CALGARY, ALBERTA--(Marketwired - March 27, 2014) - New Millennium Iron Corp. ("NML" or the "Corporation") (TSX:NML) (OTCQX:NWLNF) announced today the results of the techno-economic viability of the Taconite Project Feasibility Study ("the Study"), which was jointly undertaken by Tata Steel Limited ("Tata Steel") and NML, and financed by the parties on a 64% - 36% basis, respectively. Under the Taconite Project Heads of Agreement (the "HOA") dated March 6, 2011, Tata Steel retains the option to participate in the development in due course, of one or both of the LabMag, and KéMag deposits. The Study consists of three separate scenarios, one for the development of KéMag deposit (100% owned by NML), one for LabMag deposit (80% owned by NML and 20% owned by the Naskapi Nation of Kawawachikamach) and the third which combines the development of the LabMag and KéMag deposits simultaneously. The Study covering all the three scenarios is collectively referred to as the Taconite Project ("TP"). Only the LabMag and KéMag deposits will be included in the NI 43-101 Technical Report. The choice of scenario to be developed will be made at the time of the investment decision. The Study Manager is a well-known international consulting firm and, in preparing the Study, was supported by a number of consultants specialized in their respective fields. The Capex and Opex details from the Study have been used by the Corporation to compile the financial summary as noted in Table 1 below. Infrastructure related items in the mine, ferroduct and port are proposed to be owned by third parties and leased to the Project. A reputed international accounting firm was engaged to review the financial model. In preparation for publication of the highlights of the Study, NML has engaged Met-Chem Canada Inc., Montreal, Quebec, to compile a National Instrument 43-101 compliant Technical Report for each of the LabMag and KéMag projects, which is required to be filed on SEDAR within 45 days of publication of this news release.

Project Highlights:

The following table summarizes the financial results for two standalone cases, LabMag and KéMag.

Table 1 (in CDN $millions unless otherwise noted)

| LabMag | KéMag | |||||

| Capex - Mine & Process 1 | 5,012 | 5,227 | ||||

| Capex - Infrastructure 2 | 2,737 | 3,012 | ||||

| Production cost per tonne of concentrate | $ | 43.03 | $ | 42.55 | ||

| Production cost per tonne of pellet 3 | $ | 52.22 | $ | 51.59 | ||

| Finance Lease for Infrastructure Cost per tonne of product 4 | $ | 12.50 | $ | 14.17 | ||

| Project IRR (before tax, 100% equity) | 18.2 | % | 17.5 | % | ||

| Project IRR (after tax, 100% equity) | 14.1 | % | 13.2 | % | ||

| IRR on equity (before tax, 30%-70% equity debt ratio) | 28.8 | % | 28.0 | % | ||

| IRR on equity (after tax, 30%-70% equity debt ratio) | 23.3 | % | 21.9 | % | ||

| Payback before tax at 100% equity (years after production start) | 4.9 | 4.9 | ||||

| Payback after tax at 100% equity (years after production start) | 5.6 | 5.7 | ||||

| Payback before tax at 30%-70% equity debt ratio (years after production start) | 3.3 | 3.3 | ||||

| Payback after tax at 30%-70% equity debt ratio (years after production start) | 3.5 | 3.5 | ||||

| NPV @ 8% before tax (100% equity) | 5,838 | 5,262 | ||||

| NPV @ 8% after tax (100% equity) | 2,849 | 2,241 | ||||

| NPV @ 8% before tax(30% equity) | 5,977 | 5,397 | ||||

| NPV @8% after tax (30% equity) | 3,303 | 2,697 | ||||

| Proven+Probable Reserves (million tonnes)5 | 3,410 | 1,891 | ||||

| Mine life (estimated years based on total low silica reserves)6 | 39 | 22 | ||||

(1) Costs of major mining equipment and power transmission line are not included in capex, but servicing costs are in the cash cost

(2) Consists of slurry transportation ferroduct and product storage and reclaiming system are to be financed on the basis of long term debt

(3) Average cash costs per tonne based on a total production of 23 million tonnes of pellets and pellet feed. Conversion cost of pellets is estimated at $11.12/t.

