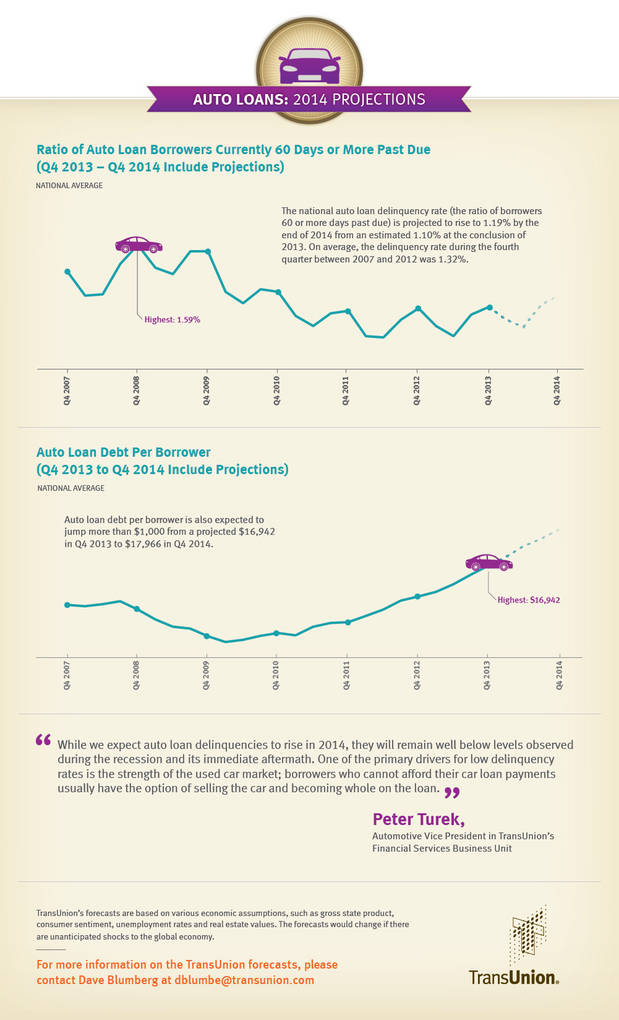

CHICAGO, IL--(Marketwired - Dec 17, 2013) - TransUnion's annual auto loan forecast calls for increases in both delinquency and debt levels during 2014. The national auto loan delinquency rate (the ratio of borrowers 60 or more days past due) is projected to rise to 1.19% by the end of 2014 from an estimated 1.10% at the conclusion of 2013. Auto loan debt per borrower is also expected to jump more than $1,000 from a projected $16,942 in Q4 2013 to $17,966 in Q4 2014.

"While we expect auto loan delinquencies to rise in 2014, they will remain well below levels observed during the recession and its immediate aftermath," said Peter Turek, automotive vice president in TransUnion's financial services business unit. "One of the primary drivers for low delinquency rates is the strength of the used car market; borrowers who cannot afford their car loan payments usually have the option of selling the car and becoming whole on the loan. The wide availability of this exit strategy has caused the overall volume of auto loan debt to rise faster than the delinquent volume of auto loans, which leads to a lower delinquency rate -- it's a denominator effect."

Since 2007, the auto loan delinquency rate has been as low as 0.86% in Q2 2012 and as high as 1.59% in Q4 2008. On average, the delinquency rate during the fourth quarter between 2007 and 2012 was 1.32%.

60-Day National Auto Loan Delinquency Rate (Q4 2013 and Q4 2014 include projections)

| Q4 2007 | Q4 2008 | Q4 2009 | Q4 2010 | Q4 2011 | Q4 2012 | Q4 2013 | Q4 2014 | |||||||

| 1.38% | 1.59% | 1.54% | 1.22% | 1.07% | 1.09% | 1.10% | 1.19% |

TransUnion data show that auto leasing may play a greater role in the industry during 2014. The number of leases issued since the recession ended in 2009 has steadily climbed. In the first six months of 2009, approximately 500,000 auto leases were issued. Three years later, this number doubled to one million leases for the first six months of 2012. This number increased further in 2013, with more than 1.3 million auto leases issued in the first six months of the year.

