VANCOUVER, BRITISH COLUMBIA--(Marketwired - June 8, 2015) - Northern Vertex Mining Corp. (the "Company") (TSX VENTURE:NEE) (OTCQX:NHVCF) is pleased to announce the results of a recently completed Feasibility Study on the Moss Gold-Silver Project located in Mohave County, Arizona. The Feasibility Study, which was completed on time and on budget, was prepared in accordance with standard industry practices and is summarized and disclosed in accordance with Canadian Securities Administrators NI 43 - 101 (Standards of Disclosure for Mineral Projects). The Feasibility Study will also serve as the "Bankable Feasibility Study" ("BFS") required by the Company's 2011 Exploration and Option to Enter Joint Venture Agreement, Moss Mine Project with Patriot Gold Corp. (the "Earn-in Agreement"). Under the Earn-in Agreement, Northern Vertex will earn 70% of the Project with the BFS being the final material requirement of the earn-in.

The Feasibility Study envisions an open-pit mining operation with crushing, agglomeration and stacking of ore onto a conventional heap leach pad. Gold and silver recovery will be achieved by a Merrill Crowe process to produce doré bar at the project site. The Project has been designed to have a 5 year mine life at a projected mining rate of 5,000 tonnes per day (tpd). All dollars are in US dollars.

The key highlights, at prices of US$1,250/oz Gold and US$20/oz Silver, 100% Project basis are:

| Annual Production (5,000 tpd) | 1,750,000 tonnes per year |

| Strip Ratio | 1.62 |

| Average Gold grade | 0.826 grams per tonne |

| Average Silver grade | 9.282 grams per tonne |

| Average Gold Equivalent ("AuEq") grade* | 0.93 grams per tonne |

| Recoveries to Doré | Gold 82% and Silver 65% |

| Life of Mine Gold Production | 173,490 oz |

| Life of Mine Silver Production | 1,530,650 oz |

| Initial Capital Costs (including indirects) | US$33 million |

| Operating Costs (@5,000 tpd) | US$13.19/tonne |

| Gold Equivalent Ounces/yr (Avg. @5,000 tpd) | 42,000 oz/yr |

| Gold Equivalent Cash Cost (@5,000 tpd) | US$ 514.27/oz |

| Cash Cost net of Ag/oz (@5,000tpd) | US$409.07 |

| All-in Sustaining Costs AuEq**(LOM) | US$624.01/oz |

| NPV 5% after tax | US$55.25 million |

| IRR after tax | 44.3% |

| Payback Period after tax | 2.4 years |

Dick Whittington, President and CEO, states: "We are delighted that the Feasibility Study re-affirms the Moss Mine to be an economically robust, higher margin, lower risk project in one of the world's premier mining jurisdictions. We look forward to building on this solid foundation to position ourselves as a premier, development stage, junior gold mining company. We are also pleased to have now completed the final requirement of our earn-in. We will be formally submitting the BFS to Patriot shortly. We believe the BFS will clearly comply with our Earn-in Agreement and provide the Company with another transformative milestone going forward.

Dick Whittington added: "Our attention will now focus on securing the necessary financing to fund our 70% share of the costs to build the mine, as per the joint venture with Patriot. We believe the BFS will demonstrate the eminent financability of the Project as we are already in receipt of a major equipment financing proposal from a major US bank. In addition to direct equipment bank financing, we will be exploring both equity and debt financing with the various financial institutions and lenders we are currently in discussions with. It is an exciting time for the Company and we look forward to realizing on the potential that the Moss Mine project offers."

*Gold equivalent grades are defined in the footnotes to the Reserve Statement

**All-in Sustaining Costs ("AISC") as presented are defined by the World Gold Council ("WGC") less corporate G&A

The Moss Gold-Silver Project encompasses 15 patented lode claims covering 102.8 hectares and 468 unpatented lode claims for a total of 4,030.8 hectares. The focus of the Feasibility Study is the gold-silver mineralization associated with the Moss Vein, the West Extension and adjacent stockworks on the patented claims. All of the project facilities, including the open-pit, heap leach pad, waste dumps and other ancillary works are designed to be constrained wholly within the patented claims.

The Feasibility Study is based on contract mining for the full 5 year mine life. Mine production will ramp up from an initial 2,500 tpd at Month 1, to 3,500 tpd at Month 7 and then full production of 5,000 tpd in Month 13. The base assumptions assume a gold price of US$1,250/oz and a silver price of US$20/oz for the life of the project. Consumable prices for process reagents, cement, cyanide and fuel are based on quotes received from local vendors. Capital is based on equipment quotes received from suppliers and service providers.

The economic analysis was carried out using standard discounted cash flow modelling techniques. The production and cost estimates derived for the Feasibility Study were estimated on a monthly basis for all pre-production costs and for the first twelve months of production. Quarterly estimates were used for the remaining forty-eight months of production.

Applicable royalties were applied - the BHL, Greenwood and MinQuest royalties - current Federal and Arizona State taxes were incorporated into the cash flow model and the "unit of production" depreciation method was used to calculate net taxable income. The economic analysis was carried out on a project basis and does not take into account any potential tax savings available to Golden Vertex (see Phase I - Potential Future Tax Benefits, page 9). Given the location and relatively uncomplicated nature of the project, the Base Case uses a 5% discount factor in arriving at the project Net Present Value ("NPV"). Standard payback calculation methodology was also utilized.

