Earnings Analysis

--------------------------------------------------------------------------

2010 2009 2008

-------- --------- --------

Income before tax and preferred dividends,

as reported: $ (3,917) $ 3,536 $ 2,659

Credit related costs:

Loan loss provision 6,500 3,700 2,300

OREO write-downs/gains and losses 2,753 208 (80)

Noncore income:

Security gains 215 1,471 64

Gain on sale of branch offices - 1,208 -

-------- --------- --------

"Adjusted" income before taxes and preferred

dividends $ 5,121 $ 4,765 $ 4,815

======== ========= ========

(Excluding items, noted above)

As you will note from the chart above, the company's "core earnings" run

rate outside of extraordinary credit related charges and other one-time

items has improved as the result of lowered funding costs from the

significant growth in our core deposit base, control of non-interest

expenses, and increases in non-interest income from our SBA/USDA lending

programs and secondary market 1-4 family loan sales. It should be noted

that the subsidiary bank posted a small profit for the year of

approximately $83,000.

Paul Tobias, Chairman of MFNC, commenting on the overall results for 2010,

stated, "During 2010 we recognized the losses associated with a few large

credits, booked prior to the recession, that were well secured at the time

of loan origination but suffered from operating models that could not

withstand the severe recession and the deterioration of collateral values

in Southeastern Michigan. Despite the challenging times, we have made

significant progress to increase our franchise value. Our remaining

portfolio continues to perform satisfactorily and asset quality matrices

continue to outperform peers. We are confident that credit related expenses

will decrease in 2011 and return to normal levels in 2012."

Listed below are several key points relative to our 2010 results:

- We grew core bank deposits by $80 million. This reduced our reliance

on wholesale deposits by $115.4 million, reducing balance sheet risk. We

experienced core deposit growth in all of our markets, with $40 million in

Northern Lower Michigan, $11 million in Southeast Michigan and $29 million

in the Upper Peninsula. Most of our 2010 deposit growth occurred in low

cost transactional accounts which grew by $44 million.

- We continued to experience good loan demand with approximately $114

million of new loan production. At 2010 year-end, the Corporation's loans

stood at $383.086 million, a slight decrease from the 2009 year-end

balances of $384.310 million. Our total outstanding loans declined by $1.2

million after reductions for loan sales, (both SBA/USDA and secondary

market) amortization and payoffs, some associated with the elimination of

problem assets. We continue to be highly successful in producing well

priced high quality loans in the Upper Peninsula with 2010 loan production

of $81 million. Loan production totaled $22 million in Northern Lower

Michigan and $11 million in Southeast Michigan where the market have been

hit the hardest by the recession.

- In 2010 we had continued success in the origination and sales of

SBA/USDA loans with total fee income of $.9 million in 2010 compared to $.5

million in fee income during 2009. We continue to be a state leader in

these programs.

- One of our initiatives for 2010 was the expansion of our consumer

lending program by hiring several key mortgage loan producers and the

centralization of our consumer lending processing. This was successful,

with secondary market fee income of $.5 million in 2010 compared to $.3

million in 2009 and an increase in total consumer loan production from $39

million in 2009 to $60 million in 2010. We also have retained the servicing

of approximately $27 million of mortgage loans which provides future

refinancing opportunities and is a source of core deposits.

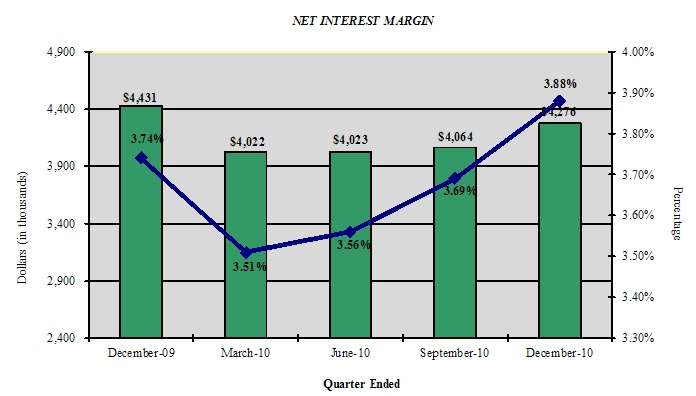

- We improved our net interest margin from 3.74% in the fourth quarter of

2009 to 3.88% in 2010's fourth quarter. Given our current funding

structure, we expect to see this improve throughout 2011 as

well.

