VANCOUVER, BRITISH COLUMBIA--(Marketwire - Oct. 19, 2012) - Fancamp Exploration Ltd. (TSX VENTURE:FNC) ("Fancamp"or the "Company") announces today that its board of directors (the "Board") reaffirms its recommendation that shareholders vote FOR the management board nominees, Paul Ankcorn, Debra Chapman, Gilles Dubuc, Fouad Kamaleddine, Jean Lafleur, Mel de Quadros, Michael Sayer and Peter H. Smith at the upcoming annual general meeting of shareholders to be held on October 26, 2012 (the "Meeting").

In a letter being delivered to Fancamp's shareholders, members of the Board respond to misleading statements by concerned shareholder Mr. Robert N. Granger and advises them to reject the slate of nominees proposed by Mr. Granger since his proposals are not in the best interests of the Company's shareholders.

Because of the limited time before the Meeting, the Board also recommends that shareholders vote the WHITE proxy as soon as possible and prior to the final deadline for voting on Wednesday October 24, 2012 at 1 p.m. EDT.

The Board directs shareholders with questions or for voting assistance to please contact Fancamp's proxy solicitation agent:

| Georgeson |

| North American Toll Free Number: 1-888-605-8406, or |

| Email: askus@georgeson.com |

Letter to Shareholders

The full text of the letter to shareholders follows:

October 19, 2012

Dear Fancamp Shareholder:

By now, you may be aware that on October 15, 2012, Mr. Robert N. Granger ("Granger" or the "Concerned Shareholder") issued a concerned shareholder information circular (the "Concerned Shareholder Circular") seeking support to remove the existing board of directors (the "Board") of Fancamp Exploration Ltd. ("Fancamp" or the "Company") and replace it with his own nominees. This question will be decided at the Company's annual general meeting of shareholders scheduled for October 26, 2012 in Toronto (the "Meeting"). Your answer will be crucial to the future of your Company and your investment.

The Concerned Shareholder's "hide-in-the-weeds" tactics are evident from his belatedly issued Concerned Shareholder Circular on October 15, 2012 - only 9 days before voting deadline.

If Granger's interests are truly aligned with the best interests of the shareholders, he would not insist on complete control of the board through a slate of 100% Granger nominees, only three of whom owns any shares of the Company. Granger is attempting to take over your Company without compensation to the current shareholders.

| YOUR BOARD OF DIRECTORS RECOMMENDS THAT YOU: | |

| Γû¬ | VOTE FOR FANCAMP'S NOMINEES TO THE BOARD OF DIRECTORS USING THE ENCLOSED WHITE PROXY AND FOLLOWING ANY OF THE METHODS FOR VOTING DESCRIBED IN THE FORM OF PROXY |

| Γû¬ | REJECT GRANGER'S NOMINEES. DO NOT USE THE YELLOW CONCERNED SHAREHOLDER PROXY |

Having reviewed the Concerned Shareholder Circular, your Board is convinced that Granger has a hidden objective. Just days before the Meeting, Granger issued his Concerned Shareholder Circular seeking control of your Company without making an offer to all shareholders or payment of a control premium. Granger is opportunistically seizing this moment to fill the board with his own nominees and turn an approximately 6.8% interest in Fancamp into effective control. Under the Granger "plan", the dissident controls the board and the shareholders obtain no premium.

The Board considered the Concerned Shareholder Circular and after careful deliberation determined that the Concerned Shareholder Circular is based upon false allegations and misleading and slanted information and are intended to persuade you to willingly support the Concerned Shareholder under the false premise of protecting shareholder value.

| A NUMBER OF STATEMENTS MADE IN THE CONCERNED SHAREHOLDER PROXY CIRCULAR ARE MATERIALLY INCORRECT AND AT BEST ARE TAKEN OUT OF CONTEXT. |

Granger knows the value your Board is creating for all shareholders by developing Fancamp's projects. Granger did not personally own any shares or support the market in any way during his term as Chairman and director of Fancamp. In fact, he only recently purchased 75,000 shares to be eligible for the role of concerned shareholder. The Board urges the shareholders to ask themselves what is Granger's true intent.