The Feasibility Study was prepared by a team of independent specialist consultants that included M3 Engineering of Tucson, AZ (process facility and site infrastructure design and costing), Golder Associates of Tucson, AZ (heap leach design and costing and stormwater management designs and costing), SAB Mining Consultants of Hamilton, UK (mineral reserves, mine planning and production scheduling), MineFill Services, Inc. of Seattle, WA (pit geotechnical), Smith Water Management Consultants of Richmond, B.C. (groundwater resources), and CDM Smith of Phoenix, AZ (project permitting). The Feasibility Study team was managed by Dr. David Stone, PE of MineFill Services, Inc.

A detailed summary report of the Feasibility Study, in the form of a Technical Report, prepared and certified in accordance with NI 43-101, will be filed on SEDAR within the next 45 days.

Mineral Resource Estimate:

The Feasibility Study is based on the previously reported mineral resource estimate prepared by David Thomas, P.Geo. with an effective date of October 31, 2014. This estimate encompasses the Moss and Ruth Veins, the West Extension to the Moss Vein, and associated stockworks. The mineral resources, as reported in the December 30, 2014 Technical Report filed on SEDAR, are summarized in Table 1 below.

Table 1: Moss Project Mineral Resource Estimate - David Thomas, P. Geo. (Effective Date: October 31st, 2014)

| Category | Tonnes | Au | Ag | Au | Ag | Au Eq | Au Eq |

| (g/t) | (g/t) | (oz) | (oz) | g/t | (oz) | ||

| Moss & Ruth Veins | |||||||

| Measured | 4,265,000 | 1.03 | 10.9 | 141,000 | 1,490,000 | 1.17 | 160,000 |

| Indicated | 4,910,000 | 0.87 | 11.8 | 137,000 | 1,860,000 | 1.02 | 161,000 |

| Measured & Indicated | 9,175,000 | 0.94 | 11.4 | 278,000 | 3,350,000 | 1.09 | 321,000 |

| Inferred | 805,000 | 0.6 | 4.5 | 16,000 | 120,000 | 0.66 | 17,000 |

| West Extension | |||||||

| Measured | 595,000 | 0.54 | 7.3 | 10,000 | 140,000 | 0.63 | 12,000 |

| Indicated | 5,710,000 | 0.48 | 6.1 | 88,000 | 1,110,000 | 0.55 | 102,000 |

| Measured & Indicated | 6,305,000 | 0.48 | 6.2 | 98,000 | 1,250,000 | 0.56 | 114,000 |

| Inferred | 1,375,000 | 0.52 | 6.3 | 23,000 | 280,000 | 0.59 | 26,000 |

| Combined Total | |||||||

| Measured | 4,860,000 | 0.97 | 10.4 | 152,000 | 1,630,000 | 1.1 | 172,000 |

| Indicated | 10,620,000 | 0.66 | 8.7 | 225,000 | 2,980,000 | 0.77 | 263,000 |

| Measured & Indicated | 15,480,000 | 0.76 | 9.3 | 377,000 | 4,610,000 | 0.87 | 435,000 |

| Inferred | 2,180,000 | 0.55 | 5.6 | 38,000 | 390,000 | 0.62 | 43,000 |

Footnotes to Mineral Resource statement:

- The Mineral Resource estimate is constrained within a pit-constrained Lerchs-Grossman ("LG") pit with maximum slope angles of 65Γùª. Metal prices of US$1,250/oz and US$20/oz were used for gold and silver respectively. Metallurgical recoveries of 82% for gold and 65% for silver were applied.

- A 0.25 g/t gold cut-off was estimated based on a total process and G&A operating cost of US$6.97/t of ore mined.

- The gold equivalent ("AuEq") formulae, applied for purposes of estimating AuEq grades and ounces, are as follows:

- Factor A (gold) = 1 / 31.10346 x metallurgical recovery (82%) x smelter recovery (99%) x refinery recovery (99%) x unit Au price (US$1,250 / oz)

- Factor B (silver) = 1 / 31.10346 x metallurgical recovery (65%) x smelter recovery (98%) x refinery recovery (99%) x unit Ag price (US$20 / oz)

- AuEq grade = Au grade + (Ag grade x [Factor B / Factor A])

- AuEq ounces = (AuEq grade x material tonnes)/31.10346

- All figures have been rounded to reflect accuracy and to comply with securities regulatory requirements. Summations within the tables may not agree due to rounding.

- Mineral Resources which are not Mineral Reserves do not have demonstrated economic viability. The estimate of Mineral Resources may be materially affected by environmental, permitting, legal, title, taxation, sociopolitical, marketing, or other relevant issues.

- The quantity and grade of reported Inferred resources in this estimation are conceptual in nature and there has been insufficient exploration to define these Inferred resources as an Indicated or Measured Mineral Resource and it is uncertain if further exploration will result in upgrading them to an Indicated or Measured Mineral Resource category.