- We had an overall reduction in nonperforming assets from $21.0 million

at the end of 2009 to $16.1 million at the end of 2010. As noted above, the

resolution of problem assets during 2010 impacted our earnings but we

divested these problem loans and OREO properties so that we could eliminate

holding costs and forego the opportunity cost that impacts longer-term

shareholder value creation.

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

SELECTED FINANCIAL HIGHLIGHTS

For The Years Ended

December 31,

(Dollars in thousands, except per share data) 2010 2009

----------- -----------

(Unaudited) (Unaudited)

Selected Financial Condition Data (at end of

period):

Assets $ 478,696 $ 515,377

Loans 383,086 384,310

Investment securities 33,860 46,513

Deposits 386,779 421,389

Borrowings 36,069 36,140

Shareholders' equity 53,882 55,299

Selected Statements of Income Data:

Net interest income $ 16,385 $ 16,287

Income before taxes and preferred dividend (3,917) 3,536

Net income (1,160) 1,907

Income per common share - Basic (.34) .56

Income per common share - Diluted (.34) .56

Weighted average shares outstanding 3,419,736 3,419,736

Selected Financial Ratios and Other Data:

Performance Ratios:

Net interest margin 3.66% 3.59%

Efficiency ratio 72.57 72.24

Return on average assets (.23) .39

Return on average equity (2.06) 3.77

Average total assets $ 502,993 $ 493,652

Average total shareholders' equity 56,171 50,531

Average loans to average deposits ratio 94.36% 92.99%

Common Share Data at end of period:

Market price per common share $ 4.58 $ 4.64

Book value per common share $ 12.63 $ 13.10

Common shares outstanding 3,419,736 3,419,736

Other Data at end of period:

Allowance for loan losses $ 6,613 $ 5,225

Non-performing assets $ 16,125 $ 21,041

Allowance for loan losses to total loans 1.73% 1.36%

Non-performing assets to total assets 3.37% 4.08%

Texas ratio 26.66% 34.77%

Number of:

Branch locations 11 10

FTE Employees 110 100

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

December 31, December 31,

(Dollars in thousands) 2010 2009

------------ ------------

(Unaudited) (Audited)

ASSETS

Cash and due from banks $ 22,719 $ 18,433

Federal funds sold 12,000 27,000

------------ ------------

Cash and cash equivalents 34,719 45,433

Interest-bearing deposits in other financial

institutions 713 678

Securities available for sale 33,860 46,513

Federal Home Loan Bank stock 3,423 3,794

Loans:

Commercial 308,677 305,670

Mortgage 68,473 74,350

Installment 5,936 4,290

------------ ------------

Total Loans 383,086 384,310

Allowance for loan losses (6,613) (5,225)

------------ ------------

Net loans 376,473 379,085

Premises and equipment 9,660 10,165

Other real estate held for sale 5,562 5,804

Other assets 14,286 23,905

------------ ------------

TOTAL ASSETS $ 478,696 $ 515,377

============ ============

LIABILITIES AND SHAREHOLDERS' EQUITY

Liabilities:

Non-interest-bearing deposits $ 41,264 $ 35,878

Interest-bearing deposits:

NOW, Money Market, Checking 134,703 95,790

Savings 17,670 18,207

CDs < $100,000 96,976 59,953

CDs > $100,000 22,698 36,385

Brokered 73,467 175,176

------------ ------------

Total deposits 386,778 421,389

Borrowings:

Federal funds purchased - -

Short-term 20,000 15,000

Long-term 16,069 21,140

------------ ------------

Total borrowings 36,069 36,140

Other liabilities 1,967 2,549

------------ ------------

Total liabilities 424,814 460,078

Shareholders' equity:

Preferred stock - No par value:

Authorized 500,000 shares, no shares

outstanding 10,706 10,514

Common stock and additional paid in capital

- No par value

Authorized - 18,000,000 shares

Issued and outstanding - 3,419,736 shares 43,525 43,493

Accumulated deficit (961) 199

Accumulated other comprehensive income

(loss) 612 1,093

------------ ------------

Total shareholders' equity 53,882 55,299

------------ ------------

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY $ 478,696 $ 515,377

============ ============

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in thousands, except per share

data) For The Years Ended December 31,

2010 2009 2008

---------- ----------- -----------

INTEREST INCOME: (Unaudited) (Audited) (Audited)

Interest and fees on loans:

Taxable $ 21,091 $ 20,521 $ 22,555

Tax-exempt 188 292 404

Interest on securities:

Taxable 1,406 2,783 1,293

Tax-exempt 28 19 5

Other interest income 127 93 305

---------- ----------- -----------

Total interest income 22,840 23,708 24,562

---------- ----------- -----------

INTEREST EXPENSE:

Deposits 5,607 6,431 10,115

Borrowings 848 990 1,583

---------- ----------- -----------

Total interest expense 6,455 7,421 11,698

---------- ----------- -----------

Net interest income 16,385 16,287 12,864

Provision for loan losses 6,500 3,700 2,300

---------- ----------- -----------

Net interest income after provision for

loan losses 9,885 12,587 10,564

---------- ----------- -----------

OTHER INCOME:

Service fees 990 1,023 838

Net security gains 215 1,471 64

Net gains on sale of secondary market

loans 1,407 830 120

Proceeds from settlement of lawsuits - - 3,475

Other 183 1,427 156

---------- ----------- -----------

Total other income 2,795 4,751 4,653

---------- ----------- -----------

OTHER EXPENSES:

Salaries and employee benefits 6,918 6,583 6,886

Occupancy 1,313 1,385 1,374

Furniture and equipment 806 805 771

Data processing 740 862 844

Professional service fees 627 603 508

Loan and deposit 4,620 1,793 489

Telephone 193 187 170

Advertising 297 322 305

Other 1,084 1,262 1,211

---------- ----------- -----------

Total other expenses 16,598 13,802 12,558

---------- ----------- -----------

Income before provision for income

taxes (3,918) 3,536 2,659

Provision for (benefit of) income taxes (3,500) 1,120 787

---------- ----------- -----------

---------- ----------- -----------

NET INCOME $ (418) $ 2,416 $ 1,872

---------- ----------- -----------

Preferred dividend expense 742 509 -

---------- ----------- -----------

NET INCOME AVAILABLE TO COMMON

SHAREHOLDERS $ (1,160) $ 1,907 $ 1,872

========== =========== ===========

INCOME PER COMMON SHARE

Basic $ (0.34) $ .56 $ .55

========== =========== ===========

Diluted $ (0.34) $ .56 $ .55

========== =========== ===========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

LOAN PORTFOLIO AND CREDIT QUALITY

(Dollars in thousands)

Loan Portfolio Balances (at end of period):

December 31, December 31,

2010 2009

------------- -------------

(Unaudited) (Audited)

Commercial Loans:

Real estate - operators of nonresidential

buildings $ 58,114 $ 48,689

Hospitality and tourism 37,737 45,315

Operators of nonresidential buildings 16,598 12,619

Real estate agents and managers 15,857 24,242

Other 135,411 150,214

------------- -------------

Total Commercial Loans 263,717 281,079

1-4 family residential real estate 75,074 67,232

Consumer 5,283 4,290

Construction

Commercial 33,330 24,591

Consumer 5,682 7,118

------------- -------------

Total Loans $ 383,086 $ 384,310

============= =============

Credit Quality (at end of period):

