TORONTO, ONTARIO--(Marketwired - May 2, 2013) - Forsys Metals Corp (TSX:FSY)(FRANKFURT:F2T)(NAMIBIAN:FSY) ("Forsys" or the "Company") is pleased to announce the completion of an Engineering Cost Study ("ECS") on its planned Valencia process plant for the Company's consolidated Norasa uranium project in Namibia. The ECS, which was completed by the Perth office of leading engineering group, AMEC Australia Pty Ltd ("AMEC"), confirms the Company's focus on optimizing the Norasa project's economics. Completion of the ECS is a significant milestone on the path to completion of a NI 43-101 Feasibility Study, which is expected before the end of 2013.

Engineering Cost Study Highlights

- Differential NPV estimates increased by US$348m1 before tax.

- Opex is significantly reduced from the adjusted 2010 engineering cost study (in 2013 dollars).

- Capex for the process plant is cost-effective at US$249.7m.

- Leach residence time reduced significantly by 30%.

- Increase in plant throughput from 8.7 Mt/a to 11.2 Mt/a.

- An increase in average annual production from 3.3 Mlb to 4.2 Mlb U3O8.

- Plant availability increased from 88% to 91%.

- Plant block model greatly simplified.

Marcel Hilmer, Chief Executive Officer, commented, "We are very pleased to have delivered a positive engineering cost study which highlights many positives for the Norasa Uranium Project. It constitutes an important component for the completion of a feasibility study, which is planned for release by year's end. As a consequence of the positive study, we are now accelerating the drilling programs at Valencia East and Valencia North with a strategy to release an updated mineral resources statement in Q3 2013. In the near term, we will appoint an engineering firm to complete the feasibility study, which will incorporate the optimized processing plant."

The study reviewed the Snowden Group 2008 definitive feasibility study and 2010 engineering cost study that outlined some potentially attractive comminution flowsheet changes and optimizations. The ECS details the results of these investigations and studies and incorporates the recommended flowsheet changes and optimizations into the revised and updated capital and operating costs for the process plant component of the Norasa project.

The ECS will be available for download from www.forsysmetals.com.

Engineering Study - Key Metrics

AMEC completed a review of a number of alternative comminution circuits and compared them to an Adjusted Base Case ("ABC"). The ABC used the existing Snowden Group design; a 8.7 Mt/a, three-stage crushing and rod milling (3 off) at a grind of P80 = 850 µm. Capital and operating Costs were adjusted to reflect rate changes from 2010 to 2013 costs. Of the options considered, the most beneficial in overall terms was the semi autogenous grinding (SAG) Mill. The design is a two-stage crush plus single stage SAG mill using acidic filtrate at a grind of P80 ~600 µm.

| ABC | SAG Mill1 | |

| Feed tonnage, Mt/a | 8.7 | 11.2 |

| Mill grade, g/ t U3O8 | 194 | 194 |

| Overall U3O8 recovery | 85% | 85% |

| Annual production, Mlb U3O8 | 3.3 | 4.2 |

| Operating cost, US$ Tonne | $8.60 | $7.68 |

| Operating cost, US$ lb U3O8 | $23.66 | $21.11 |

| Capital cost, US$ M | $241.60 | $249.70 |

| Crushing | Three-stage | Two-stage |

| Milling | 3 rod mills | 1 SAG mill |

| U3O8 Price $/lb | $70 | $70 |

| Total Revenue US$M/LoM | $3,504 | $4,487 |

| Total Operating Costs US$M/LoM | $2,109 | $2,314 |

| Differential NPV $M (relative to ABC, 8% DR - before tax) |

$0 | $348 |

1 - The revenue, total operating costs and differential NPV values were generated by the Company using the capital costs and indicative operating costs estimated in the ECS, in addition to other assumptions made by Forsys on items excluded from this study, such as mining, external infrastructure, owner's costs, etc. which will be reviewed and estimated as part of the feasibility study. The differential NPV values in the above table are within 4% of the AMEC estimated differential NPV values considering the process plant and site infrastructure only. The differential NPV is a suitable measure to determine the possible economic improvements from implementing the SAG mill option as it relates to the processing plant. There is a ±25% accuracy associated with the cost study review.

To view the figure accompanying this press release, please visit the following link:

http://media3.marketwire.com/docs/870460.jpg

{kind=link}

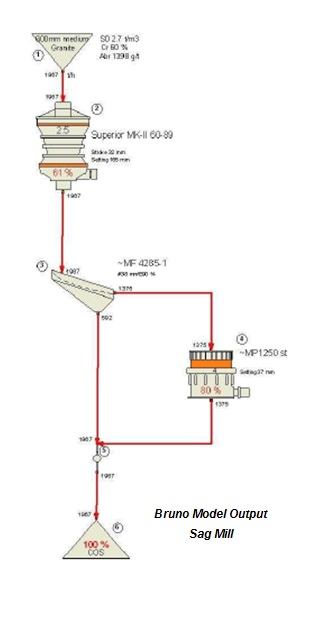

Bruno Modelling (A Metso process optimization tool)

Bruno modelling was conducted to model circulating loads around the main front end comminution equipment. The basis for the Bruno modelling is shown in the table below.

