MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

SELECTED FINANCIAL HIGHLIGHTS

For The Years Ended

December 31,

(Dollars in thousands,except per share data) 2006 2005

----------- -----------

(Unaudited) (Audited)

Selected Financial Condition Data (at end of

period):

Total assets $ 382,791 $ 298,722

Total loans 322,581 239,771

Total deposits 312,421 232,632

Borrowings and subordinated debentures 38,307 36,417

Total shareholders' equity 28,790 26,588

Selected Statements of Income Data:

Net interest income $ 11,593 $ 9,780

Income (loss) before taxes 1,216 (7,364)

Net income (loss) 1,716 (7,364)

Income (loss) per common share - Basic .50 (2.15)

Income (loss) per common share - Diluted .50 (2.15)

Selected Financial Ratios and Other Data:

Performance Ratios:

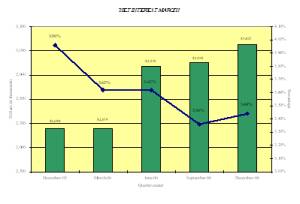

Net interest margin 3.51% 3.64%

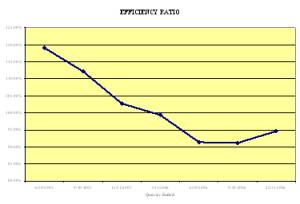

Efficiency ratio 93.95 160.43

Return on average assets .49 (2.58)

Return on average equity 6.19 (25.63)

Average total assets $ 347,927 $ 285,896

Average total shareholders' equity 27,744 28,732

Average loans to average deposits ratio 99.77% 98.17%

Common Share Data at end of period:

Market price per common share $ 11.50 $ 9.10

Book value per common share $ 8.40 $ 7.75

Common shares outstanding 3,428,695 3,428,695

Weighted average shares outstanding 3,428,695 3,428,695

Other Data at end of period:

Allowance for loan losses $ 5,006 $ 6,108

Non-performing assets $ 2,965 $ 1,059

Allowance for loan losses to total loans 1.55% 2.55%

Non-performing assets to total assets .77% .35%

Number of:

Branch locations 13 12

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in thousands, except per share data) December 31,

2006 2005

----------- -----------

ASSETS (Unaudited) (Audited)

Cash and due from banks $ 4,865 $ 4,833

Federal funds sold 5,841 3,110

----------- -----------

Cash and cash equivalents 10,706 7,943

Interest-bearing deposits in other financial

institutions 856 1,025

Securities available for sale 32,769 34,210

Federal Home Loan Bank stock 3,794 4,855

Loans:

Commercial 261,726 192,826

Mortgage 58,014 44,660

Installment 2,841 2,285

----------- -----------

Total loans 322,581 239,771

Allowance for loan losses (5,006) (6,108)

----------- -----------

Net loans 317,575 233,663

Premises and equipment 12,453 11,987

Other real estate held for sale 26 945

Other assets 4,612 4,094

----------- -----------

TOTAL ASSETS $ 382,791 $ 298,722

=========== ===========

LIABILITIES AND SHAREHOLDERS' EQUITY

Liabilities:

Non-interest-bearing deposits $ 23,471 $ 19,684

Interest-bearing deposits

Money market 42,340 31,198

NOW, Savings, and IRA 53,079 55,923

CDs < $100,000 80,719 67,725

CDs > $100,000 23,645 12,335

Brokered 89,167 45,767

----------- -----------

Total deposits 312,421 232,632

Borrowings 38,307 36,417

Other liabilities 3,273 3,085

----------- -----------

Total liabilities 354,001 272,134

Shareholders' equity:

Preferred stock - No par value:

Authorized 500,000 shares, no shares

outstanding - -

Common stock and additional paid-in capital -

No par value

Authorized - 18,000,000 shares

Issued and outstanding - 3,428,695 shares 42,720 42,412

Retained earnings (13,743) (15,461)

Accumulated other comprehensive income (loss) (187) (363)

----------- -----------

Total shareholders' equity 28,790 26,588

----------- -----------

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY $ 382,791 $ 298,722

=========== ===========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in thousands, For The Years Ended December 31,

except per share data) 2006 2005 2004

-------- -------- --------

(Unaudited) (Audited) (Audited)