December 31, December 31,

2010 2009

------------ ------------

(Unaudited) (Audited)

Nonperforming Assets:

Nonaccrual loans $ 5,921 $ 14,368

Loans past due 90 days or more - -

Restructured loans 4,642 869

------------ ------------

Total nonperforming loans 10,563 15,237

Other real estate owned 5,562 5,804

------------ ------------

Total nonperforming assets $ 16,125 $ 21,041

============ ============

Nonperforming loans as a % of loans 2.76% 3.96%

------------ ------------

Nonperforming assets as a % of assets 3.37% 4.08%

------------ ------------

Reserve for Loan Losses:

At period end $ 6,613 $ 5,225

------------ ------------

As a % of average loans 1.72% 1.39%

------------ ------------

As a % of nonperforming loans 62.61% 34.29%

------------ ------------

As a % of nonaccrual loans 111.69% 36.37%

------------ ------------

Texas Ratio 26.66% 34.77%

------------ ------------

Charge-off Information (year to date):

Average loans $ 384,347 $ 374,796

------------ ------------

Net charge-offs $ 5,112 $ 2,752

------------ ------------

Charge-offs as a % of average loans 1.33% .73%

------------ ------------

MACKINAC FINANCIAL CORPORATION

FIVE YEAR OVERVIEW

QUARTER ENDED

--------------------------------------------------------

(Unaudited)

--------------------------------------------------------

December September June March December

31, 30, 30, 31, 31,

2010 2010 2010 2010 2009

--------- --------- --------- --------- ---------

BALANCE SHEET

(Dollars in

thousands)

Total loans $ 383,086 $ 382,727 $ 384,839 $ 377,311 $ 384,310

Allowance for

loan losses (6,613) (5,437) (6,371) (4,737) (5,225)

--------- --------- --------- --------- ---------

Total loans,

net 376,473 377,290 378,468 372,574 379,085

Intangible assets - - - - -

Total assets 478,696 499,006 500,774 502,427 515,377

Core deposits 290,614 287,055 271,026 236,227 209,828

Noncore deposits

(1) 96,165 117,469 134,758 168,985 211,561

--------- --------- --------- --------- ---------

Total deposits 386,779 404,524 405,784 405,212 421,389

Total borrowings 36,069 36,069 36,140 36,140 36,140

Total

shareholders'

equity 53,882 55,987 56,231 58,722 55,299

Total shares

outstanding 3,419,736 3,419,736 3,419,736 3,419,736 3,419,736

AVERAGE BALANCES

(Dollars in

thousands)

Assets $ 488,320 $ 512,335 $ 502,942 $ 508,495 $ 514,102

Loans 385,296 385,268 382,169 384,640 386,203

Deposits 393,266 416,847 405,449 413,897 418,280

Equity 55,015 56,668 57,889 55,109 55,665

INCOME STATEMENT

(Dollars in

thousands)

Net interest

income $ 4,276 $ 4,064 $ 4,023 $ 4,022 $ 4,431

Provision for

loan losses 1,800 1,000 2,800 900 2,300

--------- --------- --------- --------- ---------

Net interest

income after

provision 2,476 3,064 1,223 3,122 2,131

Total noninterest

income 747 648 593 807 1,503

Total noninterest

expense 4,037 3,601 5,330 3,629 3,650

--------- --------- --------- --------- ---------

Income before

taxes (814) 111 (3,514) 300 (16)

Provision for

income taxes 1,093 30 (1,212) (3,411) (22)

--------- --------- --------- --------- ---------

Net income (1,907) 81 (2,302) 3,711 6

--------- --------- --------- --------- ---------

Preferred

dividend expense 185 185 186 185 186

--------- --------- --------- --------- ---------

Net income

available to

common

shareholders $ (2,092) $ (104) $ (2,488) $ 3,526 $ (180)