Mineral Reserve Estimate:

Mineral resources were estimated from conventional LG techniques to establish mineable shapes with the mineral resource block model and an optimum pit shell. Only Measured and Indicated resources can be upgraded to a mineral reserve. For the Feasibility Study, a detailed mine plan was developed within the LG defined pit, to which the detailed operating costs were then applied.

The Feasibility Study mine plan was purposefully restricted by the physical constraints of keeping the consequent heap leach pad and waste dump volumes on the patented land. No mine plan has been developed to evaluate the extraction of the remaining resources at this time.

Two cut-off grades were applied to the mineral reserves. Primary Ore material assumes an economic cut-off grade of 0.25 g/t Au whereas Low Grade Ore assumes a cut-off of 0.20 g/t Au. During mining it is assumed the Low Grade ore will be stockpiled for processing towards the end of the mine life when the Primary Ore nears depletion and there is insufficient ore feed for processing. The reserve figures include 5% dilution with zero grade waste and 95% in-pit mining recovery.

The final pit shell contains 5,570 tonnes of Inferred Resources above a cutoff grade of 0.2 g/t Au. These resources are not classed as mineral reserves and are not included in the mine production schedule or mine economics.

The results of the mineral reserve estimation are shown on Table 2.

Table 2: Moss Project Mineral Reserve Statement with an effective date of May 15, 2015 (Qualified Person: Scott Britton, C.Eng.)

| Material | Category | ROM (MT) |

Diluted Au (g/t) | Diluted Ag (g/t) | Contained Au (oz) | Contained Ag (oz) | Diluted AuEq (g/t) | Contained AuEq (oz) |

| Primary Ore | Proven | 4.20 | 0.95 | 10.01 | 128,160 | 1,352,030 | 1.07 | 144,490 |

| Probable | 3.30 | 0.75 | 9.20 | 79,770 | 976,260 | 0.86 | 91,240 | |

| Combined | 7.50 | 0.86 | 9.66 | 207,930 | 2,328,290 | 0.97 | 233,900 | |

| Low Grade Ore | Proven | 0.25 | 0.22 | 2.99 | 1,740 | 24,070 | 0.25 | 2,010 |

| Probable | 0.21 | 0.22 | 3.54 | 1,460 | 23,920 | 0.26 | 1,760 | |

| Combined | 0.46 | 0.22 | 3.24 | 3,190 | 47,980 | 0.25 | 3,700 | |

| ALL | Combined | 7.96 | 0.82 | 9.29 | 211,130 | 2,376,270 | 0.93 | 238,010 |

Footnotes to Mineral Reserve statement:

- The Mineral Reserve estimate is constrained within a pit-constrained LG pit with maximum slope angles of 65Γùª. Metal prices of US$1,250/oz and US$18.50/oz were used for gold and silver respectively. Metallurgical recoveries of 82% for gold and 65% for silver were applied.

- A variable gold cut-off was estimated based on a mining cost of US$2.75/t mined, and a total process and G&A operating cost of US$6.48/t of ore mined. Primary ore is based on a cut-off of 0.25 g/t Au, and low grade ore is based on a cut-off of 0.2 g/t Au.

- The gold equivalent ("AuEq") formulae, applied for purposes of estimating AuEq grades and ounces, are as follows:

- Factor A (gold) = 1 / 31.10346 x metallurgical recovery (82%) x smelter recovery (99%) x refinery recovery (99%) x unit Au price (US$1,250 / oz)

- Factor B (silver) = 1 / 31.10346 x metallurgical recovery (65%) x smelter recovery (98%) x refinery recovery (99%) x unit Ag price (US$18.50 / oz)

- AuEq grade = Au grade + (Ag grade x [Factor B / Factor A])

- AuEq ounces = (AuEq grade x material tonnes)/31.10346

- All figures have been rounded to reflect accuracy and to comply with securities regulatory requirements. Summations within the tables may not agree due to rounding.

- The Mineral Reserves were defined in accordance with CIM Definition Standards dated May 10, 2014.

- The Measured and Indicated Resources are inclusive of those Mineral Resources modified to produce the Mineral Reserves.

- Tonnages listed (ROM) are in millions of tonnes ("MT").

The above in-pit reserves do not include unprocessed ore mined during Phase I - Pilot Plant operations. The following table outlines the additional reserves available in stockpiles. The average grade of this material, including material previously classified as waste, exceeds the economic cut-offs applied in this study.

Table 3: Stockpile Reserves

| Existing Stockpiles | Au (g/t) | Ag (g/t) | Tonnes | Au (oz) | Ag (oz) | AuEq (g/t) | AuEq (oz) |

| High Grade Stockpile | 2.126 | 29.99 | 1,922 | 130 | 1,850 | 2.47 | 150 |

| Low Grade Stockpile | 0.854 | 10.70 | 23,913 | 660 | 8,230 | 0.98 | 750 |

| Waste Dump | 0.654 | 6.49 | 36,130 | 760 | 7,540 | 0.73 | 850 |

| Total | 0.777 | 8.84 | 61,965 | 1,550 | 17,620 | 0.88 | 1,750 |

Footnotes to Stockpile Reserves Statement:

- The footnotes to the Mineral Reserve Statement above apply to this estimate, where applicable.