Unfounded Broad-Based Criticisms:

Granger alleges that the Board's history demonstrates a dismal share performance and serious mismanagement. However, as a director of the Company since July 5, 2010 and as the Chairman of the board from December 7, 2010 up to October 9, 2012, Granger has been involved in and approved all final decisions regarding corporate strategy, annual budgets and program resource allocation. More importantly, as Chairman, Granger had control over the Company's agenda and items of business discussed at board meetings.

Our Proven Track Record

The pursuit of grassroots exploration activities is the cornerstone of the Company's vision and has lead to the Company's impressive roster of assets. Fancamp's funds have been spent wisely and indeed the targets have been carefully chosen with minimal acquisition costs (staking) and occasional property options where warranted. The Board and management of Fancamp have a proven track record with your Company, delivering tangible results on which you can rely, as evidenced by:

- The completion on May 18, 2012 of the acquisition by Champion Iron Mines Ltd. ("Champion") of Fancamp's 17.5% joint venture interest in the Fermont Properties in the Fermont iron ore district in north-eastern Quebec, which was not already owned by Champion. This agreement with Champion completes the contributory phase of Fancamp's share of the Fermont Joint Venture, locking in the value of a significant share of this important valuable asset, originally staked as a grassroots project.

- The Company filed on June 1, 2012, a National Instrument 43-101 Technical Report on the in-pit mineral resource estimates prepared by P&E Mining Consultants Inc. of Brampton (Ontario) on the Magpie #2 Deposit at its 46.72% owned Magpie Iron-Titanium-Vanadium-Chrome Project which represents a major milestone for the Magpie project, and confirms what management has believed all along about the resource and potential of the Magpie deposits.

- The Company announced this past March 5, 2012 that it had entered into a letter of intent with Bold Ventures Inc. ("Bold"), whereby Bold can earn a 50% interest in the McFaulds Fancamp Property by making cash payments totaling $1,500,000 and incurring $8,000,000 in exploration expenditures, over a three-year period. An additional 10% interest may be earned upon Bold delivering a positive feasibility study and making an additional payment of $700,000.

- The recent announcement this past September 28, 2012 by Fancamp of the ongoing evaluation of a series of five historic gold showings located in western Gaspé, and a part of its Appalachian early stage exploration project.

- The report by the Company this past August 16, 2012 of significant drill hole assay results based on compilation synthesis of historic unpublished information from the recently acquired Namex property in the Clinton volcano sedimentary belt located in southern Quebec near the Maine border, which information brought new insight on the potential of that zone.

- The Company's current holdings of 9.0 M shares of Argex Titanium Inc. ("Argex") as a result of Argex earning a 100% interest in the Company's interests in the staked Lac La Blache and Hanna/Consolidated Morrison properties from option agreements entered into in 2008.

Conflicting Granger's Actions

We believe that Granger's actions are unwarranted and unnecessary:

- Granger's hand-picked nominees for the replacement board have prior relationship with Granger, but no financial interest in Fancamp except for two of the nominees;

- Fancamp's existing strategy is on track to deliver value for all shareholders and not just selected shareholders;

- Granger has not demonstrated any value added strategic input nor a coherent exploration and development strategy;

- Granger has made numerous biased and unfounded allegations against the current Board and management; and

- Granger's tactics are evident from his belatedly issued Concerned Shareholder Circular on October 15, 2012 - only 9 days before voting deadline.

The Concerned Shareholder's Nominees Do Not Represent the Best Interests of Fancamp Shareholders

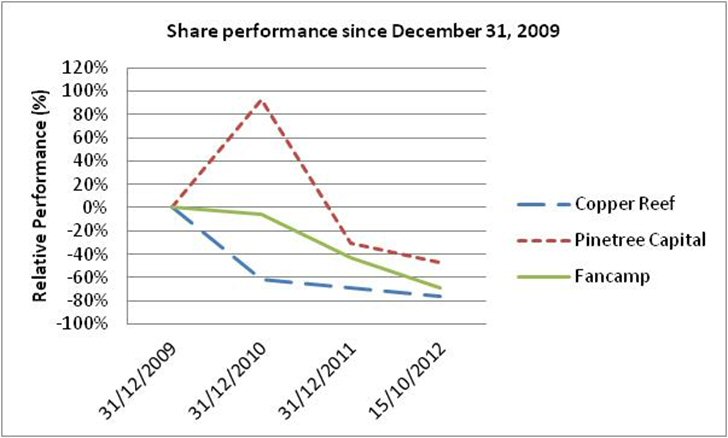

The proposed slate does not represent all shareholders' interests and is seen to be self-serving. We do not believe that the proposed slate will enhance shareholder value and, based on past record, may in fact unfavorably affect it. See for yourself the comparative performance graph reproduced below.