(4) Cost of servicing the annuity assumed at 7% interest for 25 years

(5) Does not include 523 and 493 million tonnes of proven and probable reserves in LabMag and KéMag respectively due to higher silica content at a cut-off of 4%

(6) Mine life increases to 42 years and 25 years for LabMag and KéMag respectively if additional reserves are included and if mined concurrently or in succession, to a combined life of 61 years

Project Assumptions:

- Production of 22 million metric tonnes per year ("Mtpy") of concentrate to produce 17.0 Mtpy of pellets and 6.0 Mtpy of pellet feed. (Actual total is estimated to be 23 Mtpy due to weight gain during the pelletizing process).

- Pellet production consists of 12 Mtpy of low silica (2.5% SiO2) blast furnace ("BF") grade fluxed pellets and 5 Mtpy of direct reduction ("DR") grade pellets with 1.8% SiO2.

- 6 Mtpy of pellet feed containing > 69.0% Fe and 2.2% SiO2.

- Product prices are based on a long term price forecast of US$103 for 62% Fe fines CFR North Chinese ports. This forecast was developed by World Steel Dynamics, Englewood Cliffs, New Jersey, USA, marketing consultant for the Study.

- After adjustment for ocean freight and quality factors, the assumed product prices loaded into ship at the Port are as follows: Pellet Feed US$90.00 per tonne ("t"), BF grade Pellets US$116.61/t and DR grade Pellets US$126.86/t.

- Exchange rates used for the cost estimates and revenues in the financial evaluation are US$0.90 and EUR 0.71 per CAD$1.00.

- Project economics presented are based on a 25 year mine plan for LabMag and 22 years for KéMag.

- Accuracy of cost estimates is considered to be ±15%.

Implementation Plan

- The shared conclusion is that the Study demonstrates Project viability and the parties are now proceeding with addressing key parameters on a timely basis that are expected to lead to an investment decision by Tata Steel which include, working with governments on selection of an appropriate scenario; completion of environmental assessment work; reviewing refined process and models that would permit a ramp up of production, improve operating expenditures and reduced initial capital costs; and update robust financial modelling that would result in making the Project investor and lender ready.

Robert Patzelt, President and CEO of NML said, "We are very pleased with the results of this joint study with our strategic partner, Tata Steel which is amongst the largest steelmakers in the world. We believe the results present a compelling case for a profitable, successful, long-term iron ore operation. We have always believed that New Millennium has the best ore bodies in the Labrador Trough. The favourable geological and mining characteristics of the deposits are manifested in the study's operating cost estimates, which would place our Taconite Project among the low cost pellet producers. We also want to emphasize that the project would produce premium products whose supply and demand balance over the next decade is estimated to be the best for all iron ore products. It also demands emphasis that we have been very fortunate in having support and technical expertise of Tata Steel. We will continue to work with governments at all levels, First Nations, suppliers, contractors and other stakeholders to advance the project to the next stage of development."

Project Descriptions:

General: The Study demonstrates that each of the two project scenario has the potential to become a significant new source of high quality pellets to serve the global steel industry. Each project scenario is based on primary processing consisting of mining and concentrating at the mine site, a slurry transportation system ("Ferroduct") to the secondary processing consisting of a pellet plant and product storage and reclaiming for transport to the terminal. Products will be shipped through a multi-user deep water dock.