- The Mineral Reserves reported for stockpiles are not included in the Mineral Resources.

- The Mineral Reserves for stockpiles are based on legal surveys conducted by a registered Land Surveyor (for volumes), and trench samples on 4.5m centers cut across the stockpile to generate bulk samples which were split into 3 assay splits for analysis by fire assay with a gravimetric finish (for grade). Based on the surveys and sampling the stockpiles were deemed to be classed as Probable Reserves based on the CIM definitions.

Mining:

Mine design has been tailored to take advantage of the natural linear structural features of the Moss deposit. An East-West, on-strike, trench pit design has been utilized allowing for the efficient planning of in-pit haul roads and enabling the competent nature of the host rocks to be taken advantage of. As a result, final pit walls are designed to a 65 degree angle, with in-pit haul roads being established in the more competent footwall structure.

Final pit wall angles for the Moss open-pit are based on a thorough review of the available kinematic data from surface mapping and oriented core drill holes, and a rock quality assessment based on fracture frequencies and rock mass strengths. Rock strengths in the monzonite host rocks range from 50 MPa to 110 MPa and RQD values typically exceed 80% below an upper weathered zone of 10m to 20m. Pit wall stability will be controlled by structural features in the rock mass, most likely in the form of wedges on the hanging wall, and planar or sliding failures on the footwall. An observational approach to management of pit wall stability will be adopted for mining including bench mapping of discontinuities, local scaling of unstable wedges, and regular inspections of benches to ensure safe mine operations.

The mine plan assumes a series of push-backs, in the hanging wall, to achieve a balanced production of waste rock and ore material over the life of the mine. The pit will be developed in 6m mining benches with conventional drill and blast equipment. The final pit shell assumes 65 degree pit walls with double benches, 3m wide berms, and 10m wide haul roads. The mine production schedule is shown in Table 4 below. Tonnages are in millions of tonnes ("MT").

Table 4: Mine Production Schedule

| Category | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Total |

| Total In-Pit Material MT | 3.5 | 6.0 | 4.3 | 4.3 | 2.9 | 21.0 |

| Waste MT | 2.4 | 4.2 | 2.4 | 2.5 | 1.6 | 13.0 |

| Strip Ratio | 2.1 | 2.3 | 1.3 | 1.4 | 1.2 | 1.6 |

| Total ROM MT | 1.135 | 1.809 | 1.903 | 1.822 | 1.293 | 7.962 |

| Au g/t (diluted) | 0.86 | 0.84 | 0.82 | 0.59 | 1.11 | 0.82 |

| Ag g/t (diluted) | 8.69 | 9.01 | 9.53 | 7.14 | 12.84 | 9.28 |

| Primary ROM MT | 1.079 | 1.688 | 1.781 | 1.690 | 1.262 | 7.500 |

| Au g/t (diluted) | 0.89 | 0.88 | 0.87 | 0.62 | 1.13 | 0.86 |

| Ag g/t (diluted) | 8.99 | 9.46 | 9.96 | 7.41 | 13.06 | 9.66 |

| Low Grade ROM Tonnes | 0.056 | 0.121 | 0.121 | 0.132 | 0.031 | 0.461 |

| Au g/t (diluted) | 0.21 | 0.22 | 0.22 | 0.22 | 0.22 | 0.22 |

| Ag g/t (diluted) | 2.85 | 2.81 | 3.26 | 3.67 | 3.70 | 3.24 |

Mining will produce roughly 13 million tonnes (MT) of waste rock during the life-of-mine. The project facilities include the capacity to store 14 MT of waste on the patented claims including 2.7 MT placed as backfill into the mined out open-pit, and 0.6 MT classed as low grade ore in stockpiles.

Metallurgy:

Bench scale and pilot scale metallurgical testing have shown the Moss deposit mineralization to be amenable to precious metals recovery by cyanide leaching in a heap leach environment. Metal recoveries are sensitive to the crush size due to the partial encapsulation of gold in quartz, however excellent recoveries have been achieved with a crush size of P99 = 6.35mm. The Moss Mine mineralization exhibits slow leach kinetics and requires 270 days to achieve over 80% gold recoveries.

Pilot heap operations in Phase I were used to confirm the total precious metals recovery, and recovery curves for commercial operations. The pilot heap achieved a total gold recovery of 82%, and a total silver recovery of 38%. The low silver recoveries in the pilot heap can be attributed to the carbon-in-pulp recovery plant which typically performs poorly with silver. A Merrill Crowe process was thus selected for the Phase II commercial operations in order to maximize the recovery of silver, and to allow the production of doré bars on site.

Full details of the metallurgical testing and the conclusions used in the Feasibility Study are included in the Technical Report filed on SEDAR on December 30th, 2014.

Processing:

Ore from the open pit will be crushed to 6.35 mm and then agglomerated with cement prior to loading on the heap leach pad in 10m lifts. The crushing circuit will employ three stages of crushing consisting of a primary jaw crusher, a secondary cone crusher, and a two-stage tertiary cone crusher. After agglomeration, the fine ore will be conveyed to the leach pad with a series of grasshopper conveyors feeding a radial stacker.