Share Value and Dilution

For junior mining companies active in modern-day capital markets, dilution is an undisputable and unavoidable reality as, without cash, a company may not pursue and achieve its goal. The financings completed by the Company served to add value to significant assets of the Company. The Board believes that any dilution was materially offset by the value added to those assets.

In addition, the decline in market capitalization reflects a trend prevalent throughout the market and has nothing to do with so called mismanagement and adherence to corporate practice. That said, the Concerned Shareholder Circular fails to state that the share price of Copper Reef Mining Corporation, an issuer for which Granger acts as Chairman according to public records, has tumbled approximately 76% since December 31, 2009 (compared to Fancamp's 69%).

Furthermore, the shares of Pinetree Capital Ltd., a TSX listed venture capital firm for which Mr. Sheldon Inwentash, one of Granger's slate nominees, acts as Chief Executive Officer and Chairman, have declined nearly 47% since December 31, 2009. Moreover, its share price has plunged an estimated 72% in the past two years, a sharp decrease that Granger failed to mention.

To view Share Performance graph, visit the following link: http://media3.marketwire.com/docs/SharePerformanceGraph.jpg

{kind=link}

There is little evidence that Granger's proposed slate of directors would add value to Fancamp. Only three of them including Granger have any prior interest or ownership in Fancamp, raising concerns about their lack of knowledge of the Company and its operations.

An Ambush

Shareholders are right to ask why the Concerned Shareholder waited so long to file his Concerned Shareholder Circular. Just days before the Meeting, the Concerned Shareholder is hoping to catch shareholders off-guard with this surprise attack. In providing little time for shareholders to vote their proxies for management in what was to be a routine meeting of shareholders, Granger no doubt hopes to disenfranchise shareholders.

The Board also wishes to underline that Granger did not personally own any shares or support the market in any way during his term as Chairman and director of Fancamp. In fact, he only recently purchased 75,000 shares after a Board meeting in which the rest of the Board expressed deep dissatisfaction with his actions and approved a new slate of nominees for consideration which excluded him.

Conflict of Interest: Granger's Initiative is Self-serving and Abusive

Fancamp is not and has never been a one man show. The Company has operated with input and cooperation of all the directors, management and technical team, all working towards building a strong company for all shareholders.

Champion - Fermont Properties

It was in this spirit of cooperation that Granger was given the consent of the Board and management to commence negotiations with Champion for the sale of the Company's 17.5% interest in the Fermont Properties to Champion (the "Champion Transaction"). Granger's inclination to act in his own best interests was brought to light when the terms he was negotiating were brought back to the Board for consideration and approval. Included in the proposed terms was the arrangement to appoint two board members from each party to serve on the other party's board of directors. Granger had assumed that he had negotiated a seat for himself on the board of Champion together with a generous compensation in the form of stock options on a personal level. His fellow Board members refused to act on this item and, in fact, insisted that due to obvious conflict of interest issues, two independent Board members would be nominated. It was at this point that Granger ceased to cooperate with his fellow Board members.

The Board takes great exception to the fact that Granger is attempting to take credit for a series of transactions that were negotiated with the cooperation and participation of the whole Board.

Moreover, it is noteworthy that Granger convinced the Board to authorize the engagement of a third party legal firm of his choice for, in his own words, "support purposes" in connection with the negotiation of the Champion Transaction - it being understood that Granger, a seasoned corporate and securities lawyer, would lead such negotiations in an uninterested fashion. The Board was later surprised to learn that Granger had retained an external legal firm, where Granger was once a partner. More importantly, the Board wishes to underline that the external legal firm invoice totaled $389,000 for the performance of support services over a two-month period.

The Board also notes that R.N. Granger Management Services, Granger's wholly-owned company, also invoiced $101,560 ($82,350 in fees) to Fancamp in connection with services rendered during the financial year ended April 30, 2012.

