CALGARY, ALBERTA--(Marketwire - April 25, 2012) -

NOT FOR DISTRIBUTION TO U.S. NEWSWIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES OF AMERICA. ANY FAILURE TO COMPLY WITH THIS RESTRICTION MAY CONSTITUTE A VIOLATION OF U.S. SECURITIES LAWS.

Senmar Capital Corp. (TSX VENTURE:SMR.P) is pleased to announce, further to its news release dated March 27, 2012, that it has entered into an Amalgamation Agreement (the "Proposed Transaction") with Toscana Resource Corporation ("Toscana"). Senmar Capital Corp. ("Senmar") is also pleased to provide an update with respect to the sponsorship requirement and a technical update in connection with the Proposed Transaction.

Amalgamation Agreement

Toscana is a private company incorporated under the laws of Alberta and is engaged in the acquisition of long life oil and gas assets in Western Canada including royalties, non operating working interests and unitized production for yield and capital appreciation. Senmar is a "capital pool company" and intends for the Proposed Transaction to constitute its Qualifying Transaction as set forth in Policy 2.4 of the TSX Venture Exchange ("Exchange") Corporate Finance Manual (the "Manual"). The Proposed Transaction is not a Non-Arm's Length Qualifying Transaction as defined in the policies of the Exchange and it remains subject to the approval of the Exchange.

The Proposed Transaction is structured by way of a three corner amalgamation, in which Senmar will amalgamate with a wholly-owned subsidiary of Toscana (the "Subsidiary") pursuant to which the shareholders of Senmar will receive common shares in the capital of Toscana (the "Toscana Shares") in exchange for the common shares in the capital of Senmar ("Senmar Shares"), based on an exchange ratio of 0.01011879 of a Toscana Share for each Senmar Share (the "Exchange Ratio"). Following the amalgamation, the resulting issuer will be Toscana and the amalgamated entity will be a wholly-owned subsidiary of Toscana. Toscana will seek a listing for the Toscana Shares on the Exchange. The Proposed Transaction will require shareholder approval of both Senmar and the Subsidiary prior to the amalgamation being effected.

Senmar currently has 4,500,000 common shares issued and outstanding; 450,000 stock options exercisable at $0.20 per common share; and 250,000 agent's options exercisable at $0.20 per common share. As part of the Proposed Transaction, all of the foregoing unexercised Senmar stock options and agent's options shall be replaced with options in the capital stock of Toscana in accordance with the Exchange Ratio. Upon closing of the Proposed Transaction, the amalgamated Subsidiary will carry on the business of Toscana as currently constituted.

Sponsorship

Further to Senmar's news release dated March 27, 2012 wherein Senmar announced its intention to obtain a sponsor, Senmar has decided to make application to the Exchange that the Qualifying Transaction should be exempt from the sponsorship requirements in accordance with Policy 2.2 of the Manual. However, there can be no certainty that such an application for exemption from the sponsorship requirements will be granted by the Exchange and if not granted, GMP Securities LP has agreed to act as a sponsor in connection with this transaction.

Trading Halt

Trading in the shares of Senmar has been halted and will remain halted until such time as Senmar obtains the exemption in connection with the sponsorship requirements or is advised by the Exchange that such application will not be granted and Senmar engages a sponsor. There can be no assurance that trading in the shares of Senmar will resume prior to the completion of the Proposed Transaction.

Summary of Operational Information Relating to Toscana

Toscana was incorporated under the Business Corporations Act (Alberta) on March 2, 2010 by Toscana Merchant Group, an association of oil and gas specialists, with the mandate to acquire long life oil and gas assets including royalties, non operated working interests and unitized production for yield and capital appreciation. Toscana has grown since inception through the successful completion of a number of acquisitions and is currently producing an aggregate of approximately 1,425 Boe/d comprised of 40% oil and natural gas liquids and 60% natural gas. Toscana owns its oil and gas assets through its wholly-owned subsidiary Firenze Energy Ltd. ("Firenze").