Owing to space constraints at the project site, it will be necessary to relocate the crusher to the top of the waste dump in Month 30. The sustaining capital includes an allowance for relocating the crusher. The crusher move is expected to take 2 weeks, during which time the heap leach will operate as normal.

The heap leach pad has been designed to accommodate 8.5 MT of ore. The pad covers an area of 215,000m2 and will be constructed in 3 stages. During peak operations some 45,000m2 of pad area will be under leach. Pregnant solution from the heap will be fed to the Merrill Crowe plant at rate of about 450 m3/hr. The precious metals will be precipitated with zinc for filtration and subsequent melting in a furnace. The doré bars will be shipped by armored car service to a precious metals refiner.

Table 5: Gold and Silver production (oz/year) by year are highlighted below:

| 1 | 2 | 3 | 4 | 5 | 6 | Total | |

| Au | 17,227 | 37,086 | 41,581 | 30,589 | 37,378 | 11,383 | 175,244 |

| Ag | 135,300 | 316,372 | 366,006 | 288,554 | 349,330 | 106,322 | 1,561,884 |

| AuEq | 19,392 | 42,148 | 47,437 | 35,206 | 42,968 | 13,084 | 200,234 |

Infrastructure and Services:

The Moss Mine site is not connected to the main electrical grid that serves Mohave County, hence the Feasibility Study assumes diesel power generation using five 750kW generators. Three of the generators will be located at the crusher, and two will be located at the Merrill Crowe plant.

The primary water source for the heap leaching operations will be groundwater wells and dewatering of the open-pit. It is anticipated that a regional groundwater assessment program will prove the availability of the heap leach make-up water requirements which are estimated to be 190 gpm on average and 260 gpm on a peak demand basis. The divergence between these numbers is directly linked to seasonal climatic variations which will allow for the effective management of water resources in and around the operations. The Feasibility Study budget includes an allowance for regional groundwater exploration in areas of known water occurrence.

In the event the project has a water deficit from available groundwater resources, two options are available. The first is to temporarily reduce the daily throughput to reduce the make-up water demand, and the second is to construct a water line from Bullhead City. The City has offered to sell water to the Project should it be needed.

Capital Estimate:

The Feasibility Study capital estimate is based on vendor quotes for all the major capital items including conveyors, crushers, the Merrill Crowe facility, heap leach pad construction (earthworks and liners), and other ancillary works.

Capital savings of approximately US$1.3 M were achieved by the re-use and recycle of components already purchased for the Phase I pilot heap operations. This included office trailers, laboratory facilities, staff vehicles, solution pumps, twelve 10,000 gallon water tanks, a 350 tonne cement silo, and the re-use of the spent ore from the Phase I heap for inter-liner material in the Phase II leach pad area.

Total initial capital costs are estimated at US$33.0 M comprising US$24.8 M in direct costs, US$4.3 M in indirect costs, a 7.5% contingency on the direct and indirect costs and US$1.65 M in owner costs.

Table 6: Initial Capital Cost Estimate

| Area | Capital (US$) | |

| Site General Costs | $ | 895,619 |

| Mine Equipment * | $ | - |

| Primary Crushing | $ | 1,914,626 |

| Fine Crushing | $ | 4,311,434 |

| Crushed Ore Transfer | $ | 1,479,804 |

| Leach Pad Piping | $ | 1,482,549 |

| Leach Pad Earthworks/Liner | $ | 5,251,058 |

| Pond Earthworks/Liner | $ | 1,202,534 |

| Merrill Crowe | $ | 4,410,729 |

| Refinery | $ | 1,726,463 |

| Water Systems | $ | 1,062,094 |

| Power Generation | $ | 838,330 |

| Reagents | $ | 195,297 |

| Ancillary | $ | 68,348 |

| TOTAL DIRECT COSTS | $ | 24,838,885 |

| INDIRECTS | $ | 4,339,641 |

| CONTINGENCY | $ | 2,180,434 |

| OWNERS COSTS | $ | 1,650,000 |

| TOTAL CAPITAL COST | $ | 33,008,960 |

*Mining equipment is being supplied by the mining contractor.

The Company is in receipt of a non-binding offer from a major US banking institution, to finance the purchase of a portion of the capital equipment. The offer terms include a lease-to-own financing for 60 months, subject to customary underwriting approvals. If implemented, this financing alternative provides a significant improvement to the IRR for the project with little change to the NPV.

Operating Costs:

Operating costs were calculated in three areas - Mining, Process and G&A. Mining costs were derived directly. As contemplated in the Company's Preliminary Economic Assessment, the Company invited several industry experienced mining contractors to submit bids for the mining component of the Feasibility Study. The Company intends to select the preferred contractor and proceed to negotiate a Services Contract with the successful bidder. Process and G&A operating costs were estimated largely from first principles and from quotes for some of the major consumables including cyanide, cement, and fuel. The life of mine operating cost estimate is shown in Table 7 below:

Table 7: Operating Cost Estimate - per tonne processed

| Mining | US$5.96/tonne |

| Process | US$6.65/tonne |

| General/Administration | US$0.95/tonne |

| TOTAL OPERATING COST | US$13.56/tonne |

Project Economics and Sensitivity Analyses:

The following tables illustrate the Base Case project economics and the sensitivity of the project to changes in the base case metal prices, operating costs and capital costs. As is typical with precious metal projects, the Moss project is most sensitive to metal prices, followed by operating costs, and initial capital costs.