Interest income:

Interest and fees on loans:

Taxable $ 21,239 $ 13,862 $ 14,517

Tax-exempt 753 928 1,180

Interest on securities:

Taxable 1,186 1,455 2,401

Tax-exempt 87 167 171

Other interest income 787 564 584

-------- -------- --------

Total interest income 24,052 16,976 18,853

-------- -------- --------

Interest expnese:

Deposits 10,575 5,259 5,443

Borrowings 1,884 1,937 4,730

Subordinated debentures - - 442

Total interest expense 12,459 7,196 10,615

-------- -------- --------

Net interest income 11,593 9,780 8,238

-------- -------- --------

Provision for loan losses (861) - -

-------- -------- --------

Net interest income after provision for loan

losses 12,454 9,780 8,238

-------- -------- --------

Other income:

Service fees 547 586 982

Net gains on sale of loans 197 49 39

Loan and lease fees 79 21 17

Net security gains (losses) (1) 95 -

Gain on sale of branches - - 205

Gain on settlement of subordinated

debentures - - 6,617

Other 161 360 682

-------- -------- --------

Total other income 983 1,111 8,542

-------- -------- --------

Other expenses:

Salaries and employee benefits 6,132 6,090 8,032

Occupancy 1,264 1,053 994

Furniture and equipment 631 560 887

Data processing 691 1,720 1,220

Accounting, legal and consulting fees 1,425 886 1,836

Loan and deposit 392 852 1,718

Telephone 210 271 382

Advertising 346 814 115

Penalty on prepayment of FHLB borrowings - 4,320 -

Other 1,130 1,689 3,044

-------- -------- --------

Total other expenses 12,221 18,255 18,228

-------- -------- --------

Income (loss) before provision for income

taxes 1,216 (7,364) (1,448)

Provision for (benefit of) income taxes (500) - 147

-------- -------- --------

Net income (loss) $ 1,716 $ (7,364) $ (1,595)

-------- -------- --------

Income (loss) per common share:

Basic $ .50 $ (2.15) $ (3.23)

======== ======== ========

Diluted $ .50 $ (2.15) $ (3.23)

======== ======== ========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

LOAN PORTFOLIO AND CREDIT QUALITY

(Dollars in thousands)

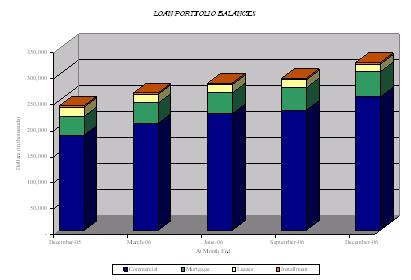

Loan Portfolio Balances (at end of period):

December 31,

2006 2005

---------- ----------

Commercial Loans

Real estate - operators of nonresidential buildings $ 44,308 $ 28,217

Hospitality and tourism 30,826 37,681

Real estate agents and managers 25,071 10,588

New car dealers 10,086 9,995

Other 115,426 88,842

---------- ----------

Total Commercial Loans 225,717 175,323

1-4 family residential real estate 58,014 44,660

Consumer 2,841 2,285

Construction 36,009 17,503

---------- ----------

Total Loans $ 322,581 $ 239,771

========== ==========

Credit Quality (at end of period):

December 31,

2006 2005

---------- ----------

Nonperforming Assets

Nonaccrual loans $ 2,899 $ 15

Loans past due 90 days or more 40 99

Restructured loans - -

---------- ----------

Total nonperforming loans 2,939 114

Other real estate owned 26 945

---------- ----------

Total nonperforming assets $ 2,965 $ 1,059

========== ==========

Nonperforming loans as a % of loans .91% .05%

---------- ----------

Nonperforming assets as a % of assets .77% .35%

---------- ----------

Reserve for Loan Losses:

At period end $ 5,006 $ 6,108

---------- ----------

As a % of loans 1.55% 2.55%

---------- ----------

As a % of nonperforming loans 170.33% 5,357.89%

---------- ----------

As a % of nonaccrual loans 172.68% N/M%

========== ==========

Charge-off Information:

