GREENWICH, CT--(Marketwire - May 30, 2012) - Oxford Lane Capital Corp. (

| Investment | S&P / Moody's Original Ratings | S&P / Moody's Current Ratings* | Stated Maturity | Manager | NAV %** | |||||

| Waterfront CLO 2007 - Class D Notes | BB/Ba2 | BB/Ba3 | 8/2/2020 | Grandview Capital Management | 10.0% | |||||

| CIFC Funding 2006-1X Class B2L Notes | BB/Ba2 | BB/Ba3 | 10/20/2020 | Commercial Industrial Finance Corp. | 9.7% | |||||

| Harbourview CLO 2006-1 Sub Notes | NR | NR | 12/27/2019 | Harbourview Asset Management Corp | 8.3% | |||||

| Hewett Island CLO III - Class D Notes | BB/Ba2 | CCC-/B2 | 8/9/2017 | CypressTree Investment Management Co | 6.9% | |||||

| Jersey Street CLO Income Notes | NR | NR | 10/20/2018 | MFS Investment Management | 5.8% | |||||

| Emporia III, Ltd. 2007-3A Class E Notes | BB/Ba2 | B+/B1 | 4/23/2021 | Emporia Capital Management | 5.8% | |||||

| Kingsland IV, Ltd. 2007-4A Sub Notes | NR | NR | 4/16/2021 | Kingsland Capital Management | 5.3% | |||||

| Mountain Capital 2005-4X Class B2L Notes | BB/Ba2 | BB+/Ba3 | 3/15/2018 | Mountain Capital Advisors | 5.1% | |||||

| Octagon XI CLO 2007-1A Income Notes | NR | NR | 8/25/2021 | Octagon Credit Investors | 4.8% | |||||

| Lightpoint CLO VII, Ltd. 2007-7X Sub Notes | NR | NR | 5/15/2021 | LightPoint Capital Management | 3.9% | |||||

| Kingsland V, Ltd. 2007-5X Class E Notes | BB/Ba2 | B/Ba3 | 7/14/2021 | Kingsland Capital Management | 3.6% | |||||

| Hillmark Funding Ltd. 2006-1A Sub Notes | NR | NR | 5/21/2021 | HillMark Capital Management | 3.5% | |||||

| Canaras Summit CLO 2007-1 - Income Notes | NR | NR | 6/19/2021 | Canaras Management | 3.4% | |||||

| GSC VIII - Class D Notes | BB/Ba2 | B+/B1 | 4/17/2021 | Black Diamond Capital Management | 3.3% | |||||

| Rampart CLO 2007-1A Sub Notes | NR | NR | 10/25/2021 | Stone Tower Debt Advisors | 3.0% | |||||

| Gale Force 4 CLO 2007-4A Income Notes | NR | NR | 8/20/2021 | GSO/Blackstone Debt Funds Management | 2.9% | |||||

| PPM Grayhawk CLO 2007 - Class D Notes | BB/Ba2 | CCC+/Ba3 | 4/18/2021 | PPM America | 2.9% | |||||

| Hewett's Island CLO IV - Class E Notes | BB/Ba2 | CCC+/Ba3 | 5/9/2018 | LCM Asset Management | 2.8% | |||||

| Cent CDO 15 - Class D Notes | BB/Ba2 | BB/Ba3 | 3/11/2021 | RiverSource Investments | 2.6% | |||||

| Bridgeport CLO II - Class D Notes | BB/Ba2 | BB/Ba3 | 6/18/2021 | Deerfield Capital Management | 1.8% | |||||

| Canaras Summit CLO 2007-1 - Class E Notes | BB/Ba2 | B+/Ba3 | 6/19/2021 | Canaras Management | 1.3% | |||||

| Cash | 3.9% |

Source: Bloomberg L.P. ("Bloomberg"), Standard & Poor's Ratings Services ("S&P"), and Moody's Investors Service, Inc. ("Moody's")

NR - Not Rated.