Table 8: Project Economics

| Pre-Tax | After-Tax | |

| NPV@ 5% | US$75.30 M | US$55.30 M |

| IRR% | 54.6% | 44.3% |

| Payback (yrs) | 2.3 | 2.4 |

Table 9: Metal Price Sensitivity - After-Tax

| Metal Price Sensitivity | |||||||

| Gold Price (US$) | Silver Price (US$) | NPV @ 0% (US$) | NPV @ 5% (US$) | NPV @ 10% (US$) | IRR | Payback | |

| +20% | $1,500 | $24 | $103,667,000 | $84,231,000 | $68,709,000 | 62.7% | 2.1 |

| +10% | $1,375 | $22 | $87,063,000 | $69,817,000 | $56,056,000 | 53.7% | 2.2 |

| 0% | $1,250 | $20 | $70,288,000 | $55,253,000 | $43,271,000 | 44.3% | 2.4 |

| -10% | $1,125 | $18 | $52,954,000 | $40,199,000 | $30,050,000 | 34.2% | 2.7 |

| -20% | $1,000 | $16 | $34,861,000 | $24,454,000 | $16,195,000 | 23.2% | 3.3 |

Table 10: Operating Cost Sensitivity - After-Tax

| Operating Cost Sensitivity | |||||

| NPV @ 0% (US$) | NPV @ 5% (US$) | NPV @ 10% (US$) | IRR | Payback | |

| +20% | $55,493,000 | $42,171,000 | $31,581,000 | 34.7% | 2.7 |

| +10% | $63,010,000 | $48,824,000 | $37,530,000 | 39.5% | 2.6 |

| 0% | $70,288,000 | $55,253,000 | $43,271,000 | 44.3% | 2.4 |

| -10% | $77,259,000 | $61,415,000 | $48,775,000 | 48.8% | 2.3 |

| -20% | $84,082,000 | $67,448,000 | $54,165,000 | 53.4% | 2.2 |

Table 11: Capital Cost Sensitivity - After-Tax

| Capital Cost Sensitivity | |||||

| NPV @ 0% (US$) | NPV @ 5% (US$) | NPV @ 10% (US$) | IRR | Payback | |

| +20% | $66,008,000 | $50,653,000 | $38,414,000 | 36.4% | 2.6 |

| +10% | $68,162,000 | $52,966,000 | $40,854,000 | 40.1% | 2.5 |

| 0% | $70,288,000 | $55,253,000 | $43,271,000 | 44.3% | 2.4 |

| -10% | $72,384,000 | $57,515,000 | $45,665,000 | 49.1% | 2.3 |

| -20% | $74,457,000 | $59,757,000 | $48,043,000 | 55.0% | 2.2 |

Manpower:

The project is expected to employ a full-time staff of 83 at the 5,000 tpd production rate. The staffing includes 18 for the contract miner, 49 in the process plant, and 16 general and administrative staff.

Permitting:

All of the facilities of the Moss Project that are the subject of this Feasibility Study, have been constrained to be entirely within the boundaries of the 15 patented claims. This will allow the project to be developed exclusively on private land pursuant to applicable state and federal law. This development plan will allow early development of the Moss Project as the timelines for permit approvals on patented lands are shorter than those that would be required if mining on the unpatented claims are incorporated into the development plan. Mine life extension studies and exploration programs on the unpatented claims will be investigated once the mine is in production. If economic, an appropriate mine plan of operations would be submitted to the Bureau of Land Management ("BLM"), Kingman Field office for review and approval. Additionally, if additional economic resources are discovered on the unpatented claims, and feasibility studies indicate economic potential, further submittals to the BLM will be made at that time.

The Moss Mine recently operated as a fully permitted pilot plant heap leach, Phase I - Pilot Plant, including all permit approvals for the mining, crushing, and heap leaching of roughly 175,000 tonnes of ore and waste. The permits required for Phase II - Operations are similar to those that were approved as part of the Phase I - Pilot Plant. Additional permitting required pursuant to Section 404 of the Clean Water Act will be necessary, but applied for later in the mine's life. In addition to the numerous routine permits/approvals, in order to commence production and proceed to Phase II - Operations, the Company will need the following permits to be amended and/or approved:

- Aquifer Protection Permit Amendment

- Air Quality Permit

- Arizona Reclamation Plan Amendment

- Arizona Storm Water Permit (AZMSGP)

