividends were paid in cash. |

| (5) | The net assets per share presented in the financial statements differs from the net asset value per share calculated for pricing purposes due to the provisions of CICA Handbook Section 3855. An explanation of the differences can be found in the notes to the financial statements. |

Ratios and Supplemental Data

| Six months ended June 30, |

Year ended December 31, |

Period March 17 to December 31, |

||||||

| 2012 | 2011 | 2010 | 2009 | |||||

| Net asset value (000's) | $137,296 | $142,178 | $143,880 | $128,930 | ||||

| Number of common shares outstanding (000's) | 10,537 | 10,537 | 10,537 | 10,537 | ||||

| Management expense ratio (1) (2) | 1.99 | % | 1.90 | % | 1.91 | % | 5.51 | % |

| Portfolio turnover rate (3) | 8.44 | % | 79.90 | % | 86.60 | % | 36.69 | % |

| Trading expense ratio (4) | 0.01 | % | 0.00 | % | 0.01 | % | 0.01 | % |

| Net asset value per common share | $13.03 | $13.49 | $13.65 | $12.23 | ||||

| Closing market price - common share | $12.62 | $11.84 | $12.54 | $11.40 | ||||

| (1) | Management expense ratio is annualized and based on total expenses for the period and is expressed as an percentage of weekly average net asset values over the period. For 2009, this ratio is calculated from the date the Company began operating its business as an investment corporation, on March 17, 2009, to December 31, 2009. |

| (2) | The Management expense ratio for 2009 includes offering costs for the IPO of $6,268,800 less the offsetting related future tax benefit of $1,692,500. |

| (3) | The Company's portfolio turnover rate indicates how actively the Company manages its portfolio investments. A portfolio turnover rate of 100% is equivalent to the Company buying and selling all of the securities in its portfolio once in the course of the year. The higher a portfolio turnover-rate in a year, the greater the trading costs payable by the Company in the year. There is not necessarily a relationship between a high turnover rate and the performance of the investment portfolio. |

| (4) | The trading expense ratio represents total commissions and other portfolio transaction costs expressed as an annualized percentage of daily average net asset value during the period. |

Management Fees

Deans Knight provides investment management services to the Company, as well as administration, financial reporting and other ancillary services required by a publicly listed company. Management fees are computed and paid quarterly, at an annual rate of 1.5% of the net asset value plus applicable taxes, and adjusted for certain non-investment related assets.

Past Performance

This section shows the Company's past performance, since it began operating its business as an investment corporation. The past performance information includes changes in net asset value and assumes the reinvestment of all dividends paid to common shareholders. It is important to note that the past performance will not necessarily indicate what performance in the future will be.

Year-by-year returns

The accompanying bar chart shows the Company's performance for the periods shown and illustrates how the Company's

performance has changed from period to period. The bar chart shows, in percentage terms, how much an investment made when it began its operation as an investment corporation, March 17, 2009 to December 31, 2009, how much an investment made for the years ended December 31, 2010 and 2011, and how much an investment made for the six- month period ending June 30, 2012.

To view the "Year-by-year returns" chart, please visit the following link: http://media3.marketwire.com/docs/814dnc10.jpg.