* Ratings are current as of May 29, 2012

** NAV % adds up to greater than 100% due to liabilities on the balance sheet.

Investment Composition

The investments held by the CLO vehicles were primarily in companies domiciled in the United States (approximately 94%(1)). The top 10 aggregate industry exposures of the CLO vehicles accounted for approximately 56%1 of combined investments while the top 10 aggregate single obligor investments accounted for approximately 4%1 (please refer to the following two tables). This results in a weighted average diversity score of 69(2) for our portfolio (which we believe is broadly comparable to industry diversity scores for other similar CLO vehicles).

| Top Ten Industry Exposures*3 | Ten Largest U.S. Debt Securities3 | |||||

| Healthcare, Education & Childcare | 11.0% | Univision Communications Inc - TL | 0.69% | |||

| Broadcasting and Entertainment | 9.0% | Asurion LLC - TL | 0.44% | |||

| Diversified/Conglomerate Services | 5.7% | HCA - TL B3 | 0.41% | |||

| Telecommunications | 5.4% | Cequel Communications - TL | 0.36% | |||

| Electronics | 5.1% | Charter Communications - TL C | 0.35% | |||

| Chemicals, Plastics & Rubber | 4.7% | Del Monte Foods Company - TL | 0.34% | |||

| Retail Stores | 4.7% | RPI Finance Trust - TL | 0.33% | |||

| Finance | 3.7% | Onex Carestream Finance LP - TL | 0.32% | |||

| Utilities | 3.7% | Transdigm Inc - TL | 0.32% | |||

| Automobile | 3.3% | DA Vita Inc - TL | 0.30% | |||

| Total | 56.2% | Total | 3.85% | |||

| Source: Intex | Source: Intex |

* Reflects industry classifications established by Moody's.

CLO Compliance

As of March 31, 2012, each of the CLO vehicles was in material compliance with all of its respective collateral and coverage tests that were necessary for full payments to be made to the Company by each CLO vehicle.(4) The current weighted average over-collateralization ("OC") cushion for the Company's CLO equity and debt investments was approximately 2.0% and 4.5%, respectively, as of March 31, 2012 (compared to 1.8% and 4.3%, respectively as of December 31, 2011). As long as each CLO vehicle maintains a positive OC cushion with respect to the OC test associated with that CLO investment, a full payment is expected to be made to the Company.(5)