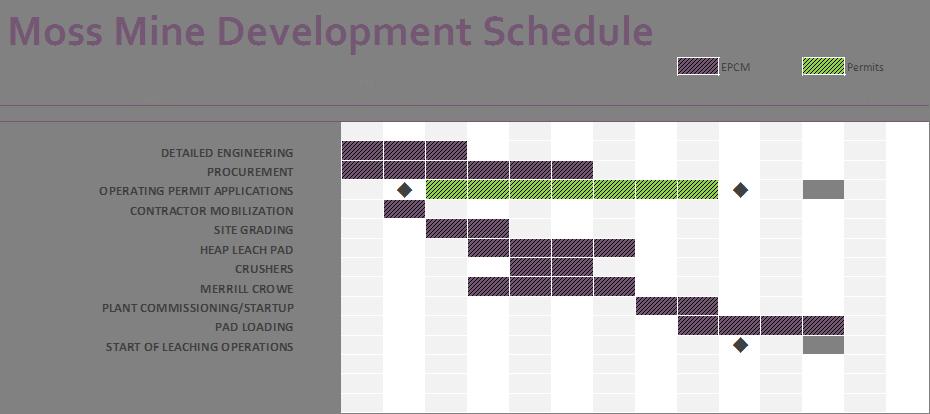

Project Development Timeline:

Several advantages accrue to the development timeline, given the location of the project in Arizona and it being so close to the city of Bullhead City. Significant savings in time and costs can be achieved as a result of the ease of access to the deposit, the relative simplicity of the site geography and topography and the ability to source key supplies from Bullhead City, Phoenix or suppliers in Nevada, none of which are more than a day's drive away from the site. In addition, the ability to access ore without the necessity of any pre-strip mining, the trench pit mine design and the well tested mining and processing technology being utilized, all further reduce timeline and cost overrun risks. The size of the planned operation - approximately 5,000 tpd - enables both equipment and supplies to be "off the shelf", thereby reducing equipment operating, maintenance or key parts re-supply risks.

The development timeline reflects the favorable year-round climate and accessibility of the Project. The detailed development timeline is shown below:

To view Table 12: Moss Mine Development Schedule, please visit the following link: http://media3.marketwire.com/docs/nv_1.jpg

{kind=link}

Corporate Initiatives/Socio-Economics:

Northern Vertex, through its US subsidiary, Golden Vertex, is endeavoring to be an organization recognized for its safety culture, community commitment, Tribal involvement, educational enhancement, open communication culture and transparency that will create a legacy for the stakeholders in the Bullhead City area for many years to come. Since December 2012, the Company has established the means to achieve this goal as follows:

- The Company's safety record during Phase I - Pilot Plant operations was exemplary with no loss time accidents or MSHA reportable incidents occurring. The Company was awarded two State/National awards as a result.

- A community enhancement plan was initiated to establish a cultural and heritage center in Bullhead City's Community Park. The first phase of that initiative was completed in August 2013 and the second phase is expected to be completed later this year. The intention is to have a central location to celebrate and showcase the unique and diverse local history of the Bullhead City area with specific recognition of the important role the Colorado River played in this history with various stakeholders providing exhibits.

- The Company has had continuous dialogue with the local Fort Mojave Tribe, to ensure the Tribe is informed and up to date about the Company's activities and to discuss possible job training programmes for the mine when in production. Where possible, site visits have been conducted to illustrate the nature and location of the Company's mine development plans and site cultural surveys have been carried out. Other Tribes in the region have been visited and informed of the Company's activities.

- An educational enhancement programme was initiated to facilitate the establishment of an Earth Sciences programme at Mohave High School along with a pathway to a mining engineering degree - or related tertiary education - at the University of Arizona. Site visits by students are actively encouraged and the Company's goal is to have senior mine staff be locally educated.

- Each month, the Moss Mine Project advisory Council - a volunteer group chaired by an individual independent of the Company - meets to discuss the latest developments related to the project. The Company presents its updates to this forum which is open to key stakeholders in the region and to the general public.

- Continuous contact is also maintained with the local government institutions - Bullhead City Council, Mohave County Board of Supervisors, Arizona State government representatives and local Federal Congressional elected officials and staff. Site visits have been conducted with all these key parties.

As the Feasibility Study contemplates a mine developed exclusively on patented lands, there are no land ownership conflicts or specific surface use agreements that have to be negotiated. The mine will be accessed via an existing road, which has been used for over 100 years for mining and related activities in the surrounding area. The road crosses public land on which the Company owns or controls unpatented mining claims associated with the mine. The mine is removed from the nearest community - Bullhead City - and does not infringe upon any other land uses apart from periodic off-road recreational activities. The Company remains focused on working effectively and respectfully with local stakeholders to enhance the capacity of the local communities in the area.

Corporate Considerations:

- Phase I - Potential Future Tax Benefits

As of March 31, 2015, as a result of the "earn-in" expenditures incurred as part of the Earn-in Agreement, operating losses and head office expenditures attributable to the support of mining activities at the Moss Mine, the Company has approximately US$30.9 million tax deduction pools that can be applied directly to the Company's 70% share of taxable income to off-set future tax liabilities. Applying these offsets to the Company's portion of the Joint Venture will significantly enhance the project's economics from the Company's perspective. These potential tax reductions have not been included in the Base Case analysis presented earlier.

- Financing Activities

The Company is currently in discussions with several potential equity and debt providers. The finalization of the Feasibility Study will enable these discussions to be elevated and to become more substantive in nature. In addition, equipment financing options have been actively explored and proposals are being entertained. As mentioned above, a major US bank has provided a non-binding proposal to finance the crushing, screening, agglomeration and stacking equipment included in the capital costs outlined in the sections above - approximate value US$6.5 million. The combination of equipment financing and other debt and equity financing is anticipated to be the optimal combination to fund the project going forward; however, at this time, funds are not available to proceed with the project and an active fund raising effort will be required prior to the project commencing.