| ABC | SAG Mill | ||

| Secondary, Tertiary Crusher Circuit | |||

| Run time | % | 75 | 65 |

| Run rate | t/h | 1322 | 1967 |

| Fine Ore Stockpile (FOS) | h (downstream capacity) | 12 | |

| t live | 13 076 | ||

| Mill/Repulp | |||

| Type | Rod | SSSAG | |

| In acid? | No | Yes | |

| No. of | 3 | 1 | |

| Run time | % | 88 | 91 |

| Run rate | t/h | 1127 | 1400 |

| Water added to mill/repulp circuit | m3/h | 628 | 1372 |

| Leach Circuit | |||

| Solids rate | t/h | 1127 | 1400 |

| Solids density | % | 65 | 48 |

| Water | t/h | 607 | 1517 |

| Water | m3/h | 607 | 1517 |

| Water SG | 1 | 1 | |

| Solids SG | 2.7 | 2.7 | |

| Slurry total | m3/h | 1024 | 2036 |

| Pulp density | t/m3 | 1.69 | 1.43 |

Capex

The capital cost summary for the SAG mill is set out below:

| Description | Amount (US$) |

| Buildings | 4 172 646 |

| Process plant | 186 307 010 |

| Services and utilities | 6 127 350 |

| Reagents | 8 759 293 |

| Contractor mobilisation and demobilisation | 4 413 834 |

| Direct Construction Costs | 209 780 132 |

| First fills and spares | 9 369 024 |

| Temporary services and facilities | 3 219 262 |

| Total Costs before EPCM and Contingency | 222 368 418 |

| EPCM allowance | 27 362 854 |

| Total Costs before Contingency | 249 731 272 |

Optimization Opportunities, Risks and Next Steps

Opportunities for further project and process improvement that were identified in the AMEC ECS and warrant further investigation include:

- Potential to increase the overall uranium extraction and recovery to above the present assumed 85% by optimizing leach and filtration conditions further and also considering the finer grind size associated with the SAG mill.

- Leach optimization, especially with regards to using a higher leach temperature, could result in a significant reduction in the required leach residence time and associated circuit size.

- The present study assumed 91% availability for the SAG mill and downstream circuits, which could potentially be improved, especially considering the relative simplicity of this comminution circuit.

- Potential of a higher throughput than the 11.2 Mt/a assumed for the current study exists, and was cursorily explored and could provide additional economic benefits.

The main risk identified during the current study is the potential implications of the iron chemistry on reagent consumption, which needs better definition.

The Company is defining a scope of work for the purpose of conducting a tender process to select an engineering firm to complete the feasibility study. The non-exhaustive scope of work will include:

- A detailed design and costing of mine plans and associated Capex.

- Further testwork including confirming recent testwork that reported higher uranium recoveries.

- A review of administration overheads.

- Detailed flowsheets to integrate with the re-designed mill.

- Completion of appropriate economic models.

- Completion of appropriate documentation and drawings.

NORASA - Consolidated Namibian Projects

The Company announced in September 2012 a consolidation of its various uranium projects in the Erongo region of Namibia (Valencia and Namibplaas), and in January 2013 the Company announced the combined projects are now known as the Norasa Uranium Project. Norasa is an everyday term used by the rich and diverse culture of the Damara people and means united or putting things together.

Qualified Person

Mr. Dag Kullmann, M.Sc., General Manager and Project Engineer Norasa Operations, and a Fellow of the Southern African Institute of Mining and Metallurgy (SAIMM), is the designated QP responsible for the reporting of Mineral Reserves.

About Forsys Metals Corp.

Forsys Metals Corp. is an emerging uranium producer with 100% ownership of the fully permitted Valencia uranium project and the Namibplaas uranium project in Namibia, Africa a politically stable and mining friendly jurisdiction. Information regarding current National Instrument 43-101 compliant Resource and Reserves at Valencia and Namibplaas are available on our website.

On behalf of the Board of Directors of Forsys Metals Corp.

| Marcel Hilmer |

| Chief Executive Officer |

Sedar Profile #00008536

Forward-Looking Information

This news release contains projections and forward-looking information that involve various risks and uncertainties regarding future events. Such forward-looking information can include without limitation statements based on current expectations involving a number of risks and uncertainties and are not guarantees of future performance of the Company. The following are important factors that could cause Forsys actual results to differ materially from those expressed or implied by such forward looking statements: fluctuations in uranium prices and currency exchange rates; uncertainties relating to interpretation of drill results and the geology; continuity and grade of mineral deposits; uncertainty of estimates of capital and operating costs; recovery rates, production estimates and estimated economic return; general market conditions; the uncertainty of future profitability; and the uncertainty of access to additional capital. Full description of these risks can be found in Forsys Annual Information Form, dated March 15, 2013, available on the Company's profile on the SEDAR website at www.sedar.com. These risks and uncertainties could cause actual results and the Company's plans and objectives to differ materially from those expressed in the forward-looking information. Actual results and future events could differ materially from anticipated in such information. These and all subsequent written and oral forward looking information are based on estimates and opinions of management on the dates they are made and expressed qualified in their entirety by this notice. The Company assumes no obligation to update forward-looking information should circumstances or management's estimates or opinions change.

Shares Outstanding: 109,875,422

The Toronto Stock Exchange has not reviewed and does not accept responsibility for the adequacy or accuracy of this release.

Contact Information:

Marcel Hilmer

Chief Executive Officer

+61 417 177 942

mhilmer@forsysmetals.com

www.forsysmetals.com

TMX Equicom

Joe Racanelli

+1 416-815-0700 Ext 243

JRacanelli@equicomgroup.com