CLO Credit Quality

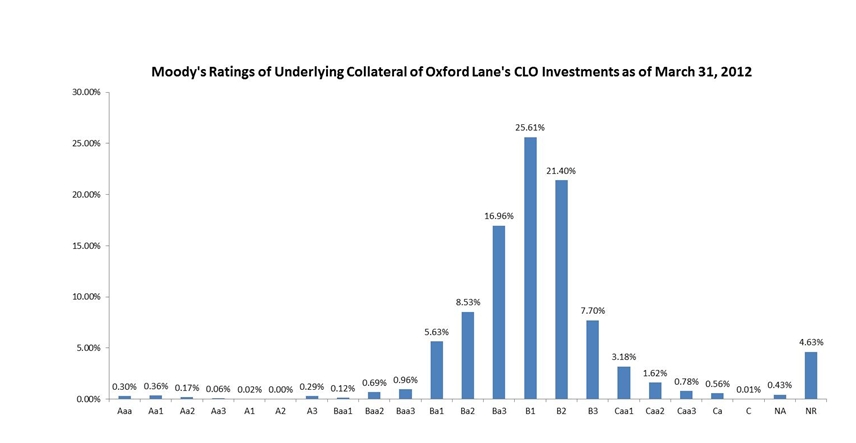

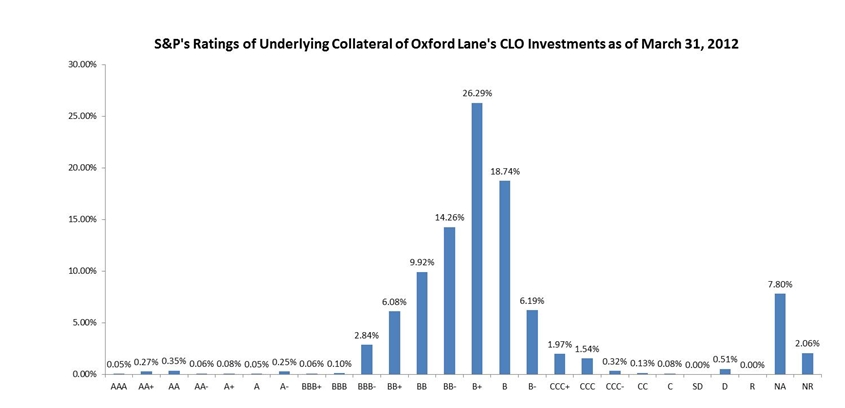

The current weighted average percentage of defaulted securities held by the CLOs (as reported by each CLO) was approximately 1.0% as of March 31, 2012 (compared to 0.8% as of December 31, 2011). The CLO vehicles which the Company has invested in have a weighted average WARF score (Weighted Average Rating Factor) of 2503 (compared to 2514 as of December 31, 2011) which is equivalent to a Moody's credit rating of between B1 and B2 (see ratings charts on the next page), based on a ratings factor scale provided by Moody's. We believe the weighted average WARF score of our portfolio is broadly comparable to industry WARF scores for other similar CLO vehicles.

Company Profitability

The Company received cash payments of $400,138 and $1,658,161 from its junior debt and equity tranche investments, respectively, for the quarter ending March 31, 2012. These payments represented a quarterly cash return of approximately 1.7% and 9.7% of the junior debt and equity tranche investments at market value (as of March 31, 2012), respectively, and on a combined basis, represented a quarterly cash return of approximately 5.1% of the Company's total portfolio at market value (as of March 31, 2012). For the quarter ending March 31, 2012 the Company received a full payment from each CLO vehicle (see table below).

| % NAV | ||

| Distributions paid by the CLOs for the 3-months ending 3/31/12 | 100.0% | |

| Distributions diverted for 3-months ending 3/31/12 | 0.0% | |

The approximate weighted average WAS (Weighted Average Spread above LIBOR) for the CLO vehicles in which the Company has an equity investment was 3.6% and the approximate weighted averaged WACC (Weighted Average Cost of Capital above LIBOR) was 0.5% resulting in approximately a 3.1% margin (before CLO vehicle expenses) as of March 31, 2012 (compared to a weighted average WAS and WACC of 3.5% and 0.5%, respectively, as of December 31, 2011). The weighted average reinvestment end date for the Company's equity positions was December 31, 2013 (with a final legal weighted average maturity date of October 1, 2020) which potentially allows for 1.75 more years of full equity distribution payments followed by up to 6.75 years of decreasing distribution payments to the Company, subject to CLO covenant compliance. During the quarter ending March 31, 2012, the Company received a weighted average cash distribution payment on its equity portfolio of approximately 8.1% (of par) with a price markup of approximately 10.8% (of par) from the prior quarter-end valuations (see table below).

