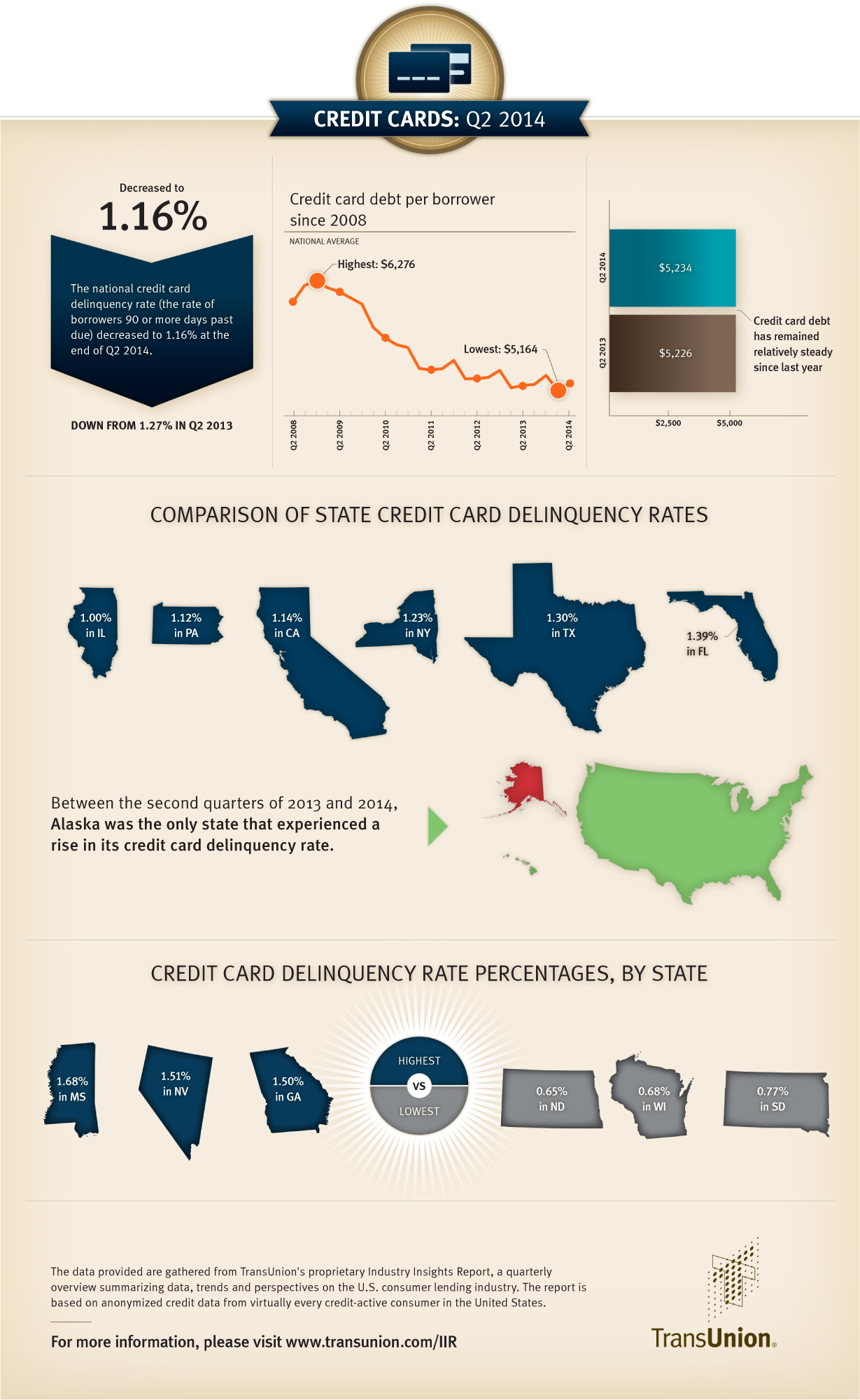

CHICAGO, IL--(Marketwired - Aug 26, 2014) - The national credit card delinquency rate declined to its lowest level in at least seven years, dropping from 1.27% in Q2 2013 to 1.16% in Q2 2014. The latest TransUnion Industry Insights Report found that the credit card delinquency rate (the ratio of borrowers 90 days or more delinquent on their general purpose credit cards) dropped nearly 9% in the last year while falling more than 15% in the last quarter (from 1.37% in Q1 2014).