- Pending Arbitration

As previously announced, the Company and Patriot Gold are engaged in an arbitration process under the Earn-in Agreement in connection with certain allegations by Patriot that, amongst other items, allege that a) the pilot plant was profitable and that Patriot is entitled to the profits, and b) that the scope of the Feasibility Study, as it relates to the BFS requirement under the Earn-in Agreement, is too limited by focusing on the patented Moss lands only. Northern Vertex's position is that it is completely within its discretion under the Earn-in Agreement to evaluate a mine within the patented lands of the Moss Project given that a mine outside the patented area will be subject to significant additional risks and delays. The evaluation of a patented lands first strategy does not negate or even reduce the likelihood that the mine will be capable of being expanded to include potential future resources should those resources be discovered and be deemed economic. The timing and outcome of the arbitration cannot be predicted with any degree of certainty at this time.

- Exploration Potential

Exploration potential is considered to be excellent both adjacent to the Main Moss Vein System, both on strike and to depth, as well as property wide. The potential of the former - mine exploration potential - is highlighted in the December 30th, 2014 Technical Report filed on SEDAR. Additionally, regarding property wide exploration potential, the Company has completed a field geological mapping and sampling program on areas outside of the main Moss vein system. As exploration to date has only focused on known mineral occurrences, only approximately 5% of the property has been explored to date.

Reconnaissance mapping followed by a rock chip sampling program, was carried out to investigate a number of vein trends on the Company's unpatented claims surrounding the flagship Moss Deposit. A significant number of samples showed evidence of gold mineralization with a portion having gold grades in excess of 1 gpt indicating that a number of vein exposures on the property are auriferous at surface with others showing alteration and trace elements that indicate their surface expression is within the boiling zone where gold might be found in the system - see news release dated March 24, 2015.

Several target areas remain to be sampled and others require follow-up sampling to further define their potential. The company plans to assess the prospects for a property wide drilling program to test the potential for further discoveries on the Moss and Silver Creek claims. Given the success to date, the Company believes that the prospects for additional discoveries of gold bearing veins and structures continue to be good.

About Northern Vertex

Northern Vertex Mining Corp. is a Canadian based exploration and mining company focused on the reactivation of the Moss Mine Gold-Silver Project located in NW Arizona, USA where the Company has the right to earn-in to a 70% property interest through a Joint Venture with Patriot Gold Corp. The Moss Mine Gold-Silver Project is an epithermal, brecciated, low sulphidation quartz-calcite vein and stockwork system which extends over a strike length of 1,400 meters and has been drill tested to depths of 370 meters below surface. It is a potential heap leach, open-pit project being advanced to the Feasibility Study stage to ensure that technical, economic, permitting and funding requirements are met prior to proceeding with the development of the mine. The Company's management comprises an experienced management team with a strong background in all aspects of acquisition, exploration, development, operations and financing of mining projects worldwide. The Company is focused on working effectively and respectfully with our stakeholders in the vicinity of the historical Moss Mine and enhancing the capacity of the local communities in the area.

Qualified Persons

The foregoing technical information contained in this news release has been approved by Messrs. Scott Britton, C.Eng., and Dr. David Stone, P.Eng., who are both independent Qualified Persons ("QP") for the purpose of NI43-101.

ON BEHALF OF THE BOARD OF DIRECTORS

J.R.H. (Dick) Whittington, President & CEO

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements: The information in this news release has been prepared as at June 5, 2015. Certain statements in this news release, referred to herein as "forward-looking statements", constitute "forward-looking statements" under the provisions of Canadian provincial securities laws. These statements can be identified by the use of words such as "expected", "may", "will" or similar terms.

Forward-looking statements are necessarily based upon a number of factors and assumptions that, while considered reasonable by the Company as of the date of such statements, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Many factors, known and unknown, could cause actual results to be materially different from those expressed or implied by such forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date made. Except as otherwise required by law, the Company expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any such statements to reflect any change in the Company's expectations or any change in events, conditions or circumstances on which any such statement is based.

Cautionary Notes to U.S. Investors Concerning Reserve and Resource Estimates

The definitions of Proven and Probable Reserves used in National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101") differ from the definitions in the United States Securities and Exchange Commission ("SEC") Industry Guide 7. Under SEC Guide 7 standards, a "Final" or "Bankable" feasibility study is required to report reserves, the three year history average price is used in any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority.

In addition, the terms "Mineral Resource", "Measured Mineral Resource", "Indicated Mineral Resource" and "Inferred Mineral Resource" are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and normally are not permitted to be used in reports and registration statements filed with the SEC. Investors are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into Reserves. "Inferred Mineral Resources" have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases.

Accordingly, information contained in this News Release, and on the Company's website, containing descriptions of Northern Vertex's mineral deposits may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations there under.

2015 number 06

Contact Information:

Investor Relations

604-601-3656 or 1-855-633-8798

www.northernvertex.com