Average loans $ 278,953 $ 207,928

---------- ----------

Net charge-offs $ 241 $ 858

---------- ----------

Charge-offs as a % of average loans .09% .41%

---------- ----------

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

QUARTERLY FINANCIAL HIGHLIGHTS

QUARTER ENDED

------------------------------------------------

Dec 31, Sept 30, June 30, March 31, Dec 31,

2006 2006 2006 2006 2005

--------- --------- --------- --------- ---------

BALANCE SHEET (Dollars

in thousands)

Total loans $ 322,581 $ 292,614 $ 283,110 $ 264,471 $ 239,771

Allowance for loan

losses (5,006) (5,316) (5,415) (5,415) (6,108)

--------- --------- --------- --------- ---------

Total loans, net 317,575 287,298 277,695 259,056 233,663

Intangible assets 205 237 268 299 330

Total assets 382,791 363,191 352,497 334,591 298,722

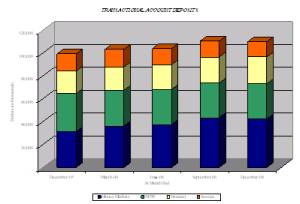

Core deposits 199,609 195,774 185,784 183,438 174,530

Noncore deposits (1) 112,812 97,720 98,380 84,516 58,102

--------- --------- --------- --------- ---------

Total deposits 312,421 293,494 284,164 267,954 232,632

Total borrowings 38,307 38,307 37,617 36,417 36,417

Total shareholders'

equity 28,790 28,226 27,179 27,173 26,588

Total shares

outstanding 3,428,695 3,428,695 3,428,695 3,428,695 3,428,695

INCOME STATEMENT (Dollars

in thousands)

Net interest income $ 3,027 $ 2,952 $ 2,935 $ 2,679 $ 2,680

Provision for loan

losses (261) - - (600) -

--------- --------- --------- --------- ---------

Net interest income

after provision 3,288 2,952 2,935 3,279 2,680

Total noninterest income 276 240 251 216 303

Total noninterest

expense 3,226 3,002 2,996 2,997 4,011

--------- --------- --------- --------- ---------

Income before taxes 338 190 190 498 (1,028)

Provision for income

taxes - (500) - - -

--------- --------- --------- --------- ---------

Net income $ 338 $ 690 $ 190 $ 498 $ (1,028)

========= ========= ========= ========= =========

PER SHARE DATA

Earnings per share -

basic $ .10 $ .20 $ .05 $ .15 $ (.30)

Earnings per share -

diluted .10 .20 .05 .15 (.30)

Book value per share 8.40 8.23 7.93 7.93 7.75

ASSET QUALITY RATIOS

Nonperforming loans/total

loans .91% .71% .16% N/M% .05%

Nonperforming

assets/total assets .77 .58 .14 .28 .35

Allowance for loan

losses/total loans 1.55 1.82 1.91 2.05 2.55

Allowance for loan

losses/nonperforming

loans 170.33 257.43 1,214.13 N/M 5,357.89

PROFITABILITY RATIOS

Return on average assets .37% .75% .22% .63% (1.41)%

Return on average equity 4.68 9.76 2.82 7.47 (14.95)

Net interest margin 3.44 3.36 3.62 3.62 3.96

Efficiency ratio 94.60 91.17 91.41 99.37 128.37

Average loans/average

deposits 102.29 97.51 99.67 98.44 102.01

CAPITAL ADEQUACY RATIOS

Leverage ratio 7.85 7.81 8.04 8.54 9.23

Tier 1 capital ratio 8.77 9.36 9.28 9.74 10.57

Total capital ratio 10.02 10.62 10.54 11.00 11.84

Average equity/average

assets 7.81 7.73 7.94 8.48 9.45

Tangible equity/tangible

assets 7.47 7.71 7.64 8.04 8.80

(1) Noncore deposits includes brokered deposits and CDs greater than

$100,000

Contact Information: Contact: Investor Relations (888) 343-8147 Website: www.bankmbank.com