| Equity Investments | Stated Maturity | Payments in Q4 as a % of par |

Price Change from 12/31/11 Mark | ||||

| Canaras Summit CLO 2007-1 - Income Notes | 6/19/2021 | 10.54 | 10.00 | ||||

| Gale Force 4 CLO 2007-4A Income Notes | 8/20/2021 | 6.93 | 17.00 | ||||

| Harbourview CLO 2006-1 Sub Notes | 12/27/2019 | 7.81 | 17.25 | ||||

| Hillmark Funding Ltd. 2006-1A Sub Notes | 5/21/2021 | 8.10 | 0.00 | ||||

| Jersey Street CLO Income Notes | 10/20/2018 | 7.30 | 5.50 | ||||

| Kingsland IV, Ltd. 2007-4A Sub Notes | 4/16/2021 | 7.56 | 19.75 | ||||

| Lightpoint CLO VII, Ltd. 2007-7X Sub Notes | 5/15/2021 | 8.44 | 13.50 | ||||

| Octagon XI CLO 2007-1A Income Notes | 8/25/2021 | 8.86 | 5.00 | ||||

| Rampart CLO 2007-1A Sub Notes | 10/25/2021 | 8.89 | 2.00 | ||||

| Weighted Average | 10/1/2020 | 8.11 | 10.77 | ||||

Source: Bloomberg

Oxford Lane Capital Corp.

Oxford Lane Capital Corp. is a publicly-traded registered closed-end management investment company. It seeks to achieve its investment objective of maximizing total return by investing primarily in senior secured loans made to companies whose debt is unrated or is rated below investment grade, with an emphasis on current income. Those investments may take a variety of forms, including the direct purchases of such loans (either in the primary or secondary markets) or through investments in entities that in turn own a pool of such loans.

Forward-Looking Statements

This press release contains forward-looking statements subject to the inherent uncertainties in predicting future results and conditions. Any statements that are not statements of historical fact (including statements containing the words "believes," "plans," "anticipates," "expects," "estimates" and similar expressions) should also be considered to be forward-looking statements. Certain factors could cause actual results and conditions to differ materially from those projected in these forward-looking statements. These factors are identified from time to time in our filings with the Securities and Exchange Commission. We undertake no obligation to update such statements to reflect subsequent events.

Disclaimer

This document has been prepared by Oxford Lane Capital Corp. and is the sole responsibility of the Company. No liability whatsoever (whether in negligence or otherwise) arising directly or indirectly from the use of this document is accepted and no representation, warranty or undertaking, express or implied, is or will be made by the Company or any of their respective directors, officers, employees, advisers, representatives or other agents ("Agents") for any information or any of the opinions contained herein or for any errors, omissions or misstatements. The Company has relied on certain information provided from Intex, Bloomberg, S&P and Moody's but makes no representation with respect to the accuracy of such information provided by Intex, Bloomberg, S&P or Moody's. Neither the Company nor any of its respective Agents makes or has been authorized to make any representation or warranties (express or implied) in relation to the Company or as to the truth, accuracy or completeness of this document, or any other written or oral statement provided. In particular, no representation or warranty is given as to the achievement or reasonableness of, and no reliance should be placed on any projections, targets, estimates or forecasts contained in this document and nothing in this document is or should be relied on as a promise or representation as to the future.

1 These percentages are based on the amount of CLO vehicles' underlying assets on a weighted average basis, without regard to the amount of the Company's investments in these CLO vehicles.

2 Source: Intex Solutions, Inc. ("Intex").

3 These percentages are calculated by taking the aggregate amount invested in the industries or debt securities and dividing by the aggregate amount of all of the CLO vehicles' underlying assets (excluding cash), without regard to the amount of the Company's investments in each of these CLO vehicles.

4 The CLO vehicles' indentures have a variety of covenant tests which those CLO vehicles may not be in compliance with in the future should credit markets deteriorate, the loans held by the CLO vehicles fail to make expected payments or otherwise not perform, or for a variety of other reasons. If those covenants are violated, it could result in principal paydowns of the CLO vehicles' higher-rated notes and/or interest diversion which may result in partial or non-payment of the quarterly amounts otherwise due to the Company.

5 Although we expect each of our current CLO equity and debt investments to maintain a positive OC cushion through maturity, there can be no assurance that such OC cushions will not be reduced to zero, either as a result of a deterioration in general economic conditions or other factors specific to the industries or specific companies in which such CLOs have invested. If that were to occur, our ability to receive payments on such CLO investments would be impaired, and we may lose a portion or all of our investment in such CLOs.

Contact Information:

Contact:

Bruce Rubin

203-983-5280