"We expect the number of leases to continue to rise as a percentage of all auto loans in 2014," said Turek. "This will likely help keep auto loan delinquencies low, as leases are generally issued to consumers with a higher VantageScore® credit score. Overall, the increased demand in both new and used vehicles has allowed dealers and lenders to match consumers with the right vehicles and loan terms."

Another contributing factor to lower delinquency levels is the fact that non-prime borrowers make up a smaller portion of all auto loans. Non-prime borrowers are identified as those with a VantageScore® credit score lower than 700 on a scale of 501-990. Even though the percentage of newly originated non-prime auto loans (33.18% in Q2 2013) has increased, the impact on the overall delinquency is minor.

In Q3 2013 (latest data available), non-prime borrowers made up 29.8% of all auto loans. This is significantly down from the Q3 high observed in 2008, when 34.6% of non-prime borrowers comprised all auto loans. In Q3 2013 there were more than 3 million fewer auto loans (down nearly 15%) in the non-prime borrower segment than there were in Q3 2008. As a comparison, the total auto loan population has only dropped about 1% in that same timeframe, or around 550,000 fewer auto loans.

Total Auto Loan Account Volume -- Percentage of Non-Prime Borrowers

| Q3 2007 | Q3 2008 | Q3 2009 | Q3 2010 | Q3 2011 | Q3 2012 | Q3 2013 | ||||||

| 33.2% | 34.6% | 34.1% | 32.2% | 30.2% | 30.0% | 29.8% |

"The data highlight the significance non-prime borrowers play in the overall delinquency rate," said Turek. "We have been tracking this segment of the population closely for some time, because once they take a bigger part of the overall auto loan pie, we expect upward pressure on delinquencies."

On a state level, auto loan delinquency rates are expected to rise in 34 states with the largest increases occurring in Maine (+7%), Connecticut (+6%), Indiana (+6%) and South Carolina (+5%). The biggest percentage declines are expected in Oregon (-8%), Alaska (-4%) and Utah (-4%). "The state data is especially encouraging as we don't expect any major delinquency rises," added Turek.

TransUnion projects auto loan debt to continue to rise, finishing 2014 with 15 straight quarterly increases. The projected $17,966 auto loan debt level in Q4 2014 would mark a 6.0% increase from the previous year, greater than those expected or observed in 2013 (+5.5%), 2012 (+4.8%), 2011 (+2.1%) and 2010 (+0.6%).

"Unless there is a real shock to the economy, we don't envision auto loan debt levels to drop for quite some time," said Turek. "This is good news for dealers, lenders and consumers, as higher demand for autos will lead to more auto loans, creating incentives for consumers as auto dealers and auto lenders compete for their business."

TransUnion's forecasts are based on various economic assumptions, such as gross state product, consumer sentiment, unemployment rates and real estate values. The forecasts would change if there are unanticipated shocks to the global economy.

60-Day Auto Loan Delinquency Historical Data and Projections for 2014

| 2012-2014 | Q4 2012 Q4 2013 | Q4 2014 | ||||

| USA | 1.09% | 1.10% | 1.19% |

Highest Auto Loan Delinquency States Q4 2014

| Mississippi | 2.25% | |

| Oklahoma | 1.95% | |

| Louisiana | 1.90% |

Lowest Auto Loan Delinquency States Q4 2014

| Oregon | 0.54% | |

| North Dakota | 0.55% | |

| Minnesota | 0.64% |

Note: Q4 2013 also is a projected number as the quarter has not yet ended.

TransUnion's Industry Insights Report

The data provided are gathered from TransUnion's proprietary Industry Insights Report (IIR), a quarterly overview summarizing data, trends and perspectives on the U.S. consumer lending industry. The report is based on anonymized credit data from virtually every credit-active consumer in the United States.

About TransUnion

As a global leader in information and risk management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering high quality data, and integrating advanced analytics and enhanced decision-making capabilities. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion reaches businesses and consumers in 33 countries around the world. www.transunion.com/business

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail

Telephone 312 972 6646