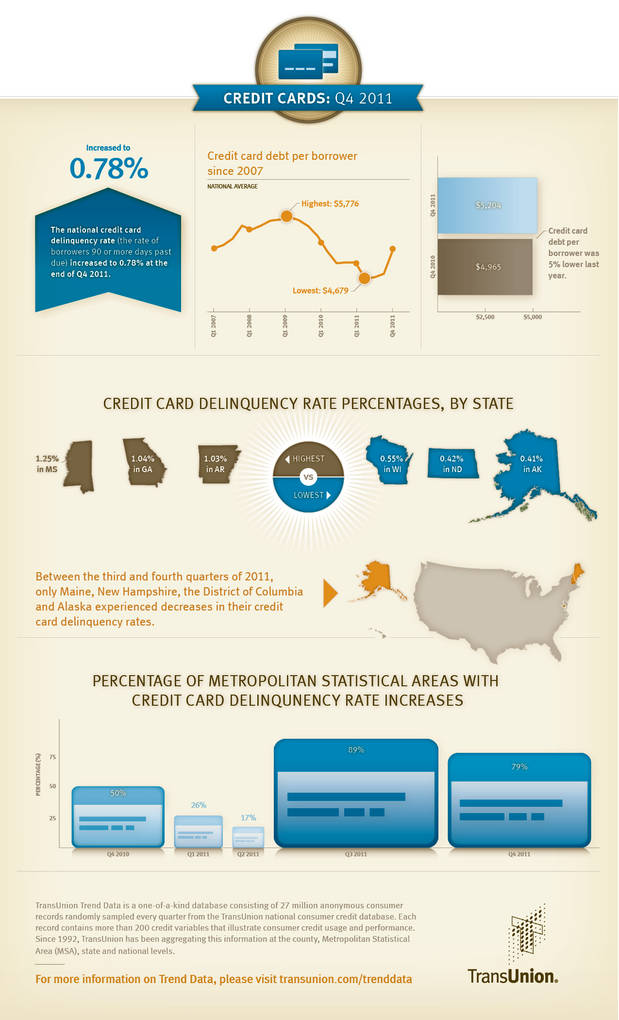

CHICAGO, IL--(Marketwire - Feb 22, 2012) - The national credit card delinquency rate (the ratio of borrowers 90 or more days past due) reached 0.78% in the fourth quarter of 2011, a drop of almost 5% from the same period one year ago and continuing well below historical norms. Average credit card debt per borrower increased $239 from the same period last year to $5,204, though it too remains near record-low levels. For the quarter, credit card delinquencies and debt both experienced seasonal increases. This information is reported by TransUnion and is part of its ongoing series of quarterly analyses of credit-active U.S. consumers, evaluating how they are managing credit related to mortgages, credit cards and auto loans.

"2011 closed out with the lowest year-end card delinquency rate nationwide since 1995," said Ezra Becker, vice president of research and consulting in TransUnion's financial services business unit. "This is the net result of riskier loans having worked their way through the system, cautious risk management strategies on the part of lenders and consumers working to maintain the health and good status of their card relationships."

Total card originations in 2011 grew by more than 14% relative to 2010. Moreover, in 2010 only 21.8% of new card accounts went to consumers with a VantageScore® lower than 700 (on a scale of 501 - 990); In 2011, that number had risen to 25.2%. So not only are more non-prime consumers gaining access to card credits, they also comprise a larger percentage of the cards entering the market. "We have seen a shift toward non-prime borrowers beginning in the second half of 2010 and continuing through the fourth quarter of 2011, which makes the current low delinquency rates even more remarkable," added Becker. "This shift is driven in part by the fierce competition among lenders for prime borrowers, as well as the effects of ongoing consumer deleveraging efforts in the prime credit range. As a result, many lenders have put more of a focus on originating cards in the non-prime market."

On a quarter-over-quarter basis, delinquency rates have risen slightly from the all-time low reached in Q2 2011. This is driven mostly by seasonality. "We are still well below historical delinquency norms for credit cards, indicating that consumers are still effectively managing this debt and their relationship with the credit card providers."