Granger has put his own interests before those of the Company in the negotiation of the Champion Transaction as he let the external legal firm take charge of the technical aspects of the Champion Transaction to shift his focus towards the obtaining of personal rewards for himself as evidenced by the significant invoice of the external legal firm.

Fancamp's Strategic Plan is On Track

As stated in its management information circular, Fancamp's Board and management understand the need for the Company to grow and evolve. The Board acknowledges the importance of that growth being sustainable, measured and disciplined. It is certainly risky and adventurous in these difficult markets to presume that wholesale change is the answer.

Well Seasoned Team with Experience

Fancamp's ability to achieve success in its competitive market requires focus, attention to detail and the support and guidance of an expert Board that understands the business and is up to speed on the intricacies involved in executing the Board's strategy. Fancamp's current Board is comprised of qualified and dedicated directors who understand both the industry and the Company.

All of Fancamp's director nominees are experienced and successful professionals with excellent reputations. They understand and have always upheld their fiduciary obligations to the Company.

The Company continues to search for additional talent to add value for the shareholders through involvement of senior and experienced persons on the Board and management and sees this managed approach as the effective way to grow the Company as we move forward.

Good things take time and hard work. Your Board represents the interests of ALL shareholders.

Corporate Governance

The Company has adopted sound corporate governance practices as disclosed in the management proxy circular dated September 26, 2012 (the "Management Circular").

Filing of Annual Financial Statements and related MD&A

Fancamp's audited financial statements and related MD&A for the year ended April 30, 2012 were approved by its audit committee and ultimately approved by the Board. The annual audited financial statements and related MD&A were filed on a timely basis.

Press Releases

As standard practice, the Company always issues news releases "on behalf of the board". The management of the Company acts on behalf of the Board. Press releases are circulated and input is requested. As some Board members are not always available, it is considered only important that the participating directors review and approve the content - i.e. QP on exploration projects. Fancamp is a company governed by a spirit of cooperation, with directors participating in its management, at all times putting the interests of shareholders first.

The Company and Ultimately the Shareholders Will be Paying for the Concerned Shareholder Proxy Contest

The Concerned Shareholder Circular states that Granger has retained the services of Kingsdale Shareholder Services Inc. in connection with Granger's solicitation of proxies and that he has agreed to a fee of up to approximately $225,000 plus disbursements. The Concerned Shareholder Circular further states that if Granger takes control of the Company, he will seek to be reimbursed by the Company for his out of pocket expenses, including the above-mentioned amount of $225,000 and legal fees incurred in connection with the solicitation of proxies for the Meeting.

The Board estimates that the costs to be borne by the Company in connection with Granger's proxy contest will range between $500,000 and $800,000 including the costs to be incurred by Fancamp's management to protect your Company.

Voting Instructions

The Company is confident that once shareholders understand the facts and motivations surrounding Granger's attempt to obtain control of Fancamp, shareholders will vote for Fancamp's nominee directors. The Board urges shareholders to NOT sign or return any forms of proxy that may be sent to you by the Concerned Shareholder group.

| WE URGE SHAREHOLDERS TO EXPRESS THEIR SUPPORT FOR THE BOARD BY VOTING THEIR WHITE PROXY PRIOR TO THE VOTING DEADLINE OF 1 P.M. ON WEDNESDAY OCTOBER 24, 2012. |

Your vote is important regardless of the number of common shares you own. Whether or not you are able to attend the Meeting, if you are a registered shareholder, we urge you to complete the White Management Proxy using any one of the methods described in the Management Circular by no later than Wednesday, October 24, 2012.

Voting by proxy will not prevent you from voting in person if you attend the Meeting to be held on October 26, 2012 at 1:00 p.m. but will ensure that your vote will be counted if you are unable to attend. If you hold your common shares through a broker or an intermediary, we urge you to complete the applicable White Management voting instruction form using any one of the methods described in it.

For view document on How to Cast Your Vote, visit the following link: http://media3.marketwire.com/docs/VotingInstructions.pdf

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Contact Information:

Peter H. Smith, PhD, P. Eng.

President

(514) 481-3172

www.fancampexplorationltd.ca