{kind=link}

| Summary of Investment Portfolio | ||||

| Top 25 Investments | % of Net | |||

| Asset Value | ||||

| PARAMOUNT RESOURCES | 8.250 | % | 13-Dec-17 | 6.8 |

| STONE ENERGY CORP | 8.625 | % | 1-Feb-17 | 6.6 |

| NORTH AMERICA ENERGY | 9.125 | % | 7-Apr-17 | 5.5 |

| CCS INC | 11.000 | % | 15-Nov-15 | 5.3 |

| MIRABELA NICKEL LTD | 8.750 | % | 15-Apr-18 | 5.1 |

| WHITECAP RESOURCES | N/A | N/A | 4.9 | |

| SOUTHERN PACIFIC RES | 10.750 | % | 7-Jan-16 | 4.4 |

| CALFRAC HOLDINGS LP | 7.500 | % | 1-Dec-20 | 4.2 |

| RAPIDEYE CANADA | 5.000 | % | 31-Aug-14 | 3.8 |

| TEMBEC INDUSTRIES | 11.250 | % | 15-Dec-18 | 3.7 |

| NORTHLAND RESOURCES | 13.000 | % | 6-Mar-17 | 3.5 |

| MERCATOR MINERALS | 7.000 | % | 3-Jan-13 | 3.3 |

| PERPETUAL ENERGY INC | 8.750 | % | 15-Mar-18 | 3.1 |

| PETROAMERICA OIL | 11.500 | % | 31-Mar-15 | 2.9 |

| SHERRITT INTL CORP | 8.000 | % | 15-Nov-18 | 2.9 |

| CARA OPERATIONS LTD | 9.125 | % | 1-Dec-15 | 2.6 |

| CONIFEX TIMBER INC | 10.000 | % | 31-Dec-12 | 2.2 |

| GATEWAY CASINOS | 8.875 | % | 15-Nov-17 | 2.2 |

| BEAZER HOMES USA | 9.125 | % | 15-Jun-18 | 2.1 |

| BLACK PRESS GROUP | 100.000 | % | 4-Feb-14 | 2.0 |

| GARDA WORLD SECURITY | 9.750 | % | 15-Mar-17 | 1.9 |

| PACIFIC RUBIALES | 7.250 | % | 12-Dec-21 | 1.9 |

| SKYLINK AVIATION INC | 12.250 | % | 15-Mar-16 | 1.8 |

| SURE ENERGY | 6.250 | % | 21-Jan-14 | 1.8 |

| WESTERN ENERGY SVS | 7.785 | % | 30-Jan-19 | 1.7 |

| Portfolio Composition | % of Net |

| Asset Value | |

| Fixed Income | |

| Canadian denominated in CAD | 45.4 |

| Canadian denominated in USD | 20.5 |

| United States denominated in USD | 17.1 |

| Other Foreign denominated in USD | 3.5 |

| 86.5 | |

| Convertible Debentures | |

| Other Foreign denominated in AUD | 1.1 |

| 87.6 | |

| Equity and Warrants | 5.5 |

| Investment Portfolio | 93.1 |

| Cash & Short-term Deposits | 2.8 |

| Other Net Assets | 4.1 |

| 100.0 | |

| Sector Breakdown | |

| Energy | 51.5 |

| Materials & Metals | 16.1 |

| Consumer Discretionary | 8.8 |

| Forestry | 7.0 |

| Industrial/Manufacturing | 4.1 |

| Technology | 3.8 |

| Services | 1.8 |

| Financial Services | - |

| Investment Portfolio | 93.1 |

| Cash & Short-term Deposits | 2.8 |

| Other Net Assets | 4.1 |

| 100.0 |

| Deans Knight Income Corporation |

| Financial Statements |

| June 30, 2012 |

| (Unaudited) |

| Deans Knight Income Corporation |

| Statements of Net Assets |

| (Unaudited) |

| June 30, | December 31, | |

| 2012 | 2011 | |

| $ | $ | |

| Assets | ||

| Current | ||

| Investments - at fair value (cost - June 30, 2012 - $ 128,269,140; December 31, 2011 - $125,475,983) | 127,400,378 | 129,918,543 |

| Cash and cash equivalents | 3,878,758 | 4,997,715 |

| Accrued interest receivable | 2,031,791 | 2,339,751 |

| Prepaid expenses | 136,918 | 73,151 |

| Future income tax benefits (note 7) | 2,310,000 | 2,180,000 |

| 135,757,845 | 139,509,160 | |

| Non-current | ||

| Future income tax benefits (note 7) | 1,740,000 | 2,740,000 |

| 137,497,845 | 142,249,160 | |

| Liabilities | ||

| Accounts payable and accrued liabilities (note 5) | 732,202 | 709,240 |

| Net Assets | 136,765,643 | 141,539,920 |

| Shareholders' Equity | ||

| Common shares (note 3) | 99,366,429 | 99,366,429 |

| Contributed surplus (note 3) | 9,904,504 | 9,904,504 |

| Retained earnings (note 4) | 27,494,710 | 32,268,987 |

| 136,765,643 | 141,539,920 | |

| Number of common shares outstanding (note 3) | 10,537,263 | 10,537,263 |

| Net assets per common share (notes 7 and 10) | 12.98 | 13.43 |

| Contingencies (notes 1 and 7) | ||

| Commitments (notes 1 and 9) | ||

| Subsequent events (note 11) | ||

| The accompanying notes are an integral part of these financial statements. |

| Deans Knight Income Corporation |

| Statements of Operations |

| Six-month period ended June 30, 2012 and 2011 |

| (Unaudited) |

| 2012 | 2011 | ||||

| $ | $ | ||||

| Investment income | |||||

| Interest and other | 6,050,208 | 5,459,044 | |||

| Expenses | |||||

| Management fees (note 5) | 1,147,216 | 1,165,607 | |||

| Public company reporting costs | 88,938 | 93,067 | |||

| Director's fees and expenses | 77,913 | 87,086 | |||

| Audit, accounting and tax fees | 42,600 | 37,043 | |||

| Custodial fees | 23,379 | 24,607 | |||

| Transaction costs | 11,318 | - | |||

| Legal fees (note 5) | 11,098 | 17,895 | |||

| Independent Review Committee Fees | 4,500 | 4,500 | |||

| 1,406,962 | 1,429,805 | ||||

| Net investment income | 4,643,246 | 4,029,239 | |||

| Realized and unrealized gains (losses) on investments | |||||

| Net realized gain on securities sold (note 6) | 953,729 | 2,064,001 | |||

| Net realized (loss) gain on settlement of foreign currency contracts | |||||

| (note 6) | (503,995 | ) | 2,203,559 | ||

| Change in unrealized depreciation on investments | (6,199,089 | ) | (4,457,177 | ) | |

| Unrealized appreciation on foreign currency contracts | 887,767 | 611,610 | |||

| Net (loss) gain on investments | (4,861,588 | ) | 421,993 | ||

| (Decrease) increase in net assets from operations before tax | (218,342 | ) | 4,451,232 | ||

| Provision for future income tax (note 7) | (870,000 | ) | (680,000 | ) | |

| (Decrease) increase in net assets from operations | (1,088,342 | ) | 3,771,232 | ||

| (Decrease) increase in net assets from operations per weighted average common share (note 2) | (0.10 | ) | 0.36 | ||

| The accompanying notes are an integral part of these financial statements. |

| Deans Knight Income Corporation |

| Statements of Changes in Net Assets |

| Six-month period ended June 30, 2012 and 2011 |

| (Unaudited) |

| 2012 | 2011 | |||

| $ | $ | |||

| (Decrease) increase in net assets from operations | (1,088,342 | ) | 3,771,232 | |

| Dividends to common shareholders (notes 4 and 9) | (3,685,935 | ) | (3,685,935 | ) |

| (Decrease) increase in net assets during the period | (4,774,277 | ) | 85,297 | |

| Net assets - Beginning of period | 141,539,920 | 143,343,361 | ||

| Net assets - End of period | 136,765,643 | 143,428,658 | ||

| The accompanying notes are an integral part of these financial statements. |

| Deans Knight Income Corporation |

| Statements of Cash Flows |

| Six-month period ended June 30, 2012 and 2011 |

| (Unaudited) |

| 2012 | 2011 | |||||

| $ | $ | |||||

| Cash flows from operating activities | ||||||

| (Decrease) increase in net assets from operations | (1,088,342 | ) | 3,771,232 | |||