Summary of Reserves Information Relating to Toscana

Sproule Associates Ltd. ("Sproule"), an independent reserves evaluator, prepared an evaluation of the proved and probable crude oil, natural gas liquids and natural gas reserves and the net present value of those reserves for the petroleum and natural gas interests of Firenze (other than Firenze's Carmangay property), a wholly-owned subsidiary of Toscana, effective as of December 31, 2011. In addition, McDaniel & Associates Consultants Ltd. ("McDaniel's"), an independent reserves evaluator, prepared an evaluation of the proved and probable crude oil, natural gas liquids and natural gas reserves and the net present value of those reserves for the petroleum and natural gas interests of Firenze's Carmangay property effective as of December 31, 2011. The reserve estimates and future net revenue forecasts were prepared by Sproule and McDaniel's respectively, in accordance with National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities.

The future net revenues and net present values presented below were calculated using forecast prices and costs based on the crude oil, natural gas and natural gas liquids prices as published in Sproule's December 31, 2011 price deck and as published in McDaniel's January 1, 2012 price deck respectively.

The following table summarizes Firenze's oil and gas reserves and the undiscounted value and the present value, discounted at 0%, 5%, 10%, 12% and 15% of Firenze's estimated future net revenue based on forecast price and cost assumptions as of December 31, 2011 pursuant to the Sproule report:

Table S-1A

Firenze Energy Ltd. Consolidation

Summary of the Evaluation of the P&NG Reserves

(As of Date: 2011-12-31)

| Remaining Reserves | Net Present Value Before Income Taxes | |||||||

| Company | ||||||||

| Gross | WI | RI | 0% | 5% | 10% | 15% | 20% | |

| 100% | Gross | Gross | M$ | M$ | M$ | M$ | M$ | |

| Oil (MBBL) | ||||||||

| Proved Developed Producing | 5494.8 | 2002.9 | 1789.0 | 104071 | 59275 | 41188 | 36818 | 31879 |

| Probable Developed Producing | 569.6 | 167.6 | 156.6 | 20069 | 7063 | 3555 | 2886 | 2216 |

| Probable Developed Non-Producing | 11.8 | 5.9 | 5.6 | 281 | 222 | 179 | 165 | 147 |

| Total Probable | 581.3 | 173.4 | 162.2 | 20350 | 7284 | 3734 | 3051 | 2363 |

| Total Proved + Probable | 6076.1 | 2176.3 | 1951.2 | 124421 | 66559 | 44922 | 39869 | 34242 |

| Solution Gas (MMCF) | ||||||||

| Proved Developed Producing | 2329 | 947 | 834 | 0 | 0 | 0 | 0 | 0 |

| Probable Developed Producing | 116 | 48 | 42 | 0 | 0 | 0 | 0 | 0 |

| Total Proved + Probable | 2445 | 995 | 876 | 0 | 0 | 0 | 0 | 0 |

| Non-Assoc, Assoc Gas (MMCF) | ||||||||

| Proved Developed Producing | 23790 | 8736 | 8157 | 20468 | 16077 | 13138 | 12227 | 11067 |

| Proved Developed Non-Producing | 382 | 77 | 73 | 211 | 174 | 146 | 137 | 125 |

| Proved Undeveloped | 623 | 311 | 293 | 111 | 48 | -4 | -23 | -48 |

| Total Proved | 24795 | 9124 | 8523 | 20790 | 16300 | 13280 | 12341 | 11143 |

| Probable Developed Producing | 8295 | 3209 | 2951 | 10142 | 6030 | 4021 | 3499 | 2894 |

| Probable Developed Non-Producing | 4954 | 1281 | 1105 | 3720 | 2469 | 1705 | 1485 | 1217 |

| Probable Undeveloped | 125 | 62 | 59 | 235 | 186 | 150 | 138 | 122 |

| Total Probable | 13373 | 4552 | 4115 | 14097 | 8685 | 5876 | 5121 | 4233 |

| Total Proved + Probable | 38168 | 13677 | 12638 | 34887 | 24984 | 19156 | 17463 | 15376 |