LabMag and KéMag both feature Taconite ore similar to the ore currently being mined in the Mesabi Iron Range (MIR) in Minnesota, USA. The MIR Taconites have been a mainstay for the US steel industry since the early 1950s. The processing is based on well-proven and established flowsheet designs employed by the current producers. The Project will be competitive, aiming for a favourable position on the global cost curve for pellet producers. Natural advantages include a low stripping ratio and magnetite ore, which reduces energy costs in the pelletizing process. The Project's cost structure will also benefit from the use of large-scale and proven state of the art equipment. The concentrate will be transported from the mine through the ferroduct to the pellet plant. This is the most economical and environmentally friendly mode of transportation to the port, and will enable implementation of the Project independent of other users. The pellet plant will utilize the largest size equipment currently in operation. Shipping will be through a deep water dock capable of handling today's large-size vessels.

Geology & Mining: The Project's mining operation will have a total mining rate of up to a nominal 86 Mtpy of crude ore at an average Davis Tube ("DT") Weight Recovery ("WR") of between 25 to 27%. Mining will include all facilities for pre-strip, waste rock and low grade ore stockpiling, ore delivery and mine rehabilitation. Mine plans have been considered for each of the three scenarios, viz. LabMag, KéMag and Combined scenario. The deposits are ideal for open pit mining with low strip ratio and conventional truck and shovel mining methods have been selected. Due to the high tonnages expected to be mined, the trucks and shovels will be the largest and proven equipment available on the market. For each scenario, an optimized pit was determined using the 3D Lerchs-Grossman algorithm and a separate set of cut-off grades were established in order to ensure the feed ore would consist of better liberating ores that would allow for producing lower-silica products.

The Mineral Reserves are the portion of the Measured and Indicated Mineral Resources (refer to Table 2 below) that have been identified as being economically extractable, which incorporate mining losses and the addition of waste dilution. The total reserve base for the LabMag and KéMag deposits are shown respectively in Table 3 and Table 4 below.

Table 2: LabMag & KéMag Resources (Met-Chem 2013 models)

| Block | Resource by category | Million Tonnes | DTWR % | Head | Davis Tube Concentrate | |

| (18% DTWR cut-off) | %Fe | %Fe | %SiO2 | |||

| LabMag | Measured | 3,689 | 26.18 | 29.81 | 69.93 | 2.10 |

| Indicated | 632 | 25.03 | 29.24 | 70.08 | 2.00 | |

| Measured + Indicated | 4,321 | 26.01 | 29.73 | 69.96 | 2.09 | |

| Inferred | 1,063 | 25.22 | 29.64 | 69.88 | 1.85 | |

| KéMag | Measured | 1,507 | 26.97 | 31.45 | 69.69 | 2.56 |

| Indicated | 876 | 27.32 | 31.95 | 69.83 | 2.51 | |

| Measured + Indicated | 2,383 | 27.10 | 31.63 | 69.74 | 2.54 | |

| Inferred | 1,007 | 26.97 | 31.56 | 69.31 | 2.65 | |

| Total | Measured | 5,196 | 26.41 | 30.29 | 69.86 | 2.23 |

| Indicated | 1,508 | 26.36 | 30.81 | 69.93 | 2.30 | |

| Measured + Indicated | 6,704 | 26.40 | 30.41 | 69.88 | 2.25 | |

| Inferred | 2,070 | 26.07 | 30.57 | 69.60 | 2.24 | |

Table-3: LabMag Mineral Reserves

| Category | Tonnage (Mt) |

DTWR (%) |

Crude Fe (%) |

Davis Tube Concentrate | |

| Fe (%) | SiO2(%) | ||||

| Proven | 2,885 | 27.1 | 29.9 | 69.9 | 2.1 |

| Probable | 525 | 26.2 | 29.3 | 70.0 | 2.0 |

| Proven & Probable | 3,410 | 27.0 | 29.8 | 69.9 | 2.1 |

Note: Does not include 523 Mt of proven and probable reserves having higher silica content at a cut off of 4%.