| Items not affecting cash | ||||||

| Net realized gain on securities sold | (953,729 | ) | (2,064,001 | ) | ||

| Net realized loss (gain) on settlement of foreign currency contracts | 503,995 | (2,203,559 | ) | |||

| Change in unrealized depreciation on investments | 6,199,089 | 4,457,177 | ||||

| Unrealized appreciation on foreign exchange contracts | (887,767 | ) | (611,610 | ) | ||

| Future income tax provision | 870,000 | 680,000 | ||||

| 4,643,246 | 4,029,239 | |||||

| Cost of investments purchased (note 6) | (13,398,699 | ) | (40,887,826 | ) | ||

| Proceeds from investments sold (note 6) | 11,055,277 | 36,200,473 | ||||

| Net change in non-cash balances related to operations | ||||||

| Accrued interest receivable | 307,960 | (79,949 | ) | |||

| Prepaid expenses | (63,768 | ) | (68,497 | ) | ||

| Accounts payable and accrued liabilities | 22,962 | (26,751 | ) | |||

| 2,566,978 | (833,311 | ) | ||||

| Cash flows from financing activities | ||||||

| Dividends paid to common shareholders (note 4) | (3,685,935 | ) | (3,685,935 | ) | ||

| (3,685,935 | ) | (3,685,935 | ) | |||

| Net decrease in cash during the period | (1,118,957 | ) | (4,519,246 | ) | ||

| Cash and cash equivalents - Beginning of period | 4,997,715 | 7,137,967 | ||||

| Cash and cash equivalents - End of period | 3,878,758 | 2,618,721 | ||||

| Cash and cash equivalents comprise | ||||||

| Cash | 3,878,758 | 2,618,721 | ||||

| Short-term deposits | - | - | ||||

| 3,878,758 | 2,618,721 | |||||

| The accompanying notes are an integral part of these financial statements. |

| Deans Knight Income Corporation |

| Statement of Investments |

| As at June 30, 2012 |

| (Unaudited) |

| Percentage | ||||

| of total | ||||

| Par value 1 | Average cost ² | Fair value ² | fair value 3 | |

| $ | $ | $ | % | |

| Fixed income - Canadian | ||||

| Denominated in Canadian dollars | ||||

| Black Press Group 10.00% 02-04-2014 | 2,750,000 | 2,750,000 | 2,769,250 | 2.2 |

| Cara Operations Ltd. 9.13% 12-01-2015 | 3,500,000 | 3,500,000 | 3,574,375 | 2.8 |

| Conifex Timber Inc. 10.00% 12-31-2012 4 | 3,000,000 | 3,000,000 | 3,000,000 | 2.4 |

| Garda World Security 9.75% 03-15-2017 | 3,250,000 | 3,237,405 | 3,400,313 | 2.7 |

| Gateway Casinos 8.88% 11-15-2017 | 2,750,000 | 2,816,875 | 2,935,625 | 2.3 |

| Mercator Minerals 7.0% 01-03-2013 4 | 4,500,000 | 4,500,000 | 4,500,000 | 3.5 |

| North American Energy Partners Inc. 9.13% 04-07-2017 | 8,750,000 | 8,793,125 | 7,470,313 | 5.9 |

| Paramount Resources 8.25% 12-13-2017 | 9,250,000 | 9,250,000 | 9,319,375 | 7.3 |

| Perpetual Energy Inc. 8.75% 03-15-2018 | 5,000,000 | 5,000,000 | 4,275,000 | 3.4 |

| Petroamerica Oil 11.5% 03-31-2015 4 | 4,000,000 | 4,000,000 | 4,000,000 | 3.1 |

| RapidEye Canada 5.00% 08-31-2014 4 | 5,281,250 | 5,281,250 | 5,281,250 | 4.2 |

| Sherritt International Corp. 7.75% 10-15-2015 | 196,000 | 152,233 | 207,760 | 0.2 |

| Sherritt International Corp. 8.00% 11-15-2018 | 3,750,000 | 3,750,000 | 3,956,250 | 3.1 |

| Skylink Aviation Inc. 12.25% 03-15-2016 | 5,450,000 | 5,357,250 | 2,507,000 | 2.0 |

| Sure Energy 6.25% 01-21-2014 4 | 2,500,000 | 2,500,000 | 2,500,000 | 2.0 |

| Western Energy 7.88% 01-30 -2019 | 2,250,000 | 2,250,000 | 2,278,125 | 1.8 |

| 66,137,838 | 61,974,636 | 48.9 | ||

| Denominated in US dollars | ||||

| CCS Inc. 11.00% 11-15-2015 | 7,100,000 | 3,554,052 | 7,307,966 | 5.7 |

| Mirabela Nickel Ltd. 8.75% 04-15-2018 | 10,050,000 | 9,138,320 | 7,066,949 | 5.6 |

| Pacific Rubiales Energy Corp. 7.25% 12-12-2021 | 2,300,000 | 2,365,780 | 2,563,673 | 2.0 |

| Southern Pacific Resources Libor+8.5% 07-01-2016 | 5,910,000 | 5,838,394 | 6,022,881 | 4.7 |

| Tembec Industries 11.25% 12-15-2018 | 5,000,000 | 5,287,975 | 5,025,437 | 3.9 |

| 26,184,521 | 27,986,906 | 21.9 | ||

| Total Canadian fixed income | 92,322,359 | 89,961,542 | 70.8 | |

| (1) | Par values are presented in their source currency |

| (2) | All amounts are shown in Canadian dollars |

| (3) | Percentages are shown as a percentage of total investments |

| (4) | These investments represent loans receivable |

| The accompanying notes are an integral part of these financial statements. |

| Deans Knight Income Corporation |

| Statement of Investments…continued |

| As at June 30, 2012 |

| (Unaudited) |

| Par value 1 | Average cost² |

Fair value ² |

Percentage of total fair value 3 |

|

| $ | $ | $ | % | |

| Fixed income - United States | ||||

| Denominated in US dollars | ||||

| Abitibibowater 10.25% 10-15-2018 | 1,390,000 | 1,433,090 | 1,575,911 | 1.2 |

| Beazer Homes USA, Inc. 9.13% 06-15-2018 | 3,250,000 | 3,327,056 | 2,856,665 | 2.2 |