Credit card delinquencies rose 9.9% from 0.71% in Q3 2011 to 0.78% in Q4 2011 while average credit card debt per borrower increased $442 from $4,762 to $5,204 in that same timeframe.

Between the third and fourth quarters of 2011, only Maine, New Hampshire, the District of Columbia, and Alaska experienced decreases in their credit card delinquency rates, and two states remained unchanged. On a more granular level, 79% of metropolitan statistical areas (MSAs) saw increases in their respective credit card delinquency rates in Q4 2011. This was down compared to last quarter, when 89% of MSAs experienced an increase.

Based on revised economic assumptions, TransUnion forecasts that credit card borrower delinquency rates could continue to drift upward in the short term, but then begin to gradually drop towards the end of the year. This forecast is based on seasonality effects and various other economic factors such as anticipated gross state product, consumer sentiment, disposable income, and employment conditions. The forecast changes as the economy deviates from a conservative economic forecast, or if there are unanticipated shocks to the economy affecting recovery.

Q4 2011 Credit Card Statistics - Delinquency Rates

| Quarter over Quarter | Q3 2011 | Q4 2011 | Pct. Change |

| USA | 0.71% | 0.78% | 9.86% |

| Year over year | Q4 2010 | Q4 2011 | Pct. Change |

| USA | 0.82% | 0.78% | (4.88%) |

| Highest Credit Card Delinquency States | Q4 2011 |

| Mississippi | 1.25% |

| Georgia | 1.04% |

| Arkansas | 1.03% |

| Alabama | 1.02% |

| Lowest Credit Card Delinquency States | Q4 2011 |

| Alaska | 0.41% |

| North Dakota | 0.42% |

| Wisconsin | 0.55% |

| South Dakota | 0.55% |

| Top 3 Year-over-Year Declines | Q4 2010 | Q4 2011 | Pct. Change |

| Alaska | 0.54% | 0.41% | (24.07%) |

| Nevada | 1.27% | 1.01% | (20.47%) |

| Utah | 0.74% | 0.59% | (20.27%) |

Q4 2011 Credit Card Statistics - Credit Card Debt Per Borrower

| Quarter over Quarter | Q3 2011 | Q4 2011 | Pct. Change |

| USA | $4,762.00 | $5,204.00 | 9.27% |

| Year over Year | Q4 2010 | Q4 2011 | Pct. Change |

| USA | $4,965.00 | $5,204.00 | 4.80% |

| Highest Credit Card Debt States | Q4 2011 |

| Alaska | $7,024 |

| Colorado | $6,110 |

| Connecticut | $5,822 |

| North Carolina | $5,814 |

| Lowest Credit Card Debt States | Q4 2011 |

| Iowa | $4,120 |

| North Dakota | $4,340 |

| South Dakota | $4,422 |

| West Virginia | $4,455 |

| Top Year-over-Year Increase | Q4 2010 | Q4 2011 | Pct. Change |

| Vermont | $4,337 | $4,910 | 13.19% |

| Top 3 Year-over-Year Declines | Q4 2010 | Q4 2011 | Pct. Change |

| Tennessee | $5,605 | $4,965 | (11.43%) |

| Mississippi | $5,201 | $4,842 | (6.92%) |

| Hawaii | $5,573 | $5,414 | (2.86%) |

Supporting Resources/Links

TransUnion Trend Data Interactive U.S. Map

TransUnion 3Q11 Credit card Statistics

TransUnion Payment Hierarchy Study

TransUnion Deleveraging Analysis

TransUnion on Twitter

TransUnion's Trend Data database

TransUnion's Trend Data is a one-of-a-kind database consisting of 27 million anonymous consumer records randomly sampled every quarter from TransUnion's national consumer credit database. Each record contains more than 200 credit variables that illustrate consumer credit usage and performance. Since 1992, TransUnion has been aggregating this information at the county, Metropolitan Statistical Area (MSA), state and national levels. For the purpose of this analysis, the term "credit card" refers to those issued by banks.

About TransUnion

As a global leader in information and risk management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering high quality data, and integrating advanced analytics and enhanced decision-making capabilities. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion reaches businesses and consumers in 25 countries around the world. For more information, visit www.transunion.com.

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail

Telephone 312 972 6646