| NGLs (MBBL) | ||||||||

| Proved Developed Producing | 238.1 | 94.9 | 72.9 | 0 | 0 | 0 | 0 | 0 |

| Proved Developed Non-Producing | 18.4 | 1.2 | 0.9 | 0 | 0 | 0 | 0 | 0 |

| Total Proved | 256.5 | 96.1 | 73.8 | 0 | 0 | 0 | 0 | 0 |

| Probable Developed Producing | 23.7 | 9.8 | 7.2 | 0 | 0 | 0 | 0 | 0 |

| Probable Developed Non-Producing | 3.7 | 0.2 | 0.2 | 0 | 0 | 0 | 0 | 0 |

| Total Probable | 27.4 | 10.0 | 7.3 | 0 | 0 | 0 | 0 | 0 |

| Total Proved + Probable | 283.8 | 106.1 | 81.1 | 0 | 0 | 0 | 0 | 0 |

| Grand Total (Mboe) | ||||||||

| Proved Developed Producing | 10085.9 | 3711.6 | 3360.4 | 124539 | 75352 | 54326 | 49045 | 42945 |

| Proved Developed Non-Producing | 82.1 | 14.0 | 13.1 | 211 | 174 | 146 | 137 | 125 |

| Proved Undeveloped | 103.8 | 51.9 | 48.9 | 111 | 48 | -4 | -23 | -48 |

| Total Proved | 10271.8 | 3777.5 | 3422.4 | 124861 | 75574 | 54468 | 49159 | 43022 |

| Probable Developed Producing | 1995.2 | 720.2 | 662.7 | 30211 | 13092 | 7576 | 6385 | 5110 |

| Probable Developed Non-Producing | 841.1 | 219.7 | 189.9 | 4001 | 2690 | 1884 | 1650 | 1364 |

| Probable Undeveloped | 20.8 | 10.4 | 9.8 | 235 | 186 | 150 | 138 | 122 |

| Total Probable | 2857.0 | 950.2 | 862.4 | 34447 | 15969 | 9610 | 8172 | 6596 |

| Total Proved + Probable | 13128.8 | 4727.7 | 4284.8 | 159308 | 91543 | 64078 | 57331 | 49618 |

Solution gas revenue included in oil. NGL revenue included with oil and gas.

The following table summarizes Firenze's oil and gas reserves and the undiscounted value and the present value, discounted at 0%, 5%, 10%, 12% and 15% of Firenze's estimated future net revenue based on forecast price and cost assumptions as of December 31, 2011 pursuant to the McDaniel report:

| Firenze Energy Ltd. - Carmangay Property |

| Total Company Reserves and Net Present Value |

| Forecast Prices and Costs as of December 31, 2011 |

| Total Reserves |

| |

Company Share of Remaining Reserves (Mbbl, MMcf, Mlt) |

Company Share of Net Present Value Before Income Tax (M$) (5) |

||||||

| |

Gross (1) |

RI (2) | Net (3) | @ 0.0% |

@ 5.0% |

@ 10.0% |

@ 12.0% |

@ 15.0% |

| Proved Producing Reserves | ||||||||

| Light/Medium Oil | 372.0 | - | 322.0 | 20,814.90 | 17,410.10 | 14,967.30 | 14,178.90 | 13,150.10 |

| Natural Gas | 99.3 | - | 92.7 | 345.0 | 276.5 | 229.9 | 215.4 | 196.7 |

| Natural Gas Liquids | 2.0 | - | 1.2 | 107.9 | 90.1 | 77.7 | 73.7 | 68.5 |

| Total | 21,267.80 | 17,776.70 | 15,274.90 | 14,468.0 | 13,415.30 | |||

| Proved Non-Producing Reserves | ||||||||

| Light/Medium Oil | - | - | - | -179.3 | -118.5 | -80.1 | -68.9 | -55.3 |

| Total | -179.3 | -118.5 | -80.1 | -68.9 | -55.3 | |||

| Proved Undeveloped Reserves | ||||||||

| Light/Medium Oil | 312.6 | - | 272.4 | 13,957.10 | 10,844.60 | 8,560.60 | 7,818.80 | 6,851.0 |