| Calfrac Holdings LP 7.5% 12-01-2020 | 6,000,000 | 6,130,329 | 5,778,297 | 4.5 |

| McMoRan Exploration Co. 11.88% 11-15-2014 | 2,000,000 | 2,114,471 | 2,106,989 | 1.7 |

| Number Merger Sub 11.00% 12-15-2019 | 1,850,000 | 1,926,584 | 2,031,448 | 1.6 |

| Stone Energy Corp. 8.63% 2-01-2017 | 8,750,000 | 8,821,638 | 9,028,589 | 7.1 |

| Total United States fixed income | 23,753,168 | 23,377,899 | 18.3 | |

| Total fixed income | 116,075,527 | 113,339,441 | 89.1 | |

| Convertible debentures - International | ||||

| Denominated in Australian dollars | ||||

| Western Areas NL 8.0% 07-02-2012 | 1,500,000 | 1,322,277 | 1,564,650 | 1.2 |

| Denominated in US dollars | ||||

| Northland Resources 13.0% 03-06-2017 | 4,750,000 | 4,678,275 | 4,768,114 | 3.7 |

| 6,000,552 | 6,332,764 | 4.9 | ||

| Equities | ||||

| Conifex Timber Inc.- purchase warrants | 81,250 | - | 20,816 | 0.0 |

| Petroamerica Oil - purchase warrants | 400 | - | 60,918 | 0.1 |

| Sure Energy Inc.- purchase warrants | 625,000 | - | 2,606 | 0.0 |

| Whitecap Resources Inc.- common shares | 1,005,367 | 6,193,061 | 6,756,066 | 5.3 |

| 6,193,061 | 6,840,406 | 5.4 | ||

| Investments subtotal | 128,269,140 | 126,512,611 | 99.4 | |

| Hedges | ||||

| Denominated in US dollars | ||||

| Foreign currency exchange contracts (note 8) | 60,000,000 | - | 887,767 | 0.6 |

| 128,269,140 | 127,400,378 | 100.0 | ||

| (1) | Par values are presented in their source currency |

| (2) | All amounts are shown in Canadian dollars |

| (3) | Percentages are shown as a percentage of total investments |

| (4) | These investments represent loans receivable |

| The accompanying notes are an integral part of these financial statements. |

| Deans Knight Income Corporation |

| Notes to Financial Statements |

| June 30, 2012 |

| (Unaudited) |

1 Nature of operations and basis of presentation

Deans Knight Income Corporation (the "Company") is a corporation continued under the laws of Canada on April 11, 2001. The Company is a closed-end, non-redeemable investment company. It invests, primarily, in corporate debt rated BBB or below by recognized credit rating organizations.

Prior to its reorganization in May 2008, the Company was a life sciences company involved in the research, development and commercialization of innovative products for the prevention and treatment of life-threatening diseases. Forbes Medi-Tech Inc ("Forbes"), who now carries on the prior business of the Company, has provided an indemnity to the Company with respect to liabilities relating to the Company's assets transferred to Forbes and the Company's prior business. In addition, Forbes obtained, on behalf of the Company, product liability insurance for certain claims that may arise in the future in connection with the Company's prior business. To date, no such claims or potential claims have arisen. There can be no assurance that the above noted guarantee will be sufficient to cover any future claims. In March 2009, the Company completed an initial public offering, whereby it raised gross proceeds of $100,368,900 and began operating its new business as an investment company.

The common shares of the Company will be redeemed on, or around, April 30, 2014, for a cash amount equal to 100% of the net asset value per share.

The accompanying financial statements are prepared in accordance with Part V of the Canadian Institute of Chartered Accountants Handbook, Pre-Changeover Accounting Standards (GAAP). All amounts are presented in Canadian dollars, unless otherwise noted.

2 Summary of significant accounting policies

The following is a summary of significant accounting policies followed by the Company, and these policies are consistent with the most recent annual financial statements. These statements should be read in conjunction with the most recent annual financial statements.

Financial instruments

Investments

Investments are held for trading and are recorded at fair values determined as follows:

Fixed income investments

Fixed income investments traded on a public securities exchange or traded on an over-the-counter market are valued at the closing bid price. Where no closing bid price is available, the last sale or close price is used where, in management's opinion, this provides the best estimate of fair value.

Unlisted or non-exchange traded investments, or investments where a last bid, sale or close price is unavailable, or investments for which market quotations are, in the Company's opinion, inaccurate, unreliable, or not reflective of all available material information, are valued at their fair value as determined by the Company using appropriate and accepted industry valuation techniques including valuation models. The fair value determined using valuation models requires the use of inputs and assumptions based on observable market data including volatility and other applicable rates or prices. In certain circumstances, the fair value may be determined using valuation techniques that are not supported by observable market data.

The resulting values for investments not traded in an active market may differ from values that would be determined had a ready market existed, and the difference could be significant.

Forward currency contracts

Forward currency contracts are recorded at fair value. The proceeds (payments) on contracts settled during the six-month period are included in the net realized (loss) gain on settlement of foreign currency contracts (note 6). The Company's policy is to hedge 95% - 105% of the fair value of foreign denominated investments with foreign exchange forward sell contracts.

Public company equities

Publicly traded equities are recorded at bid prices as quoted on recognized stock exchanges.

The amounts at which the Company's publicly-traded investments could be disposed of currently may differ from carrying value based on market quotes, as the value at which significant ownership positions are sold is often different than the quoted market price due to a variety of factors such as premiums paid for large blocks or discounts due to illiquidity.