Table-4: KéMag Mineral Reserves

| Category | Tonnage (Mt) |

DTWR (%) |

Crude Fe (%) |

Davis Tube Concentrate | |

| Fe (%) | SiO2(%) | ||||

| Proven | 1,172 | 27.0 | 31.2 | 69.8 | 2.2 |

| Probable | 718 | 27.9 | 31.4 | 70.1 | 2.1 |

| Proven & Probable | 1,891 | 27.0 | 31.3 | 69.9 | 2.2 |

Note: Does not include 493 Mt of proven and probable reserves having higher silica content at a cut off of 4%.

Processing: The plant design will be the same whether the ore is mined from LabMag or KéMag because similar blending criteria will be used to achieve the same liberation index (DT concentrate silica) in the plant feed. The only differences would be related to terrain topography and infrastructure which will be specific to the chosen site. The processing facility is designed with the capacity to produce 22 Mtpy of magnetite concentrate. The process plant involves multiple crushing and grinding stages followed by a conventional magnetite recovery circuit with a flotation plant to further reduce the silica in the concentrate to produce a high grade pellet feed for the pellet plant and the remainder to be sold as a concentrate. Traditional taconite concentrators utilize a primary crusher followed by an autogenous or semi-autogenous grinding mill (SAG) to reduce the size of the crushed ore before feeding to the magnetic separation circuit. Based on the results of extensive testing conducted since 2007, the SAG mill will be replaced with a second stage of crushing followed by high pressure grinding rolls (HPGR), which have been utilized in a similar manner in several iron ore projects around the world. HPGR requires much lower energy and has lower operating costs than the SAG process. Fine grinding in a ball mill, as used in traditional concentrators, will be required to produce a concentrate for the floatation circuit.

Slurry transportation: The fine grained concentrate, which is ideal for slurry transport will be pumped from the mine site to the port through a 28" (711mm) diameter and 600+ km long ferroduct with a single intermediate pumping station. KéMag and LabMag Projects will have separate routings. It will have the necessary tools for leak detection, repair equipment and emergency back-up power. The ferroduct design slopes will be limited (<10%) to avoid plugs in valleys even if the ferroduct is shut down full of slurry. Although the line will be buried almost its entire length, where it is not possible to bury the ferroduct, an appropriate thickness of insulation and heat tracing will be provided to prevent freezing. Ferroducts are used in iron ore projects in Tasmania, Mexico, Brazil, India and China. One such system is operating in Baotou, Inner Mongolia, with ambient temperatures as low as -41 degrees C. Ferroducts are cost effective, ecofriendly and known to be extremely reliable.

Pelletizing: Concentrate slurry will be dewatered and filtered. Filtered concentrate will either be sold as pellet feed or pelletized in two 8.5 Mtpy capacity machines. These are the largest size pelletizing equipment currently in operation. It is estimated that 16 Mtpy of magnetic concentrate will be required to produce 17 Mtpy of pellets because of the weight gain due to flux additives and to the exothermic reaction during the conversion of the magnetite into hematite. Magnetite ore has lower pelletizing costs compared to hematite because of lower energy requirements. Beginning in 2006, extensive tests were undertaken to develop the design basis for the pelletizing circuit. The final equipment configuration was tested at a leading vendor's laboratory and the equipment has been designed to meet the throughput requirements and product quality specifications for seaborne pellets.

Product Stockpiling and Shipping: Concentrate and screened pellets will be stockpiled in a yard adjacent to the pellet plant at the port. Products will be reclaimed and sent via a 7.6 km long overland conveyor to the multi-user deep water dock. The port will be capable of loading ocean going vessels with a current maximum capacity of 350,000 DWT. The rated capacity of the dock is 50 Mtpy and $38.4 million has been invested by NML to reserve 15 Mtpy of this capacity (refer to NR 12-17 dated July 18, 2012).