========= ========= ========= ========= =========

PER SHARE DATA

Earnings $ (.61) $ (.03) $ (.73) $ 1.03 $ (.05)

Book value per

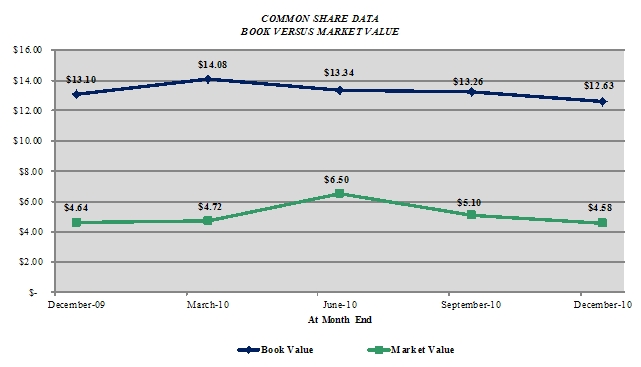

common share 12.63 13.26 13.34 14.08 13.10

Market value,

closing price 4.58 5.10 6.50 4.72 4.64

ASSET QUALITY

RATIOS

Nonperforming

loans/total

loans 2.76 % 2.94 % 2.87 % 2.62% 3.96%

Nonperforming

assets/total

assets 3.37 3.41 3.34 3.51 4.08

Allowance for

loan

losses/total

loans 1.73 1.42 1.66 1.26 1.36

Allowance for

loan

losses/nonperfo-

rming loans 62.61 48.34 57.69 47.87 34.29

Texas ratio (2) 26.66 27.68 26.71 27.76 34.77

PROFITABILITY

RATIOS

Return on average

assets (1.70)% (.08)% (1.98)% 2.81% (.14)%

Return on average

equity (15.09) (0.73) (17.24) 25.95 (1.28)

Net interest

margin 3.88 3.69 3.56 3.51 3.74

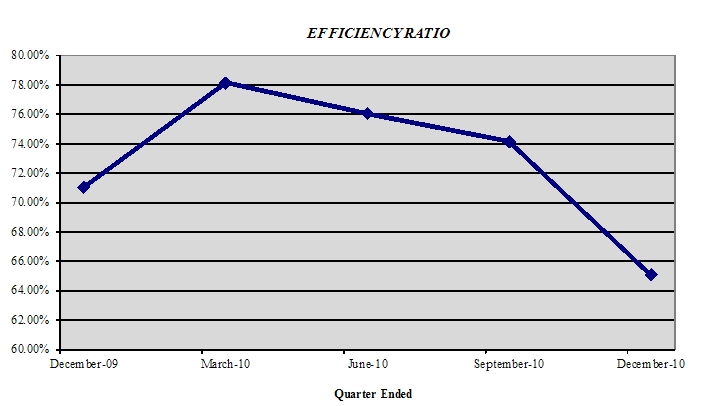

Efficiency ratio 65.05 75.98 76.04 78.12 71.03

Average

loans/average

deposits 97.97 92.42 94.26 92.93 92.33

CAPITAL ADEQUACY

RATIOS

Tier 1 leverage

ratio 9.25 % 9.22 % 9.38 % 9.85% 9.75%

Tier 1 capital to

risk weighted

assets 11.36 11.73 11.65 12.48 11.92

Total capital to

risk weighted

assets 12.62 12.98 12.91 13.69 13.17

Average

equity/average

assets 11.27 11.06 11.51 10.84 10.83

Tangible

equity/tangible

assets 11.27 11.06 11.51 10.84 10.83

(1) Noncore deposits includes Internet CDs, brokered deposits and CDs

greater than $100,000

(2) Texas ratio equals nonperforming assets divided by shareholders' equity

plus allowance for loan losses

Contact Information: Contact: Investor Relations (888) 343-8147 Website: www.bankmbank.com