Warrants

Warrants are recorded at their estimated fair value, using appropriate and accepted industry valuation techniques.

The impact of changes in fair value on net income of the Company arising from changes in estimated fair value for investments is recorded in the statement of operations.

Cash and cash equivalents

Cash and cash equivalents are accounted for at amortized cost. They consist of cash and deposits with maturities, at the time of purchase, of three months or less and are held with a Canadian chartered bank.

Accrued interest receivable

Accrued interest is designated as loans and receivables and is accounted for at amortized cost. Due to the immediate and short-term nature, carrying value approximates fair value.

Financial liabilities

Financial liabilities, consisting of accounts payable and accrued liabilities, are designated as other financial liabilities and are accounted for at amortized cost. Due to the immediate and short-term nature, carrying value approximates fair value.

Investment transactions

Investment transactions are recorded on the trade date. Transaction costs are incremental costs that are directly attributable to the acquisition, issue or disposal of an investment, which include fees and commissions paid to agents, advisors, brokers and dealers, levies by regulatory agencies and securities exchanges, and transfer taxes and duties. These costs are expensed and are included in the statement of operations.

Income recognition

Income from investments is recognized on an accrual basis. Interest income is accrued based on the number of days the investment is held during the year. Royalty income is recognized on an accrual basis as earned. Gains or losses on the sale of investments, including foreign exchange gain or loss on such investments, are calculated on an average cost basis.

Forward foreign currency contracts

Forward foreign currency contracts (note 6) entered into by the Company are valued at an amount that is equal to the gain or loss that would be realized if the position were to be closed out, which is equivalent to the difference between the deliverable asset and the value of the asset to be received. Changes in the value of a forward contract or the assets deliverable under such a contract are included as unrealized appreciation/depreciation of foreign currency contracts in the statement of operations.

Foreign exchange

Assets and liabilities denominated in foreign currencies are translated into Canadian dollars at the exchange rate applicable on the valuation date. Purchases and sales of investments, investment income and expenses are calculated at the exchange rates prevailing on the dates of the transactions.

Income taxes

The Company follows the asset and liability method of accounting for income taxes. Future income tax assets and liabilities are measured using rates expected to apply to the taxable income in the years in which the temporary differences are expected to be settled. The Company accounts for uncertain tax positions using the contingent liability model, whereby a provision is established only where it is likely that a payment will be required to be made.

A valuation allowance is recognized to the extent that it is more likely than not future income tax assets will not be realized. Management has estimated the income tax provision and future income tax balances taking into account its expectation of future taxable income and an interpretation of the various income tax laws and regulations. It is possible, due to the complexity inherent in estimating income taxes, that the tax provision and future tax balances could change (note 7), and the change could be significant.

Use of estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, income and expenses. Actual results could differ from those reported and such differences could be material. Significant areas involving the use of estimates include determining the estimated fair value of investments and future income tax assets.

Net assets per common share

The net assets per common share is computed by dividing the net assets of the Company by the total number of common shares outstanding on the balance sheet date.

(Decrease) increase in net assets from operations per weighted average common share

The (decrease) increase in net assets from operations per common share represents the decrease/increase in net assets from operations divided by the weighted average number of common shares outstanding during the period.

The weighted average number of shares outstanding during the six-month period ended June 30, 2012 was 10,537,263 (June 30, 2011 - 10,537,263). This weighted average includes both the voting common shares and non-voting common shares of the Company.

3 Capital stock

The Company is authorized to issue an unlimited number of voting common shares without par value, and an unlimited number of non-voting common shares without par value.

There have been no changes in the number of voting and non-voting common shares for the periods ended June 30, 2011 and June 30, 2012.

The total shares outstanding are summarized as follows:

| June 30, 2012 | December 31, 2011 | |||||||

| Number of | Amount | Number of | Amount | |||||

| Shares | $ | Shares | $ | |||||

| Voting common shares | 10,191,592 | 96,273,343 | 10,191,592 | 96,273,343 | ||||

| Non-voting common shares | 345,671 | 3,093,086 | 345,671 | 3,093,086 | ||||

| Total common shares outstanding | 10,537,263 | 99,366,429 | 10,537,263 | 99,366,429 | ||||

Contributed surplus

The contributed surplus balance did not change during the six-month period, and consists of:

| June 30, | December 31, | |

| 2012 | 2011 | |

| $ | $ | |

| Surplus related to stock compensation, warrants and options associated with common shares | 8,030,295 | 8,030,295 |

| Surplus relating to warrants associated with previously issued preferred shares | 1,874,209 | 1,874,209 |

| 9,904,504 | 9,904,504 | |

4 Retained earnings

The changes in retained earnings for the six-month period ended June 30 were as follows:

| 2012 | 2011 | |||

| $ | $ | |||

| Retained earnings - opening balance | 32,268,987 | 34,072,428 | ||

| (Decrease) increase in net assets from operations | (1,088,342 | ) | 3,771,232 | |

| Dividends paid from net investment income | (3,685,935 | ) | (3,685,935 | ) |

| Retained earnings - closing balance | 27,494,710 | 34,157,725 |

5 Related party transactions and balances

Management fees are paid quarterly to Deans Knight Capital Management Ltd. (the Investment Advisor), a corporation with certain common directors and officers of the Company, for services received in connection with the management of the investment portfolio and financial accounts, among other services provided.

Management fees are computed quarterly at an annual rate of 1.5% of net asset value, adjusted for certain non- investment related assets. For the six-month period ended June 30, 2012, management fees (including applicable taxes) totalled $1,147,216 (June 30, 2011 - $1,165,607). At June 30, 2012, $595,000 (December 31, 2011 - $575,224) was owed to the Investment Advisor, which was included in accounts payable and accrued liabilities in the statement of net assets and is payable immediately.

