MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

SELECTED FINANCIAL HIGHLIGHTS

(Dollars in thousands, except per share data)

For The Period Ended

-------------------------------------

March 31, December 31, March 31,

2007 2006 2006

----------- ----------- -----------

(Unaudited) (Unaudited)

Selected Financial Condition Data

(at end of period):

Total assets $ 375,644 $ 382,791 $ 334,591

Total loans 318,421 322,581 264,471

Total deposits 304,412 312,421 267,954

Borrowings and subordinated

debentures 38,307 38,307 36,417

Total shareholders' equity 29,932 28,790 27,173

Selected Statements of Income Data:

Net interest income $ 3,178 $ 11,593 $ 3,279

Income (loss) before taxes 1,035 1,216 498

Net income (loss) 1,035 1,716 498

Income (loss) per common share -

Basic .30 .50 .15

Income (loss) per common share -

Diluted .30 .50 .15

Selected Financial Ratios and Other

Data:

Performance Ratios:

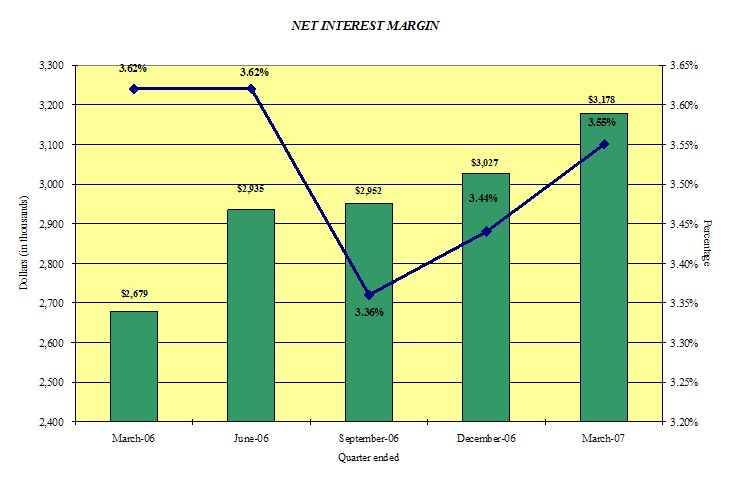

Net interest margin 3.55% 3.51% 3.62%

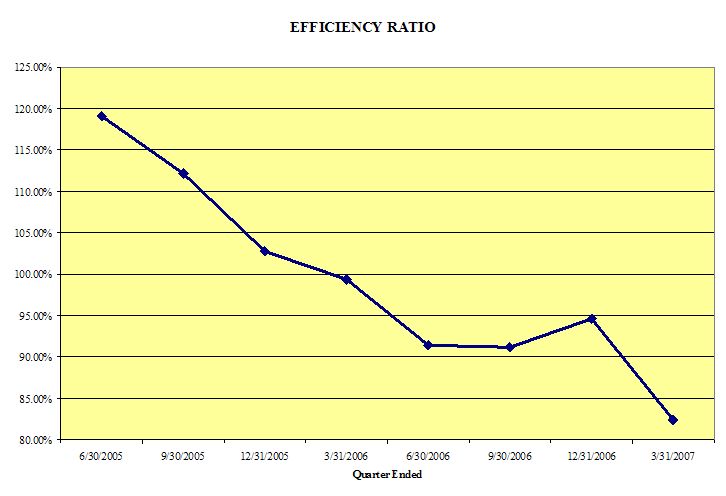

Efficiency ratio 82.40 93.95 82.88

Return on average assets 1.10 .49 .63

Return on average equity 14.35 6.19 7.47

Average total assets $ 380,403 $ 347,927 $ 319,007

Average total shareholders' equity 29,254 27,744 27,055

Average loans to average deposits

ratio 102.73% 99.77% 126.73%

Common Share Data (at end of

period):

Market price per common share $ 9.26 $ 11.50 $ 9.81

Book value per common share $ 8.73 $ 8.40 $ 7.93

Common shares outstanding 3,428,695 3,428,695 3,428,695

Weighted average shares outstanding 3,428,695 3,428,695 3,428,695

Other Data (at end of period):

Allowance for loan losses $ 4,975 $ 5,006 $ 5,415

Non-performing assets $ 4,989 $ 2,965 $ 952

Allowance for loan losses to total

loans 1.56% 1.55% 2.05%

Non-performing assets to total

assets 1.33% .77% .28%

Number of:

Branch locations 13 13 13

FTE Employees 104 99 105

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

March 31, December 31, March 31,

(Dollars in thousands) 2007 2006 2006

----------- ----------- -----------

(unaudited) (unaudited)

ASSETS

Cash and due from banks $ 5,647 $ 4,865 $ 6,220

Federal funds sold 6,330 5,841 12,000

----------- ----------- -----------

Cash and cash equivalents 11,977 10,706 18,220

Interest-bearing deposits in other

financial institutions 856 856 853

Securities available for sale 28,511 32,769 34,140

Federal Home Loan Bank stock 3,794 3,794 4,855

Loans:

Commercial 261,246 261,726 212,052

Mortgage 54,204 58,014 50,119

Installment 2,971 2,841 2,300

----------- ----------- -----------

Total Loans 318,421 322,581 264,471

Allowance for loan losses (4,975) (5,006) (5,415)

----------- ----------- -----------

Net loans 313,446 317,575 259,056

Premises and equipment 12,252 12,453 12,318

Other real estate held for sale 127 26 952

Other assets 4,681 4,612 4,197

----------- ----------- -----------

TOTAL ASSETS $ 375,644 $ 382,791 $ 334,591

=========== =========== ===========

LIABILITIES AND SHAREHOLDERS' EQUITY

Liabilities:

Non-interest-bearing deposits $ 23,416 $ 23,471 $ 20,463

Interest-bearing deposits

NOW and Money Market 70,558 73,188 67,467

Savings 13,488 13,365 15,304

CDs < $100,000 94,067 89,585 80,204

CDs > $100,000 24,475 23,645 15,246

Brokered 78,408 89,167 69,270

----------- ----------- -----------

Total deposits 304,412 312,421 267,954

Borrowings 38,307 38,307 36,417

Other liabilities 2,993 3,273 3,047

----------- ----------- -----------

Total liabilities 345,712 354,001 307,418

Shareholders' equity:

Preferred stock - No par value:

Authorized 500,000 shares, no

shares outstanding

Common stock and additional paid

in capital - No par value

Authorized - 18,000,000 shares

Issued and outstanding -

3,428,695 shares 42,750 42,722 42,489

Accumulated deficit (12,709) (13,745) (14,961)

Accumulated other comprehensive

(loss) (109) (187) (355)

----------- ----------- -----------

Total shareholders' equity 29,932 28,790 27,173

----------- ----------- -----------

TOTAL LIABILITIES AND SHAREHOLDERS'

EQUITY $ 375,644 $ 382,791 $ 334,591

=========== =========== ===========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in thousands except per share data) Three Months Ended

March 31,

-------------------------

2007 2006

------------ ------------

(Unaudited) (Unaudited)

INTEREST INCOME:

Interest and fees on loans:

Taxable $ 6,233 $ 4,499

Tax-exempt 171 194

Interest on securities:

Taxable 301 273

Tax-exempt - 41

Other interest income 200 168

------------ -----------

Total interest income 6,905 5,175

------------ -----------

INTEREST EXPENSE:

Deposits 3,222 2,080

Borrowings 505 416

------------ -----------

Total interest expense 3,727 2,496

------------ -----------

Net interest income 3,178 2,679

Provision for loan losses - (600)

------------ -----------

Net interest income after provision for loan

losses 3,178 3,279

------------ -----------

OTHER INCOME:

Service fees 161 111

Net security gains - -

Net gains on sale of secondary market loans 108 40

Other 644 65

------------ -----------

Total other income 913 216

------------ -----------

OTHER EXPENSES:

Salaries and employee benefits 1,738 1,594

Occupancy 334 317

Furniture and equipment 157 156

Data processing 171 154

Professional service fees 151 200

Loan and deposit 72 129

Telephone 58 49

Advertising 92 70

Other 283 328

------------ -----------

Total other expenses 3,056 2,997

------------ -----------

Income before provision for income taxes 1,035 498

Provision for (benefit of) income taxes - -

------------ -----------

NET INCOME $ 1,035 $ 498

============ ===========

INCOME PER COMMON SHARE:

Basic $ .30 $ .15

============ ===========

Diluted $ .30 $ .15

============ ===========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

LOAN PORTFOLIO AND CREDIT QUALITY

(Dollars in thousands)

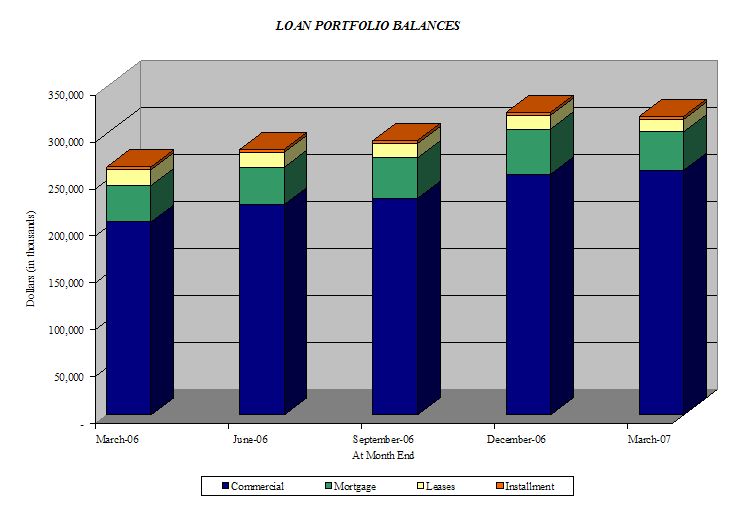

Loan Portfolio Balances (at end of period):