Environmental Assessment: The Project is expected to trigger several regimes of environmental assessment ("EA"). Discussions with the applicable governments have been held and it is concluded that a single environmental impact statement ("EIS") covering all the components of the Project may be submitted. The Project Description is a document that activates the various EA regimes and is currently complete. Much of the baseline data on the Taconite Project has been collected and has since been analyzed and reports completed. Intensive field work to collect biophysical baseline data were conducted in fall 2011 and spring-fall 2012. The data is currently being analyzed, and most of the field reports have been reviewed and approved.

Financial Analysis, Revenues and Sensitivity Analysis: Iron ore prices are based on a long-term projection of daily spot market prices, as quoted by an index, CFR Northern Chinese port for 62% Fe sinter fine products. Based on the supply demand analysis over different steel cycles, World Steel Dynamics of New Jersey, a noted steel industry analyst, has projected a long-term base line price of US$103.00 for 62% Fe grade CFR China. With appropriate quality adjustments and allowing for the freight from the port to China, the revenue assumptions are based on prices of US$90.00 per tonne of 69.0% Fe grade pellet feed Applying a US$30 spread between fines and BF grade pellets over the cycle and adjusting for 66.4% Fe grade in the pellet, the price of the BF grade fluxed pellet is estimated to be US$116.61 per tonne. Based on a 7% over the cycle premium for DR grade pellets compared to BF grades and adjusting for a Fe content of 67.9%, the price for DR grade pellets would be US$126.86. Long term exchange rate of US$0.90 equivalent to CAD$1.00 has been assumed for the Study.

The project economics presented are based on the first 25 year mine plan for the LabMag and Combined Projects, and 22 years for the KéMag Project, and consider mining only the proven and probable reserves (NI 43-101 compliant) with the required liberation characteristics (DTC silica 2.1%).

The Project financials have been evaluated with capital expenses excluding certain infrastructure-related capital expenses in the mine, port and ferroduct, which are identified and proposed to be owned by third parties and serviced on the basis of long-term lease. The evaluation is based on two separate cases: one with 100% equity and the other one with 30% -70% equity ratios. The debt is assumed to be financed at an interest rate of 7%.

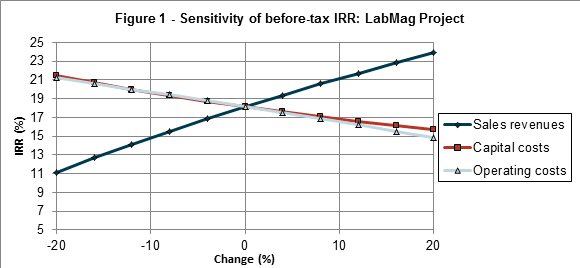

The sensitivity analysis with respect to sales revenue, capital costs and operating costs for the LabMag Project is illustrated in Figure 1. The figures are based on 100% equity.

To view the graph associated with this release, click the following link: http://media3.marketwire.com/docs/935744_c.jpg

{kind=link}

Technical Report by Met-Chem Canada Inc.:

An NI 43-101 Technical Report ("Report") is being prepared by Met-Chem Canada Inc. ("Met-Chem") will be posted on www.sedar.com within 45 days of this news release. Met-Chem is working on the Report in collaboration with the Study Manager and other supporting Consultants with their own Independent Qualified Persons. Met-Chem is a firm of experienced mining and metallurgical engineering professionals with expertise in exploration, mining evaluations, processing and the preparation of mineral resource/reserve estimates, especially in relation to iron ore. The Report will include updated mineral resource and reserve estimates which were prepared respectively by Mr. Schadrac Ibrango, P.Geo., PhD. and Mr. Jeffrey Cassoff, Eng. of Met-Chem. Both Mr. Ibrango and Mr. Cassoff are Independent Qualified Persons as defined by NI 43-101. The Report will consist of summary results from the Study. The Report is being prepared under the overall direction of Mr. Charles Cauchon Eng. of Met-Chem and will be reviewed and certified by individuals who are responsible for their respective portions of the Report. Mr. Cauchon and all other individuals providing certifications are Independent Qualified Persons as defined by NI 43-101. The financial analysis will be reviewed and certified by an Independent Qualified Person.