A director of the Company is a partner at a law firm that provides legal services to the Company. During the six-month period ended June 30, 2012, the Company incurred $11,098 (June 30, 2011 - $17,895) in legal services and disbursements received from this related party. At June 30, 2012, accounts payable and accrued liabilities include $nil (December 31, 2011 - $4,185) due to the law firm for legal fees and disbursements.

6 Net realized gains on investments sold and foreign currency contracts

The net realized gain on sale of investments for the six-month period ended June 30 was as follows:

| 2012 | 2011 | |||

| $ | $ | |||

| Proceeds from sale of investments | 11,055,277 | 36,200,473 | ||

| Investments at cost - Beginning of period | 125,475,983 | 118,563,957 | ||

| Add: Cost of investments purchased | 13,398,699 | 40,887,826 | ||

| 138,874,682 | 159,451,783 | |||

| Less: Investments at cost - End of period | (128,269,140 | ) | (127,518,870 | ) |

| Cost of investments sold | 10,605,542 | 31,932,037 | ||

| Net realized gain on investments sold | 449,734 | 4,267,560 | ||

| Net realized gain on investments sold consists of: | ||||

| 2012 | 2011 | |||

| $ | $ | |||

| Realized gain on securities sold | 953,729 | 2,064,001 | ||

| Realized (loss) gain on settlement of foreign currency contracts | (503,995 | ) | 2,203,559 | |

| 449,734 | 4,267,560 | |||

7 Taxation

Uncertainty of deductibility of tax losses

Prior to the reorganization and change in business as discussed in note 1, the Company had generated significant tax losses and other tax attributes as a result of its prior businesses and research activities. The Company has recorded, as a tax asset, the full amount of the potential tax benefit of such items to the extent of its projected taxable income. There is no guarantee that the tax authorities will allow the Company to deduct some, or all, of the tax losses and other attributes. Should the Company be denied the deductions, the recognized amount of the tax assets, as well as such amounts claimed to date, would be recorded as a charge to income. The total tax assets recognized and tax losses and other attributes claimed to date, which are subject to uncertainty, amount to $20,100,000 (December 31, 2011 - $21,024,806), representing $1.91 per common share at June 30, 2012 (December 31, 2011 - $2.00 per common share).

Future tax asset

Canadian GAAP requires a valuation allowance to be recognized against any future tax asset to the extent that it is more likely than not that the future income tax asset will not be realized. This is also the Company's stated accounting policy.

As the Company's investments in debt securities are generating interest income, but are not expected to generate sufficient taxable income in order to fully utilize the available tax credits during the years of operations through to April 30, 2014, the Company has recorded a valuation allowance. The difference between the total value of these tax benefits less the valuation allowance, being $4,050,000 (December 31, 2011 - $4,920,000), is the amount of the future income tax asset that has been recorded by the Company in the statement of net assets. The valuation allowance is reviewed periodically, based on updated projections of taxable income, and adjusted accordingly by a credit or charge to the statement of operations in that period.

The tax effects of temporary differences and tax credits that give rise to significant components of the future income tax assets at the statutory enacted rates when such benefits are expected to be realized are as follows:

| June 30, | December 31, | |||

| 2012 | 2011 | |||

| $ | $ | |||

| Future tax assets | ||||

| Non-capital loss carry forward | 54,600 | - | ||

| Research and development expenditures | 6,879,250 | 6,879,250 | ||

| Investment tax credits | 6,032,450 | 6,032,450 | ||

| Share issuance costs | 626,880 | 626,880 | ||

| Total gross future tax assets | 13,593,180 | 13,538,580 | ||

| Valuation allowance | (9,543,180 | ) | (8,618,580 | ) |

| Net future tax asset | 4,050,000 | 4,920,000 | ||

| Less: current portion | (2,310,000 | ) | (2,180,000 | ) |

| 1,740,000 | 2,740,000 |

The tax balances and income tax expense recognized by the Company are based on management's interpretation of the tax laws. Due to the complexity inherent in tax interpretations, regulations and legislation, there are significant estimates required to compute income tax balances. It is possible that some or all of the Company's significant components of the future income tax assets may not be deductible for tax purposes and, accordingly, the amount of future income taxes and provision for income taxes recorded in the financial statements could change by a material amount.

In determining the amount of future income tax assets recognized, management assessed the projected taxable income of the Company. Inherent in all forward looking information is uncertainty and actual amounts could differ from these estimates and the difference could be material. In developing the projection, management has assumed full payment of all contractual interest, that investments maturing prior to April 30, 2014 will be redeemed for par value, that reinvested funds will achieve an 8% yield, and that investments maturing after April 30, 2014 will be sold at their current value.

Tax pools available to offset future tax expense and payable

The operations of the Company and related tax interpretations, regulations and legislation are continually changing. As a result, significant estimates are required to compute income tax balances. As at June 30, 2012, the Company has accumulated scientific research and experimental development expenditures in the amount of $27,517,000 available for carry-forward indefinitely. The Company incurred non-capital losses in the six- months ended June 30, 2012, which will expire in 2032 and amount to $218,000. The Company also has accumulated approximately $7,097,000 of unclaimed federal investment tax credits, which expire as follows:

| Investment | |

| tax credits | |

| $ | |

| Year of expiry | |

| 2018 | 265,000 |

| 2019 | 990,000 |

| 2020 | 1,872,000 |

| 2021 | 2,483,000 |

| 2022 | 298,000 |

| 2023 | 187,000 |

| 2024 | 496,000 |

| 2025 | 506,000 |

| 7,097,000 | |

Reconciliation of income tax expense

The reconciliation of income tax computed at the statutory tax rate to income tax expense at June 30, using a 25.0 % statutory tax rate (2011 - 26.5%), is:

| 2012 | 2011 | |||

| $ | $ | |||

| (Decrease) increase in net assets from operations before taxes | (218,342 | ) | 4,451,232 | |