| Natural Gas | 81.2 | - | 77.2 | 328.8 | 261.8 | 213.5 | 198.0 | 177.8 |

| Natural Gas Liquids | 1.6 | - | 1.1 | 96.7 | 79.6 | 67.0 | 62.8 | 57.3 |

| Total | 14,382.60 | 11,186.0 | 8,841.10 | 8,079.60 | 7,086.10 | |||

| Total Proved Reserves | ||||||||

| Light/Medium Oil | 684.6 | - | 594.4 | 34,592.60 | 28,136.30 | 23,447.80 | 21,928.80 | 19,945.80 |

| Natural Gas | 180.5 | - | 169.9 | 673.8 | 538.3 | 443.5 | 413.4 | 374.5 |

| Natural Gas Liquids | 3.6 | - | 2.4 | 204.6 | 169.7 | 144.6 | 136.5 | 125.9 |

| Total | 35,471.0 | 28,844.30 | 24,035.90 | 22,478.70 | 20,446.20 | |||

| Probable Producing Reserves | ||||||||

| Light/Medium Oil | 106.4 | - | 91.3 | 6,047.10 | 4,080.30 | 2,912.10 | 2,580.20 | 2,180.60 |

| Natural Gas | 29.1 | - | 27.2 | 132.4 | 87.5 | 61.8 | 54.6 | 46.0 |

| Natural Gas Liquids | 0.6 | - | 0.4 | 33.5 | 22.9 | 16.8 | 15.0 | 12.9 |

| Total | 6,213.0 | 4,190.70 | 2,990.70 | 2,649.80 | 2,239.50 | |||

| Probable Undeveloped Reserves | ||||||||

| Light/Medium Oil | 77.3 | - | 65.9 | 4,665.0 | 2,950.10 | 1,928.60 | 1,641.30 | 1,300.0 |

| Natural Gas | 20.8 | - | 19.7 | 110.0 | 67.7 | 43.5 | 36.8 | 28.9 |

| Natural Gas Liquids | 0.4 | - | 0.2 | 24.1 | 14.9 | 9.6 | 8.1 | 6.4 |

| Total | 4,799.10 | 3,032.70 | 1,981.70 | 1,686.20 | 1,335.30 | |||

| Total Probable Reserves | ||||||||

| Light/Medium Oil | 183.8 | - | 157.1 | 10,712.10 | 7,030.40 | 4,840.70 | 4,221.50 | 3,480.50 |

| Natural Gas | 49.9 | - | 46.9 | 242.3 | 155.2 | 105.2 | 91.4 | 74.9 |

| Natural Gas Liquids | 1.0 | - | 0.6 | 57.6 | 37.8 | 26.3 | 23.1 | 19.3 |

| Total | 11,012.0 | 7,223.40 | 4,972.20 | 4,336.0 | 3,574.70 | |||

| Proved & Probable Producing Reserves | ||||||||

| Light/Medium Oil | 478.5 | - | 413.3 | 26,862.0 | 21,490.40 | 17,879.40 | 16,759.10 | 15,330.60 |

| Natural Gas | 128.5 | - | 119.9 | 477.3 | 364.0 | 291.7 | 269.9 | 242.7 |

| Natural Gas Liquids | 2.6 | - | 1.6 | 141.4 | 113.1 | 94.4 | 88.7 | 81.4 |

| Total | 27,480.70 | 21,967.50 | 18,265.50 | 17,117.70 | 15,654.70 | |||

| Proved & Probable Non-Producing Reserves | ||||||||

| Light/Medium Oil | - | - | - | -179.3 | -118.5 | -80.1 | -68.9 | -55.3 |

| Total | -179.3 | -118.5 | -80.1 | -68.9 | -55.3 | |||

| Proved & Probable Undeveloped Reserves | ||||||||

| Light/Medium Oil | 389.9 | - | 338.2 | 18,622.10 | 13,794.70 | 10,489.20 | 9,460.10 | 8,151.0 |