About New Millennium.

The Corporation controls the emerging Millennium Iron Range, located in the Province of Newfoundland and Labrador and in the Province of Quebec, which holds one of the world's largest undeveloped magnetic iron ore deposits. In the same area, the Corporation and Tata Steel Limited ("Tata Steel"), one of the largest steel producers in the world, have advanced a Direct Shipping Ore ("DSO") Project to the production stage, from which trial shipments have begun. Tata Steel owns approximately 26.3% of New Millennium and is the Corporation's largest shareholder and strategic partner.

Tata Steel exercised its exclusive option to participate in the DSO Project and has a commitment to take the resulting production (see news release 10-16 dated September 14, 2010). The DSO Project is owned and operated by Tata Steel Minerals Canada Limited ("TSMC"), which in turn is 80% owned by Tata Steel and 20% owned by NML. The DSO Project contains 98.8 million tonnes of Measured and Indicated Mineral Resources at an average grade of 59.3% Fe, 6.7 million tonnes of Inferred Resources at an average grade of 56.3% Fe and about 20.0 - 25.0 million tonnes of historical resources that are not currently in compliance with NI 43-101 (see news release 09-03 dated February 11, 2009, news release 09-05 dated March 4, 2009, news release 09-16 dated December 9, 2009, news release 10-12 dated July 8, 2010, news release 12-14, dated May 31, 2012 and news release 14-02 dated February 24, 2014). A qualified person has not done sufficient work to classify the historical estimate as current mineral resources or mineral reserves, the Corporation is not treating the historical estimate as current mineral resources or mineral reserves and the historical estimate should not be relied upon.

LabMag contains 3.9 billion tonnes of Proven and Probable reserves at a grade of 29.7% Fe plus 376 million tonnes of Measured and Indicated resources at an average grade of 29.6% Fe and 891.0 million tonnes of Inferred resources at an average grade of 29.3% Fe. KéMag contains 2.4 billion tonnes of Proven and Probable reserves at an average grade of 30.6% Fe and 1.0 billion tonnes of Inferred resources at an average grade of 31.7% Fe (See Tables 2, 3 & 4 in news release 14-04 dated March 27, 2014). Tata Steel also exercised its exclusive right to negotiate and settle a proposed transaction in respect of development of either or both the LabMag and the KéMag deposits (see news release 11-09 dated March 6, 2011).

The Millennium Iron Range now hosts other taconite deposits. The first is the Lac Ritchie property located at the north end of the Range. The initial 2011 drilling of 40 holes in this property revealed Indicated Resources of 3.330 billion tonnes at an average grade of 30.3% Fe, and Inferred Resources of 1.437 billion tonnes at an average grade of 30.9% Fe (see news release NR 12-11, dated April 02, 2012).

Two other taconite deposits are located south of the LabMag deposit in the Millennium Iron Range. The initial 2012 drilling of 23 holes in the Sheps Lake property and of 50 holes in the Perault Lake property revealed Indicated Resources of 3.580 billion tonnes at an average grade of 31.22%, and Inferred Resources of 795 million tonnes at an average grade of 30.56% (see news release NR 13-04, dated February 11, 2013).

The Howells Lake - Howells River North deposit is located between the LabMag and KéMag deposits, and evidences mineral continuity in the Range. The 2011 and 2012 drilling of 11 holes in the Howells River North property and of 45 holes in the Howells Lake property, revealed Indicated Resources of 7.631 billion tonnes at an average grade of 30.39% Fe, and Inferred Resources of 3.310 billion tonnes at an average grade of 29.83% Fe (see news release NR 13-15, dated May 23, 2013).

The Corporation's mission is to add shareholder value through the responsible and expeditious development of the Millennium Iron Range and other mineral projects to create a new large source of raw materials for the world's iron and steel industries.