| Statutory tax rate | 25 | % | 26.5 | % |

| Income tax (recovery) expense at statutory rates | (54,600 | ) | 1,179,576 | |

| Non-capital loss carry forward | 54,600 | - | ||

| Use of scientific research and experimental development expenditures | - | (847,330 | ) | |

| Reduction of future tax asset | 870,000 | 680,000 | ||

| Current tax deductions for offering costs | - | (322,246 | ) | |

| Provision for future income tax | 870,000 | 680,000 | ||

8 Financial instruments

The following tables illustrate the classification of the Company's financial instruments within the fair value hierarchy:

| Financial assets at fair value - June 30, 2012 | ||||

| Level 1 | Level 2 | Level 3 | Total | |

| $ | $ | $ | $ | |

| Corporate debt | 91,518,339 | 26,589,216 | 118,107,555 | |

| Convertible debentures | 1,564,650 | 1,564,650 | ||

| Equity | 6,756,066 | 84,340 | 6,840,406 | |

| Foreign currency forward contracts | 887,767 | 887,767 | ||

| 6,756,066 | 92,406,106 | 28,238,206 | 127,400,378 | |

| Financial assets at fair value - December 31, 2011 | ||||

| Level 1 | Level 2 | Level 3 | Total | |

| $ | $ | $ | $ | |

| Corporate debt | - | 94,406,534 | 22,965,956 | 117,372,490 |

| Convertible debentures | - | - | 1,554,218 | 1,554,218 |

| Equity | 10,397,044 | - | 205,444 | 10,602,488 |

| Foreign currency forward contracts | - | 389,347 | 389,347 | |

| - | ||||

| 10,397,044 | 94,795,881 | 24,725,618 | 129,918,543 | |

All investments remained at their respective levels within the fair value hierarchy during the six-month period.

The following table reconciles the Company's Level 3 fair value measurements:

| Corporate | Convertible | |||||||

| debt | debentures | Equity | Total | |||||

| $ | $ | $ | $ | |||||

| Balance - December 31, 2010 | 14,475,875 | 3,617,677 | 400,000 | 18,493,552 | ||||

| Purchases | 14,812,500 | - | - | 14,812,500 | ||||

| Sales | (7,031,250 | ) | (2,148,120 | ) | - | (9,179,370 | ) | |

| Unrealized appreciation (depreciation) included in net gain (loss) on investments | 708,831 | 4,661 | (194,556 | ) | 598,936 | |||

| Balance - December 31, 2011 | 22,965,956 | 1,554,218 | 205,444 | 24,725,618 | ||||

| Purchases | 4,000,000 | - | - | 4,000,000 | ||||

| Sales | (650,000 | ) | - | - | (650,000 | ) | ||

| Unrealized appreciation (depreciation) included in net gain (loss) on investments | 273,260 | 10,432 | (121,104 | ) | 162,588 | |||

| Balance - June 30, 2012 | 26,589,216 | 1,564,650 | 84,340 | 28,238,206 | ||||

Level 3 fair value measurements have predominantly been valued by considering data inputs such as the last price the security was traded at, most recent bid/ask information, prices of similar securities with available prices, and comparison of yields of comparable investments. Accordingly it is not practicable to provide a sensitivity analysis.

Management of financial risks

In the normal course of business, the Company is exposed to various financial risks, including credit risk, liquidity risk and market risk (consisting of interest rate risk, currency risk and other price risk). The Company's overall risk management program seeks to minimize potentially adverse effects of these risks on the Company's financial performance by employing a professional, experienced portfolio adviser, monitoring daily the Company's positions and market events, diversifying the investment portfolio within the constraints of the investment guidelines and periodically using derivatives to hedge certain risk exposures. Further, the Company monitors the portfolio to ensure compliance with its investment strategy, investment guidelines and securities regulations.

Fair value risk

The Company's investments are exposed to market price risk and this risk affects the fair value of the investments. All investments have an inherent risk of loss of capital. The maximum risk resulting from investments is determined by their fair value. The Company seeks to manage valuation risks by careful selection of fixed income investments prior to making an investment and by regular ongoing monitoring of the investment performance of the individual investee companies. Due to the predominantly fixed income nature of the investment portfolio, the Company has minimal direct price risk. A 10% change in the value of the Company's equity investments would have a $676,000 impact on net assets, on an after tax basis.

Credit risk

Credit risk is the risk that a counter party to a financial instrument will fail to discharge an obligation or commitment that it has entered into with the Company.

All transactions executed by the Company in listed securities are settled /paid for upon delivery using approved brokers. The risk of this settlement not occurring is considered minimal, as delivery of securities sold is only made once the broker has received payment. Payment is made on a purchase once the securities have been received by the broker. The trade will fail if either party fails to meet its obligation. Since the Company invests in high-yield debt instruments and derivatives, this represents the main concentration of credit risk. The fair value of debt securities includes consideration of the creditworthiness of the debt issuer. The maximum credit exposure of these assets is represented by their carrying amounts. This maximum exposure may be offset to varying degrees in each investment, based on the collateral held, if any. Collateral may include such things as a general security agreement over all assets or specific security over specific assets. It may also entitle the debt holder to take over the overall business, through restructuring of the investment.

The Company's credit risk exposure by credit ratings on its investments is listed as follows:

| As a % of net assets | ||

| June 30, | December 31, | |

| 2012 | 2011 | |

| Credit rating | ||

| BB+ | 3.0 | - |

| BB | 1.9 | 1.7 |

| B | 32.1 | 37.3 |

| CCC | 29.1 | 23.0 |

| Not rated* | 21.3 | 21.8 |

| 87.4 | 83.8 | |

* Unrated debt securities consist primarily of convertible debentures and promissory notes in publicly traded companies.

Credit ratings are obtained from various credit rating agencies and sources. Where one or more rating is obtained for a security, the lowest rating has been used.