| Natural Gas | 102.0 | - | 96.9 | 438.8 | 329.6 | 257.0 | 234.8 | 206.7 |

| Natural Gas Liquids | 2.0 | - | 1.4 | 120.8 | 94.5 | 76.6 | 70.9 | 63.8 |

| Total | 19,181.70 | 14,218.80 | 10,822.80 | 9,765.80 | 8,421.50 | |||

| Total Proved & Probable | ||||||||

| Reserves | ||||||||

| Light/Medium Oil | 868.4 | - | 751.5 | 45,304.70 | 35,166.70 | 28,288.50 | 26,150.30 | 23,426.30 |

| Natural Gas | 230.4 | - | 216.8 | 916.1 | 693.5 | 548.7 | 504.7 | 449.4 |

| Natural Gas Liquids | 4.6 | - | 3.0 | 262.2 | 207.6 | 171.0 | 159.6 | 145.2 |

| Total | 46,483.0 | 36,067.80 | 29,008.20 | 26,814.60 | 24,020.90 | |||

| Company Share of Remaining Reserves (MBOE) | Company Share of Net Present Value Before Income Tax ($/BOE) |

|||||||

| Gross (1) | RI (2) | Net (3) |

@ 0.0% | @ 5.0% | @ 10.0% | @ 12.0% | @ 15.0% | |

| BOE Reserves and NPV/BOE (4) | ||||||||

| Proved Producing | 390.6 | - | 338.7 | 54.45 | 45.51 | 39.11 | 37.04 | 34.35 |

| Proved Non-Producing | - | - | - | - | - | - | - | - |

| Proved Undeveloped | 327.7 | - | 286.3 | 43.89 | 34.13 | 26.98 | 24.66 | 21.62 |

| Firenze Energy Ltd. - Carmangay Property | ||||||||

| Total Company Reserves and Net Present Value | ||||||||

| Forecast Prices and Costs as of December 31, 2011 | ||||||||

| Total Reserves | ||||||||

| Company Share of Remaining Reserves (Mbbl, MMcf, Mlt) | Company Share of Net Present Value Before Income Tax (M$) (5) |

|||||||

Gross (1) |

RI (2) |

Net (3) |

@ 0.0% |

@ 5.0% |

@ 10.0% |

@ 12.0% |

@ 15.0% |

|

| Total Proved | 718.3 | - | 625.1 | 49.38 | 40.16 | 33.46 | 31.29 | 28.46 |

| Probable Producing | 111.9 | - | 96.2 | 55.52 | 37.45 | 26.73 | 23.68 | 20.01 |

| Probable Undeveloped | 81.2 | - | 69.4 | 59.10 | 37.35 | 24.41 | 20.77 | 16.44 |

| Total Probable | 193.1 | - | 165.6 | 57.03 | 37.41 | 25.75 | 22.45 | 18.51 |

| Proved & Probable Producing | 502.4 | - | 434.9 | 54.70 | 43.73 | 36.36 | 34.07 | 31.16 |

| Proved & Probable Non-Producing | - | - | - | - | - | - | - | - |

| Proved & Probable Undeveloped | 409.0 | - | 355.7 | 46.90 | 34.76 | 26.46 | 23.88 | 20.59 |

| Total Proved & Probable | 911.4 | - | 790.7 | 51.00 | 39.57 | 31.83 | 29.42 | 26.36 |

(1) Gross reserves are working interest reserves before royalty deductions.

(2) Royalty interest reserves.

(3) Net reserves include working interest after royalty deductions plus royalty interest reserves.

(4) Barrels of Oil Equivalent based on 6.0:1 for Natural Gas, 1.0:1 for Condensate and C5+, 1.0:1 for Ethane,1.0:1 for Propane, 1.0:1 for Butanes, 1.0:1 for NGL Mix. NPV/BOE based on Co. Share BOE reserves. BOE's may be misleading, particularly if used in isolation. A BOE conversion ratio of 6 Mcf:1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

(5) Costs associated with extraction of natural gas products have in most cases been deducted from the natural gas revenues.

