MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

SELECTED FINANCIAL HIGHLIGHTS

(Dollars in thousands, except per share

data) For The Period Ended

---------------------------------

September December September

30, 31, 30,

2009 2008 2008

---------- --------- ----------

(Unaudited) (Unaudited)

Selected Financial Condition Data (at

end of period):

Assets $ 513,180 $ 451,431 $ 440,953

Loans 384,100 370,280 361,521

Investment securities 80,203 47,490 42,781

Deposits 418,581 371,097 360,694

Borrowings 36,140 36,210 36,210

Shareholders' Equity 55,766 41,552 41,427

Selected Statements of Income Data (nine

months and year ended):

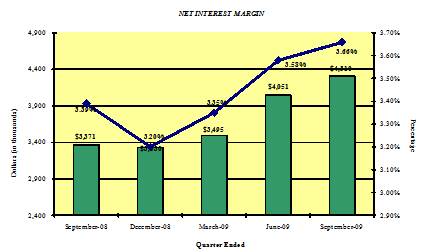

Net interest income $ 11,856 $ 12,864 $ 9,534

Income before taxes and preferred

dividend 3,552 2,659 3,082

Net income 2,087 1,872 2,124

Income per common share - Basic .61 .55 .62

Income per common share - Diluted .61 .55 .62

Three Months Ended:

Net interest income $ 4,310 $ 3,330 $ 3,371

Income before taxes and preferred

dividend 2,585 (423) 274

Net income 1,536 (252) 216

Income per common share - Basic .45 (.07) .06

Income per common share - Diluted .45 (.07) .06

Selected Financial Ratios and Other Data

(nine months and year ended):

Performance Ratios:

Net interest margin 3.54% 3.23% 3.24%

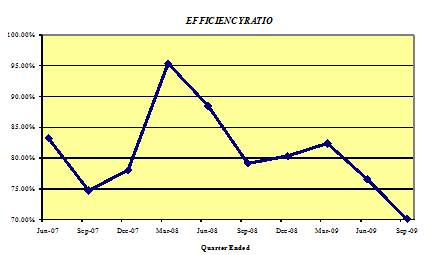

Efficiency ratio 77.71 85.51 87.36

Return on average assets .57 .44 .68

Return on average common equity 5.72 4.61 7.03

Average total assets $ 486,447 $ 425,343 $ 419,891

Average total common shareholders'

equity $ 44,312 $ 40,630 $ 40,332

Average loans to average deposits ratio 91.72% 105.61% 106.83%

Common Share Data (at end of period):

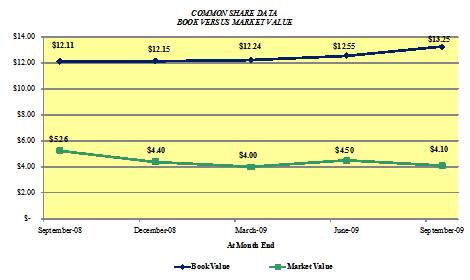

Market price per common share $ 4.10 $ 4.40 $ 5.26

Book value per common share $ 13.25 $ 12.15 $ 12.11

Common shares outstanding 3,419,736 3,419,736 3,419,736

Weighted average shares outstanding 3,419,736 3,422,012 3,422,777

Other Data (at end of period):

Allowance for loan losses $ 4,081 $ 4,277 $ 3,585

Non-performing assets $ 17,439 $ 7,076 $ 6,400

Allowance for loan losses to total loans 1.06% 1.16% .94%

Non-performing assets to total assets 3.38% 1.57% 1.45%

Number of:

Branch locations 10 12 12

FTE Employees 97 100 96

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

September December September

30, 31, 30,

(Dollars in thousands) 2009 2008 2008

---------- --------- ----------

(unaudited) (unaudited)

ASSETS

Cash and due from banks $ 23,249 $ 10,112 $ 8,217

Federal funds sold - - 4,422

---------- --------- ----------

Cash and cash equivalents 23,249 10,112 12,639

Interest-bearing deposits in other

financial institutions 662 582 382

Securities available for sale 80,203 47,490 42,781

Federal Home Loan Bank stock 3,794 3,794 3,794

Loans:

Commercial 306,590 296,088 290,406

Mortgage 73,116 70,447 67,576

Installment 4,394 3,745 3,539

---------- --------- ----------

Total Loans 384,100 370,280 361,521

Allowance for loan losses (4,081) (4,277) (3,385)

---------- --------- ----------

Net loans 380,019 366,003 358,136

Premises and equipment 10,281 11,189 11,360

Other real estate held for sale 5,821 2,189 1,751

Other assets 9,151 10,072 10,110

---------- --------- ----------

TOTAL ASSETS $ 513,180 $ 451,431 $ 440,953

========== ========= ==========

LIABILITIES AND SHAREHOLDERS' EQUITY

LIABILITIES:

Noninterest bearing deposits $ 33,254 $ 30,099 $ 34,858

NOW, money market, checking 88,843 70,584 80,185

Savings 18,807 20,730 18,957

CDs < $100,000 59,637 73,752 74,940

CDs > $100,000 25,409 25,044 30,220

Brokered 192,631 150,888 121,534

---------- --------- ----------

Total deposits 418,581 371,097 360,694

Borrowings:

Federal funds purchased - - -

Short-term - - -

Long-term 36,140 36,210 36,210

---------- --------- ----------

Total borrowings 36,140 36,210 36,210

Other liabilities 2,693 2,572 2,622

---------- --------- ----------

Total liabilities 457,414 409,879 399,526

SHAREHOLDERS' EQUITY:

Preferred stock - No par value:

Authorized 500,000 shares, no

shares outstanding 10,466 - -

Common stock and additional paid in

capital - No par value

Authorized - 18,000,000 shares

Issued and outstanding - 3,419,736

shares 43,485 42,815 42,794

Retained Earnings 378 (1,708) (1,456)

Accumulated other comprehensive

income 1,437 445 89

---------- --------- ----------

Total shareholders' equity 55,766 41,552 41,427

---------- --------- ----------

TOTAL LIABILITIES AND SHAREHOLDERS'

EQUITY $ 513,180 $ 451,431 $ 440,953

========== ========= ==========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in thousands except per share

data) Three Months Ended Nine Months Ended

September 30, September 30,

----------------- -----------------

2009 2008 2009 2008

-------- ------- -------- --------

(Unaudited) (Unaudited)

INTEREST INCOME:

Interest and fees on loans:

Taxable $ 5,106 $ 5,537 $ 15,212 $ 17,241

Tax-exempt 63 100 237 310

Interest on securities:

Taxable 888 303 2,020 840

Tax-exempt 7 1 11 4

Other interest income 28 87 44 257

-------- ------- -------- --------

Total interest income 6,092 6,028 17,524 18,652

-------- ------- -------- --------

INTEREST EXPENSE:

Deposits 1,550 2,308 4,894 7,924

Borrowings 232 349 774 1,194

-------- ------- -------- --------

Total interest expense 1,782 2,657 5,668 9,118

-------- ------- -------- --------

Net interest income 4,310 3,371 11,856 9,534

Provision for loan losses 700 450 1,400 1,200

-------- ------- -------- --------

Net interest income after provision for

loan losses 3,610 2,921 10,456 8,334

-------- ------- -------- --------

OTHER INCOME:

Service fees 236 229 750 597

Net security gains 644 (1) 644 64

Net gains on sale of secondary

market loans 247 16 179 113

Proceeds from lawsuit settlements - - - 3,475

Other 1,291 44 1,675 96

-------- ------- -------- --------

Total other income 2,418 288 3,248 4,345

-------- ------- -------- --------

OTHER EXPENSES:

Salaries and employee benefits 1,603 1,534 4,761 5,416

Occupancy 336 336 1,069 1,039

Furniture and equipment 193 202 604 570

Data processing 221 212 665 649

Professional service fees 161 120 458 352

Loan and deposit 402 176 1,175 430

Telephone 50 41 139 125

Advertising 80 93 238 213

Other 397 221 1,043 803

-------- ------- -------- --------

Total other expenses 3,443 2,935 10,152 9,597

-------- ------- -------- --------

Income before provision for income

taxes 2,585 274 3,552 3,082

Provision for (benefit of) income taxes 864 58 1,142 958

-------- ------- -------- --------

NET INCOME 1,721 216 2,410 2,124

-------- ------- -------- --------

Preferred dividend expense 185 - 323 -

-------- ------- -------- --------

NET INCOME AVAILABLE TO COMMON

SHAREHOLDERS $ 1,536 $ 216 $ 2,087 $ 2,124

======== ======= ======== ========

INCOME PER COMMON SHARE:

Basic $ .45 $ .06 $ .61 $ .62

======== ======= ======== ========

Diluted $ .45 $ .06 $ .61 $ .62

======== ======= ======== ========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

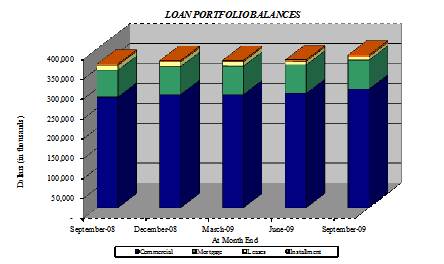

LOAN PORTFOLIO AND CREDIT QUALITY

(Dollars in thousands)

Loan Portfolio Balances (at end of period):

September December September

30, 31, 30,

2009 2008 2008

----------- ----------- -----------

Commercial Loans

Real estate - operators of

nonresidential buildings $ 47,007 $ 41,299 $ 41,486

Hospitality and tourism 45,867 35,086 35,287

Real estate agents and managers 23,996 29,292 29,277

Lessors of nonresidential buildings 13,782 13,467 13,352

Other 151,862 145,831 140,631

----------- ----------- -----------

Total Commercial Loans 282,514 264,975 260,033

1-4 family residential real estate 66,700 65,595 62,895

Consumer 4,394 3,745 3,539

Construction

Commercial 24,076 31,113 30,373

Consumer 6,416 4,852 4,681

----------- ----------- -----------

Total Loans $ 384,100 $ 370,280 $ 361,521

=========== =========== ===========

Credit Quality (at end of period):

September December September

30, 31, 30,

2009 2008 2008

---------- ---------- ----------

Nonperforming Assets:

Nonaccrual loans $ 10,655 $ 4,887 $ 4,649

Loans past due 90 days or more - - -

Restructured loans 873 - -

---------- ---------- ----------

Total nonperforming loans 11,528 4,887 4,649

Other real estate owned 5,821 2,189 1,751

---------- ---------- ----------

Total nonperforming assets $ 17,349 $ 7,076 $ 6,400

========== ========== ==========

Nonperforming loans as a % of loans 3.00% 1.32% 1.29%

---------- ---------- ----------

Nonperforming assets as a % of assets 3.38% 1.57% 1.45%

---------- ---------- ----------

Reserve for Loan Losses:

At period end $ 4,081 $ 4,277 $ 3,385

---------- ---------- ----------

As a % of average loans 1.10% 1.16% 0.94%

---------- ---------- ----------

As a % of nonperforming loans 35.40% 87.52% 72.81%

---------- ---------- ----------

As a % of nonaccrual loans 38.30% 87.52% 72.81%

========== ========== ==========

Charge-off Information (year to date):

Average loans 370,952 361,324 359,729

---------- ---------- ----------

Net charge-offs 1,596 2,169 1,961

---------- ---------- ----------

Charge-offs as a % of average loans .43% .60% .55%

---------- ---------- ----------

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

QUARTERLY FINANCIAL HIGHLIGHTS

QUARTER ENDED

-------------------------------------------------------

(Unaudited)

-------------------------------------------------------

September December September

30, June 30, March 31, 31, 30,

2009 2009 2009 2008 2008

--------- --------- --------- --------- ----------

BALANCE SHEET

(Dollars in

thousands)