The Company's credit risk exposure by sector on its investments is as follows:

| As a % of net assets | ||

| June 30, | December 31, | |

| 2012 | 2011 | |

| Sector | ||

| Energy | 45.8 | 42.9 |

| Materials and metals | 16.1 | 12.2 |

| Consumer goods | 8.7 | 7.5 |

| Forestry | 7.0 | 6.9 |

| Industrial/manufacturing | 4.1 | 3.5 |

| Technology | 3.9 | 3.7 |

| Services | 1.8 | 4.2 |

| Financial Services | - | 2.9 |

| 87.4 | 83.8 | |

Interest rate risk

Interest rate risk arises from the possibility that changes in interest rates will affect future cash flows or fair values of financial instruments.

The Company invests primarily in interest-bearing financial instruments. As such, the Company is exposed to the risk that the value of such financial instruments will fluctuate due to changes in the prevailing levels of market interest rates. The table below summarizes the Company's exposure to interest rate risk by term to maturity:

| Fair value | ||

| June 30, | December 31, | |

| 2012 | 2011 | |

| $ | $ | |

| Maturity | ||

| Less than 1 year | 9,952,417 | 1,943,565 |

| 1 - 3 years | 16,657,489 | 20,139,165 |

| 3 - 5 years | 44,287,311 | 27,120,250 |

| Greater than 5 years | 49,662,755 | 70,113,075 |

| 120,559,972 | 119,316,055 |

As at June 30, 2012, if the prevailing interest rates had been raised or lowered by 1%, assuming a parallel shift in the yield curve, with all other factors remaining constant, net assets could possibly have decreased or increased, respectively, by approximately $4,000,000, or approximately 3.0% of net assets (December 31, 2011 - $5,000,000, or approximately 3.5% of net assets).

Liquidity risk

As the Company is a publicly traded, closed-end investment company with a fixed number of common shares outstanding, unlike an open-ended mutual fund, it is not exposed to the liquidity risk associated with daily cash redemptions of securities.

Investments in fixed income investments may not be able to be liquidated quickly at an amount close to their fair value to respond to specific events such as deterioration in the creditworthiness of any particular issuer. Fixed income investments purchased by the Company may be subject to resale restrictions such as hold periods. The resulting values for fixed income investments may differ from values that would be realized had a ready market existed.

The Company actively reviews its investment portfolio, and the fixed income market, to assess liquidity risk on its holdings.

Currency risk

Currency risk is the risk that the value of a financial instrument will fluctuate due to changes in foreign exchange rates. The Company invests a portion of its assets in securities that are denominated in a currency other than the Canadian dollar, which represents the functional currency of the Company. Consequently, the Company is exposed to currency risk as the value of the portfolio securities denominated in currencies other than the Canadian dollar will vary due to changes in foreign currency exchange rates.

The Company enters into foreign currency contracts with financial institutions to hedge the value of foreign currency denominated investments. The fair value of these contracts is reflected in investments. Gains or losses arising from these contracts offset the gains or losses from translation of the underlying investments. The unrealized gains or losses are reflected in unrealized appreciation/depreciation on foreign currency contracts on the statement of operations. The potential impact to net assets of a 5% change in foreign currency rates against the Canadian dollar, assuming all other variables remain constant, would be $5,800 (December 31, 2011 - $160,000).

At June 30, 2012, the Company had outstanding foreign exchange contracts to sell US$60,000,000 against future commitments at exchange rates ranging between 1.02842 and 1.04085 for US dollar foreign exchange contracts. Those contracts had maturities ranging up to August 9, 2012 and are with AAA rated Canadian banks and counterparties.

9 Capital management

The capital of the Company is divided into voting and non-voting common shares, each having an unlimited authorized amount. The number of voting and non-voting shares outstanding and changes thereto, are outlined in note 3.

The Company manages its capital in accordance with the Company's investment objectives. The Company's investment objectives are to: (i) maximize the total return for common shareholders, consisting of dividend income and capital appreciation; and (ii) provide shareholders with monthly dividends targeted to payout a minimum of 75% of net earnings annually. Net earnings in reference to the Company's dividend payments to shareholders exclude any realized and unrealized capital gains and losses from debt securities in the portfolio and any income or loss not derived from debt securities in the portfolio. The Company commenced its dividend payments on June 30, 2009, making monthly payments of $0.0583 per voting and non-voting common share, or $614,322. During the six-month period ended June 30, 2012, the Company made dividend payments of $3,685,935 (June 30, 2011 - $3,685,935).

The Company is committed to continue paying a monthly dividend of $0.0583 per voting and non-voting common share for the three-months ending September 30, 2012, totalling $1,842,966 (note 11).

10 Comparison of net asset value per share and net assets per share

In accordance with Section 3.6(1) of National Instrument 81-106, the Company's net asset value per share, the net assets per share calculated in accordance with Canadian GAAP for financial reporting purposes, and an explanation of the differences between such amounts, are required disclosures in the notes to the financial statements. For investments that are traded in an active market, Canadian GAAP requires that bid prices be used in the fair value of instruments, rather than the use of the last traded price, as currently used for the purpose of determining net asset value. This change accounts for the difference between the net asset value and the net assets.

| June 30, | December 31, | |||

| 2012 | 2011 | |||

| $ | $ | |||

| Net asset value per share | 13.03 | 13.49 | ||

| Canadian GAAP adjustments | (0.05 | ) | (0.06 | ) |

| Net assets per share | 12.98 | 13.43 | ||

11 Subsequent events

On July 5, 2012, the Company announced a monthly dividend of $614,322, or $0.0583 per common share, payable on each of July 31, 2012, August 31, 2012 and September 28, 2012.

Contact Information:

Craig Langdon

Chief Executive Officer and Director

(604) 669-0212

Deans Knight Income Corporation

Mark Myles

Chief Financial Officer

(604) 669-0212

www.dkincomecorp.com