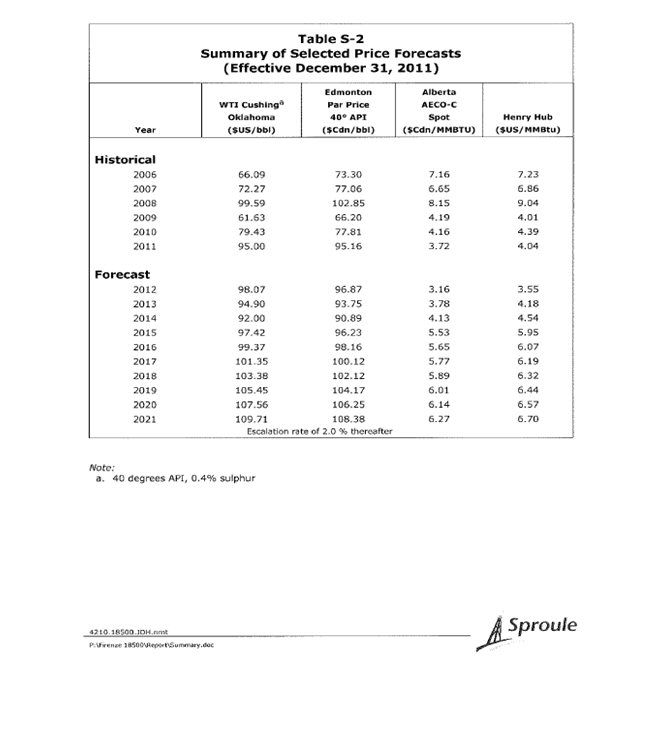

The following table sets out the forecast price assumptions used by Sproule as of December 31, 2011:

To view the table please visit the following link:

http://media3.marketwire.com/docs/425smrtables-2.jpg

{kind=link}

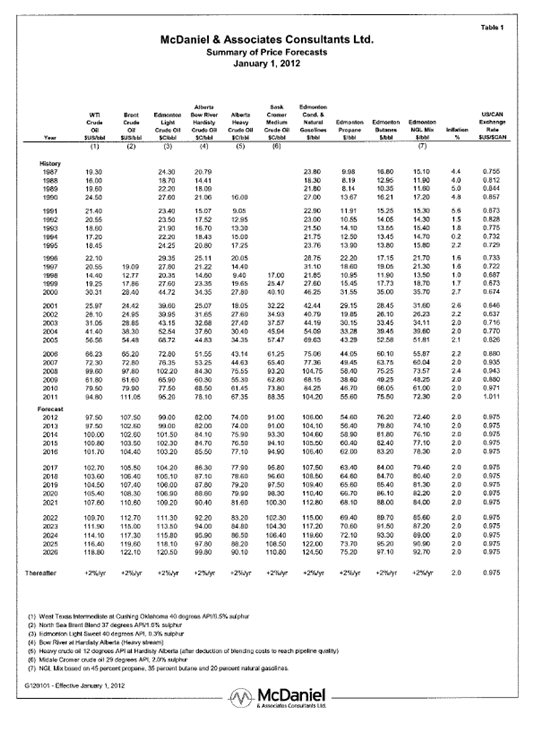

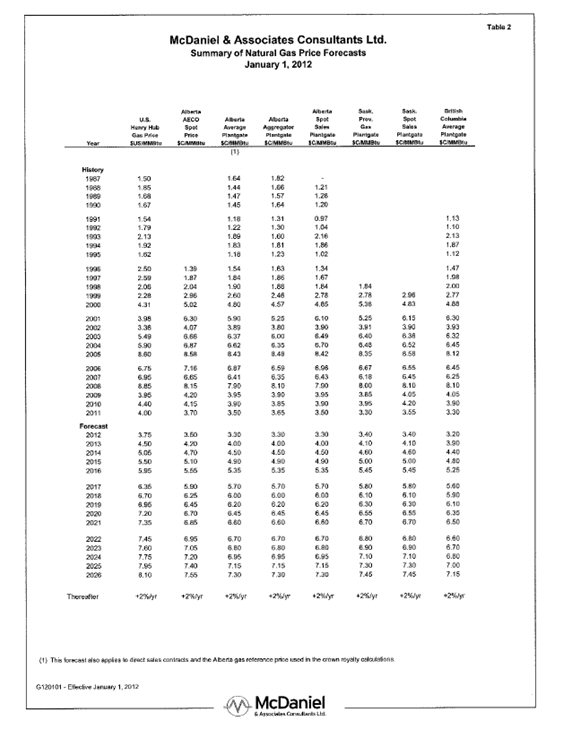

The following tables set out the forecast price assumptions and the forecast natural gas price assumptions respectively, used by McDaniel as of January 1, 2012:

To view the table please visit the following links:

http://media3.marketwire.com/docs/425smrmcdanieltable.jpg

{kind=link}

http://media3.marketwire.com/docs/425smrtable2.jpg

{kind=link}

Significant Conditions to Completion of the Proposed Transaction

Completion of the Proposed Transaction is subject to: various closing conditions which are usual and appropriate for an amalgamation; Exchange acceptance; and if applicable pursuant to Exchange requirements, majority of the minority shareholder approval. Where applicable, the Proposed Transaction cannot close until the required shareholder approval is obtained. There can be no assurance that the Proposed Transaction will be completed as proposed or at all.

Investors are cautioned that, except as disclosed in the management information circular or filing statement to be prepared in connection with the Proposed Transaction, any information released or received with respect to the Proposed Transaction may not be accurate or complete and should not be relied upon. Trading in the securities of a capital pool company should be considered highly speculative.

The Exchange has in no way passed upon the merits of the Proposed Transaction and has neither approved nor disapproved the contents of this news release.

Cautionary Note Regarding Forward-Looking Statements

This news release contains forward-looking statements relating to the Proposed Transaction, including statements regarding the exchange ratio for the Proposed Transaction, the sponsorship, the receipt of all necessary regulatory and shareholder approvals and satisfaction of all other closing conditions in connection with the Proposed Transaction and other statements that are not historical facts. Readers are cautioned not to place undue reliance on forward-looking statements, as there can be no assurance that the plans, intentions or expectations upon which they are based will occur. By their nature, forward-looking statements involve numerous assumptions, known and unknown risks and uncertainties, both general and specific, that contribute to the possibility that the predictions, forecasts, projections and other forward looking statements will not occur, which may cause actual performance and results in future periods to differ materially from any estimates or projections of future performance or results expressed or implied by such forward looking statements. These assumptions, risks and uncertainties include, among other things: that the necessary approvals and/or exemptions are not obtained or some other condition to the closing of the Proposed Transaction is not satisfied; the risk that closing of the Proposed Transaction could be delayed if Senmar and Toscana are not able to obtain the necessary approvals on the timelines planned; and the assumptions relating to the timing of obtaining required approvals and satisfying closing conditions for the Proposed Transaction, state of the economy in general and capital markets in particular, investor interest in the business and future prospects of Senmar and Toscana.

The forward-looking statements contained in this news release are made as of the date of this news release. Except as required by law, Senmar and Toscana disclaim any intention and assume no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by applicable securities law. Additionally, Senmar and Toscana undertake no obligation to comment on the expectations of, or statements made, by third parties in respect of the matters discussed above.

Additional Advisories

Boes are presented on the basis of one Boe for six Mcf of natural gas. Disclosure provided herein in respect of Boes may be misleading, particularly if used in isolation. A Boe conversion ratio of 6 Mcf:1 Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

Net present values do not necessarily represent the fair market value of the estimated reserves.

Neither the Exchange nor its Regulation Services Provider (as that term is defined in the policies of the Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Contact Information:

Steven Jmaeff

President and Chief Executive Officer

(403) 998-9770

info@senmarcapital.com

Toscana Resource Corporation

Joseph Durante

Chief Executive Officer

(403) 410-6793

jdurante@toscanacapital.com