CHICAGO, IL--(Marketwired - Jul 18, 2013) - As graduation season comes to a close, many recent graduates have or are securing their first job out of college, settling into a new apartment or home, and beginning a new chapter filled with independence and excitement. TransUnion reminds them to take a moment after the celebrations are over to evaluate their current financial situation, recognize what debts they now need to start paying back, and understand what factors can help or hurt their chances at upcoming credit applications.

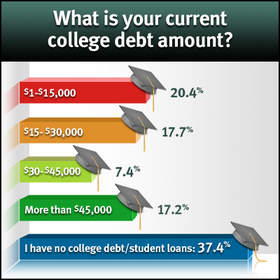

A new Google Consumer Survey commissioned by TransUnion of consumers that graduated from college in the last five years revealed that a quarter (25.1 percent) of recent graduates currently have $30,001 to $45,000 in college debt and an additional 17.2 percent of respondents said they have more than $45,000 in student debt.

"College debt can be one of the most challenging types of debt, simply because you are allowed to put off repayment -- and thinking about the money you owe -- until after graduation," said Julie Springer, vice president at TransUnion responsible for consumer education. "Graduates should take time to review their credit report on an ongoing basis to understand not only the amount of college debt they owe, but also to identify areas to work on and spot any inaccuracies that could possibly indicate identity theft."

TransUnion provides the following tips to help recent graduates get on the path to financial health and living with less college debt:

Know your repayment options: You have several options for repaying your loan. In general, if your loan balance is less than your annual starting salary, you can expect to pay off your college debt within about 10 years. If it's more, you may have to spread your payments out longer. There are several types of repayment plans outside of the traditional 10-year option, including extended, income-based and graduated. Explore all your options to see which one works best for your budget and debt amount, keeping in mind that the longer you stretch out repayment, the more interest you'll pay.

Make a plan: Once you've settled on a type of repayment plan that works best for your budget, get it down on paper. A repayment plan that factors in your living expenses, salary increases and other variables can help you feel more comfortable with your college debt -- you control your loans, not the other way around. Of course, your plan can always change from time to time, but being able to see your repayment path clearly can help you stay on track.

Pay extra: Think about all the unnecessary expenditures you have in your budget each month. While those expenses might be helping your social life, they do nothing for your student loans. Whenever you can, pay extra into your student loan. It may only be an extra $20 per month, but it can add up quickly and help you pay your education off and be debt-free sooner.

Don't Delay: It's never okay to skip a student loan payment. While most programs offer a deferment option -- where you can legally skip a payment -- it only prolongs your repayment process. Skipping payments without a deferment means defaulting and then dealing with dings on your credit report and a potentially lower credit score. Make your student debt a priority each month so you can take care of it quickly and without hurting your future ability to borrow.

Understand finances - Graduates need to understand exactly where their finances stand. Regularly reviewing financial statements along with their credit reports from all three credit reporting companies is a good way to understand where they stand at any given time.

Watch for danger signs - Negative records such as late payments and collection accounts can remain on credit reports for 7 years. Graduates can keep their future finances healthy by avoiding these problems from the beginning. Library, cell phone and video store late fees can sometimes be turned over to collection agencies who may then report them to the credit reporting companies. So graduates should keep an eye out for these as well.

Prepare for emergencies - A few preparations for the worst-case scenario can help recent graduates avoid financial problems in an emergency. To start, they should build up enough savings to cover their expenses for two to three months, with the goal of six months. If they find themselves out of a job or unable to pay back their debts, graduates should immediately call their creditors and lenders to explain the situation. Many federal loan programs have deferment and forbearance programs that allow borrowers to put their debts on hold temporarily.

For more information on how to deal with college debt, and all other debts, as well as receive your free credit score by signing up for a 7 day trial as part of your paid TransUnion membership, visit TransUnion.com.

About TransUnion

TransUnion Interactive, Inc. is a consumer subsidiary of TransUnion. As a global leader in credit and information management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering comprehensive data and advanced analytics and decisioning. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion employs associates in more than 33 countries on five continents. www.transunion.com. Follow us on Facebook at http://www.facebook.com/TransUnion.

Contact Information:

For More Information:

John Branham

512.351.3512