For further information, please visit www.NMLiron.com, www.tatasteel.com, www.tatasteelcanada.com, and www.tatasteeleurope.com.

Dean Journeaux, Eng., Moulaye Melainine, Eng., and Thiagarajan Balakrishnan, P. Geo., are the Qualified Persons as defined in National Instrument 43-101 who have reviewed and verified the scientific and technical mining disclosure contained in this news release.

Forward-Looking Statements

This news release contains certain forward looking statements and forward looking information (collectively referred to herein as "forward looking statements") within the meaning of applicable Canadian securities laws. All statements other than statements of present or historical fact are forward looking statements. Forward looking information is often, but not always, identified by the use of words such as "could", "should", "can", "anticipate", "expect", "believe", "will", "may", "projected", "sustain", "continues", "strategy", "potential", "projects", "grow", "take advantage", "estimate", "well positioned" or similar words suggesting future outcomes. In particular, this news release may contain forward looking statements relating to future opportunities, business strategies, mineral exploration, development and production plans and competitive advantages.

The forward looking statements regarding the Corporation are based on certain key expectations and assumptions of the Corporation concerning anticipated financial performance, business prospects, strategies, regulatory developments, exchange rates, tax laws, the sufficiency of budgeted capital expenditures in carrying out planned activities, the availability and cost of labour and services and the ability to obtain financing on acceptable terms, the actual results of exploration and development projects being equivalent to or better than estimated results in technical reports or prior activities, and future costs and expenses being based on historical costs and expenses, adjusted for inflation, all of which are subject to change based on market conditions and potential timing delays. Although management of the Corporation consider these assumptions to be reasonable based on information currently available to them, they may prove to be incorrect.

By their very nature, forward looking statements involve inherent risks and uncertainties (both general and specific) and risks that forward looking statements will not be achieved. Undue reliance should not be placed on forward looking statements, as a number of important factors could cause the actual results to differ materially from the beliefs, plans, objectives, expectations and anticipations, estimates and intentions expressed in the forward looking statements, including among other things: inability of the Corporation to continue meet the listing requirements of stock exchanges and other regulatory requirements, general economic and market factors, including business competition, changes in government regulations or in tax laws; general political and social uncertainties; commodity prices; the actual results of exploration, development or operational activities; changes in project parameters as plans continue to be refined; accidents and other risks inherent in the mining industry; lack of insurance; delay or failure to receive board or regulatory approvals; changes in legislation, including environmental legislation, affecting the Corporation; timing and availability of external financing on acceptable terms; conclusions of, or estimates contained in, feasibility studies, pre-feasibility studies or other economic evaluations; and lack of qualified, skilled labour or loss of key individuals; as well as those factors detailed from time to time in the Corporation's interim and annual financial statements and management's discussion and analysis of those statements, along with the Corporation's annual information form, all of which are filed and available for review on SEDAR at www.sedar.com. Readers are cautioned that the foregoing list is not exhaustive.

The forward looking statements contained herein are expressly qualified in their entirety by this cautionary statement. The forward looking statements included in this news release are made as of the date of this news release and the Corporation does not undertake and is not obligated to publicly update such forward looking statements to reflect new information, subsequent events or otherwise unless so required by applicable securities laws.

With respect to the disclosure of historical resources in this news release that are not currently in compliance with National Instrument 43-101, a qualified person has not done sufficient work to classify the historical estimate as current mineral resources or mineral reserves, the Corporation is not treating the historical estimate as current mineral resources or mineral reserves and the historical estimate should not be relied upon.

Contact Information:

Robert Patzelt

President & Chief Executive Officer

(709) 770-2635 or (514) 935-3204 ext. 370

New Millennium Iron Corp.

Ernest Dempsey

Vice-President, Investor Relations and Corporate Affairs

(514) 935-3204 ext. 349

New Millennium Iron Corp.

Andreas Curkovic

Investor Relations

(416) 577-9927