March 31, December 31, March 31,

2007 2006 2006

---------- ---------- ----------

Commercial Loans

Real estate - operators of nonresidential

buildings $ 44,155 $ 44,308 $ 32,440

Hospitality and tourism 33,726 30,826 38,045

Real estate agents and managers 27,313 25,071 12,350

New car dealers 10,139 10,086 9,988

Other 105,937 115,426 98,224

---------- ---------- ----------

Total Commercial Loans 221,270 225,717 191,047

1-4 family residential real estate 54,204 58,014 50,119

Consumer 2,971 2,841 2,300

Construction 39,976 36,009 21,005

---------- ---------- ----------

Total Loans $ 318,421 $ 322,581 $ 264,471

========== ========== ==========

Credit Quality (at end of period):

March 31, December 31, March 31,

2007 2006 2006

--------- --------- ---------

Nonperforming Assets :

Nonaccrual loans $ 4,142 $ 2,899 $ -

Loans past due 90 days or more 720 40 -

Restructured loans - - -

--------- --------- ---------

Total nonperforming loans 4,862 2,939 -

Other real estate owned 127 26 952

--------- --------- ---------

Total nonperforming assets $ 4,989 $ 2,965 $ 952

========= ========= =========

Nonperforming loans as a % of loans 1.53% .91% -%

--------- --------- ---------

Nonperforming assets as a % of assets 1.33% .77% .28%

--------- --------- ---------

Reserve for Loan Losses:

At period end $ 4,975 $ 5,006 $ 5,415

--------- --------- ---------

As a % of loans 1.56% 1.55% 2.05%

--------- --------- ---------

As a % of nonperforming loans 102.32% 170.33% N/A%

--------- --------- ---------

As a % of nonaccrual loans 120.11% 172.68% N/A%

========= ========= =========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

QUARTERLY FINANCIAL HIGHLIGHTS

QUARTER ENDED

-----------------------------------------------------

March 31, Dec 31, Sept 30, June 30, March 31,

2007 2006 2006 2006 2006

--------- --------- --------- --------- ---------

BALANCE SHEET

(Dollars in thousands)

Total loans $ 318,421 $ 322,581 $ 292,614 $ 283,110 $ 264,471

Allowance for loan

losses (4,975) (5,006) (5,316) (5,415) (5,415)

--------- --------- --------- --------- ---------

Total loans, net 313,446 317,575 287,298 277,695 259,056

Intangible assets 182 205 237 268 299

Total assets 375,644 382,791 363,191 352,497 334,591

Core deposits 201,529 199,609 195,774 185,784 183,438

Noncore deposits (1) 102,883 112,812 97,720 98,380 84,516

--------- --------- --------- --------- ---------

Total deposits 304,412 312,421 293,494 284,164 267,954

Total borrowings 38,307 38,307 38,307 37,617 36,417

Total shareholders'

equity 29,932 28,790 28,226 27,179 27,173

Total shares

outstanding 3,428,695 3,428,695 3,428,695 3,428,695 3,428,695

INCOME STATEMENT

(Dollars in thousands)

Net interest income $ 3,178 $ 3,027 $ 2,952 $ 2,935 $ 2,679

Provision for loan

losses - (261) - - (600)

--------- --------- --------- --------- ---------

Net interest

Income after

provision 3,178 3,288 2,952 2,935 3,279

Total noninterest

income 913 276 240 251 216

Total noninterest

expense 3,056 3,226 3,002 2,996 2,997

--------- --------- --------- --------- ---------

Income before taxes 1,035 338 190 190 498

Provision for income

taxes - - (500) - -

--------- --------- --------- --------- ---------

Net income $ 1,035 $ 338 $ 690 $ 190 $ 498

========= ========= ========= ========= =========

PER SHARE DATA

Earnings per share -

basic $ .30 $ .10 $ .20 $ .05 $ .15

Earnings per share -

diluted .30 .10 .20 .05 .15

Book value per share 8.73 8.40 8.23 7.93 7.93

ASSET QUALITY RATIOS

Nonperforming

loans/total loans 1.53% .91% .71% .16% N/M%

Nonperforming

assets/total assets 1.33 .77 .58 .14 .28

Allowance for loan

losses/total loans 1.56 1.55 1.82 1.91 2.05

Allowance for loan

losses/nonperforming

loans 102.32 170.33 257.43 1,214.13 N/M

PROFITABILITY RATIOS

Return on average

assets 1.10% .37% .75% .22% .63%

Return on average

equity 14.35 4.68 9.76 2.82 7.47

Net interest margin 3.55 3.44 3.36 3.62 3.62

Efficiency ratio 82.40 94.60 91.17 91.41 99.37

Average

loans/average

deposits 102.73 102.29 97.51 99.67 98.44

CAPITAL ADEQUACY

RATIOS

Leverage ratio 7.85% 7.85% 7.81% 8.04% 8.54%

Tier 1 capital ratio 9.16 8.77 9.36 9.28 9.74

Total capital ratio 10.41 10.02 10.62 10.54 11.00

Average equity/average

assets 7.69 7.81 7.73 7.94 8.48

Tangible equity/tangible

assets 7.74 7.47 7.71 7.64 8.04

(1) Noncore deposits includes Internet CDs, brokered deposits and CDs

greater than $100,000

Contact Information: Contact: Investor Relations (888) 343-8147 Website: www.bankmbank.com