CHICAGO, IL--(Marketwire - February 16, 2011) - TransUnion's quarterly analysis of trends in the mortgage industry found that the national mortgage loan delinquency rate (the ratio of borrowers 60 or more days past due) decreased for the fourth consecutive quarter at the end of 2010, dropping to 6.41 percent.

This statistic, which is traditionally seen as a precursor to foreclosure, reflects a decrease of 0.47 percent from the third quarter of 2010 (6.44 percent), and is the smallest decline since the recession ended in the summer of 2009. Year over year, mortgage borrower delinquency is down approximately 7 percent (from 6.89 percent in the fourth quarter 2009).

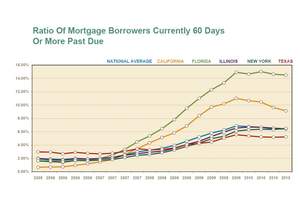

Q4 2010 Mortgage Statistics

- Mortgage borrower delinquency rates in the fourth quarter of 2010 continued to be highest in Nevada (14.76 percent) and Florida (14.50 percent), while the lowest mortgage delinquency rates continued to be found in North Dakota (1.72 percent), South Dakota (2.22 percent) and Alaska (2.73 percent).

- Unlike recent quarters, many states (33) showed increases in delinquency from the previous quarter, with North Dakota (+13.16 percent), Vermont (+10.87 percent) and the District of Columbia (+7.4 percent) experiencing the largest increases.

- Analysis of later-stage mortgage delinquency, such as the ratio of borrowers 90 or 120 or more days past due, suggest that a possible deceleration in foreclosure rates is underway.

- The average national mortgage debt per borrower again decreased (0.59 percent) to $189,046 from the previous quarter's $190,176. On a year-over-year basis, the fourth quarter 2010 average represents a 2.4 percent decrease over the fourth quarter 2009 average mortgage debt per borrower level of $193,690.

- The area with the highest average mortgage debt per borrower continued to be the District of Columbia at $368,138 followed by California at $339,088 and Hawaii at $313,838. The lowest average mortgage debt per borrower remained in West Virginia at $99,554.

- Quarter over quarter, Alabama showed the greatest percentage increase in mortgage debt per borrower (+1.40 percent), followed by New York (+1.39 percent) and Hawaii (+1.39 percent). Areas showing the largest percentage drop in average mortgage debt were Nevada (-2.82 percent), Florida (-1.71 percent) and Arizona (-1.63 percent).

- For the first time in 2010 on a quarterly year-over-year national basis, mortgage originations increased (+43.3 percent). The increase occurred across all states, with the largest increase in year-over-year originations seen in Alaska (130.8 percent) and Massachusetts (89.8 percent). The smallest increase was observed in Nevada (5.42 percent).

- Just as mortgage delinquency trends differ between the national and state economies, metropolitan areas also showed different movements in the fourth quarter of this year. In TransUnion's Q3 2010 news release we reported about 65 percent of the MSAs showing improvement in their delinquency rates over the prior quarter. The percentage of MSAs experiencing a decline in their mortgage delinquency rates has dropped to 44 percent.

Analysis and Supporting Quotes

"The current deceleration in falling mortgage delinquency rates is indeed concerning. Although the increase in January's consumer confidence index is good news for the consumer as well as the fourth quarter GDP number of 3.2 percent, real estate prices as reflected by the Case Schiller Home Price Index have been consistently falling since the end of second quarter. What we hoped was a temporary third quarter price adjustment due to the ending of the home buyer tax credit appears now to be more systemic.

"Although a variety of other factors besides house prices, such as household income and interest rates, impact the real estate market, real estate values are perhaps the most important as they have reflected a negative correlation with mortgage delinquency of more than 80 percent since the recession began at the end of 2007. Coupled with the current amount of foreclosures on the market and the historic lows associated with TransUnion's Real Estate Inquiry Index, the news may be best for home buyers who are looking for real estate bargains as prices continue to drop."

-- Tim Martin, group vice president of the U.S. Housing Market in TransUnion's financial services business unit

The trends in real estate inquiries are captured in TransUnion's 90-day Real Estate Inquiry Index*. As of the fourth quarter, the Real Estate Inquiry Index for the nation stood at 24.95 -- the lowest value since the index was benchmarked in 2000. On a year-over-year basis, the Index is down 19.25 percent compared to the fourth quarter of 2009.

Mortgage Delinquency Forecast and Supporting Quotes

"The real estate market does have some good news to offer. The National Association of Realtors recently announced that single family home sales in December marked the fifth increase in the last six months. However, with the large volume of distressed homes still on the market, TransUnion believes that if the home prices for existing residential real estate continue to slide, mortgage delinquency rates may start to tick upwards. Our econometric models, although correctly predicting mortgage delinquencies this quarter, have now been updated using a less optimistic assumption about future house prices.

"These models now suggest that the 60-day mortgage delinquency rate will likely be flat or edge up next quarter, but then begin to drift lower by year end. Note that this forecast is based on various economic assumptions such as gross state product, disposable income, unemployment rates, and particularly real estate values -- which we think will continue to fall but begin to level off by the end of 2011. This forecast would change if there are unanticipated shocks to the economy affecting the recovery in the housing market."

-- Tim Martin, group vice president of the U.S. Housing Market in TransUnion's financial services business unit

*TransUnion's Real Estate Index compares the number of credit reports requested of TransUnion for a real estate transaction (mortgage, refinance or HELOC) during a specific quarter.

Supporting Resources/Links

TransUnion Trend Data Interactive U.S. Map

TransUnion 3Q Mortgage Statistics

ARM Crisis and Why It's Not Over

TransUnion Payment Hierarchy Study

TransUnion Value of Loyalty/Delinquency Study

TransUnion on Twitter

TransUnion's Trend Data database

The report is part of an ongoing series of quarterly consumer lending sector analyses focusing on credit card, auto loan and mortgage data available on TransUnion's Web site. Information for this analysis is culled from TransUnion's Trend Data and the anonymous credit files of approximately 10 percent of credit-active U.S. consumers, providing a real-life perspective on how they are managing their credit health.

TransUnion's Trend Data, a one-of-a-kind database consisting of 27 million anonymous consumer records randomly sampled every quarter from TransUnion's national consumer credit database. Each record contains more than 200 credit variables that illustrate consumer credit usage and performance. Since 1992, TransUnion has been aggregating this information at the county, Metropolitan Statistical Area (MSA), state and national levels. For the purpose of this analysis, the term "credit card" refers to those issued by banks.

About TransUnion

As a global leader in credit and information management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering comprehensive data and advanced analytics and decisioning. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion employs associates in more than 25 countries on five continents. www.transunion.com/business

Contact Information:

Contact

Clifton ONeal

TransUnion

312 972 6646