Total loans $ 384,100 $ 372,004 $ 370,776 $ 370,280 $ 361,521

Allowance for loan

losses (4,081) (4,119) (4,793) (4,277) (3,385)

--------- --------- --------- --------- ----------

Total loans,

net 380,019 367,885 365,983 366,003 358,136

Intangible assets - 6 26 46 65

Total assets 513,180 506,304 466,375 451,431 440,953

Core deposits 200,541 202,892 196,860 195,165 208,940

Noncore deposits

(1) 218,040 210,260 188,897 175,932 151,754

--------- --------- --------- --------- ----------

Total deposits 418,581 413,152 385,757 371,097 360,694

Total borrowings 36,140 36,210 36,210 36,210 36,210

Total

shareholders'

equity 55,766 53,939 41,864 41,552 41,427

Total shares

outstanding 3,419,736 3,419,736 3,419,736 3,419,736 3,419,736

AVERAGE BALANCES

(Dollars in

thousands)

Assets $ 513,687 $ 491,205 $ 454,741 $ 441,583 $ 423,702

Loans 370,310 371,609 370,943 366,077 358,844

Deposits 419,102 401,510 372,670 358,213 341,377

Equity 54,594 49,855 41,813 41,516 41,097

INCOME STATEMENT

(Dollars in

thousands)

Net interest

income $ 4,310 $ 4,051 $ 3,495 $ 3,330 $ 3,371

Provision for loan

losses 700 150 550 1,100 450

--------- --------- --------- --------- ----------

Net interest

income after

provision 3,610 3,901 2,945 2,230 2,921

Total noninterest

income 2,418 439 391 308 288

Total noninterest

expense 3,443 3,470 3,239 2,961 2,935

--------- --------- --------- --------- ----------

Income before

taxes 2,585 870 97 (423) 274

Provision for

income taxes 864 271 7 (171) 58

Preferred dividend

expense 185 138 - - -

--------- --------- --------- --------- ----------

Net income $ 1,536 $ 461 $ 90 $ (252) $ 216

========= ========= ========= ========= ==========

PER SHARE DATA

Earnings - basic $ .45 $ .13 $ .03 $ (.07) $ .06

Earnings - diluted .45 .13 .03 (.07) .06

Book value per

common share 13.25 12.55 12.24 12.15 12.11

Market value,

closing price 4.10 4.50 4.00 4.40 5.26

ASSET QUALITY

RATIOS

Nonperforming

loans/total loans 3.00% 2.66% 3.52% 1.32% 1.29%

Nonperforming

assets/total

assets 3.38 2.93 3.27 1.57 1.45

Allowance for loan

losses/total

loans 1.06 1.11 1.29 1.16 .94

Allowance for loan

losses/nonperfor-

ming loans 35.40 41.71 36.72 87.52 72.81

PROFITABILITY

RATIOS

Return on average

assets .77% .38% .08% (.23)% .20%

Return on average

equity 7.17 3.71 .87 (2.42) 2.08

Net interest

margin 3.66 3.58 3.35 3.20 3.39

Efficiency ratio 70.09 76.55 82.36 80.30 79.12

Average

loans/average

deposits 88.36 92.55 99.54 102.20 105.12

CAPITAL ADEQUACY

RATIOS

Tier 1 leverage

ratio 10.30% 9.65% 7.86% 8.01% 8.31%

Tier 1 capital to

risk weighted

assets 12.89 11.94 9.31 9.25 9.40

Total capital to

risk weighted

assets 13.90 13.00 10.56 10.38 10.31

Average

equity/average

assets 10.63 10.15 9.20 9.40 9.70

Tangible

equity/tangible

assets 10.87 10.65 8.97 9.20 9.38

(1) Noncore deposits includes Internet CDs, brokered deposits and CDs

greater than $100,000

Contact Information: Contact: Investor Relations (888) 343-8147 Website: www.bankmbank.com