Average credit card debt per borrower remained almost unchanged in the last year, increasing slightly from $5,226 in Q2 2013 to $5,234 in Q2 2014. On a quarterly basis, credit card debt increased from $5,164 in Q1 2014.

The data provided are gathered from TransUnion's proprietary Industry Insights Report, a quarterly overview summarizing data, trends and perspectives on the U.S. consumer lending industry. The report is based on anonymized credit data from virtually every credit-active consumer in the United States."

"Consumers continue to have a good handle on their credit cards, with delinquencies at all-time lows across the spectrum," said Ezra Becker, vice president of research and consulting in TransUnion's financial services business unit. "We observed that delinquency rates are dropping for all age groups, and at relatively similar rates."

90+ Day Credit Card Delinquency Rates for Various Age Groups

| Age Range | Q2 2013 | Q2 2014 | PCT. Change |

| Under 30 | 1.76% | 1.63% | -7.35% |

| 30-39 | 1.74% | 1.56% | -10.31% |

| 40-49 | 1.63% | 1.48% | -8.85% |

| 50-59 | 1.20% | 1.11% | -7.74% |

| 60+ | 0.72% | 0.68% | -4.74% |

While delinquency rates dropped for all age groups, the credit card balance picture was more complex. The two oldest age groups -- ages 50-59 and those 60 or older -- saw a material increase in their credit card balances. All other age groups experienced relatively small declines in balances.

"Traditionally, consumers carry heavier debt loads between the ages of 40 and 60 as they are in their peak purchasing years," said Becker. "They also tend to spend more on items such as new cars, home furnishings, college tuition for their children, etc. As we've noted in recent quarters, younger consumers continue to have lower debt levels -- which can be attributed in part to limited access to card credit and a greater reliance on debit cards, among other factors."

Average Credit Card Balances for Various Age Groups

| Age Range | Q2 2013 | Q2 2014 | PCT. Change |

| Under 30 | $2,135 | $2,135 | -0.01% |

| 30-39 | $4,871 | $4,816 | -1.14% |

| 40-49 | $6,724 | $6,713 | -0.16% |

| 50-59 | $6,765 | $6,805 | 0.60% |

| 60+ | $4,802 | $4,891 | 1.86% |

Only one state -- Alaska -- experienced an increase in its credit card delinquency rate between Q2 2013 and Q2 2014. The largest percentage delinquency declines occurred in Massachusetts, Wisconsin, Arizona and Illinois. Of the largest cities in the U.S., Boston (-18.19%), San Francisco (-17.98%) and Chicago (-14.05%) saw the biggest declines in credit card delinquency rates.

Credit card debt per borrower decreased in only 13 states on a yearly basis. However, several major cities experienced declines, including: Phoenix (-2.59% from $5,347 in Q2 2013 to $5,277 in Q2 2014), Miami (-1.31% from $5,347 in Q2 2013 to $5,277 in Q2 2014) and San Francisco (-1.11% from $5,568 in Q2 2013 to $5,506 in Q2 2014).

TransUnion reported 349.79 million credit card accounts as of Q2 2014, up from 332.26 million in Q2 2013. Viewed one quarter in arrears (to ensure all accounts are included in the data), new account originations increased 17.75% to 11.73 million in Q1 2014, up from 9.96 million in Q1 2013.

TransUnion's latest credit card report also found that the non-prime population (those consumers with a VantageScore® 2.0 credit score lower than 700) represents a larger portion of all new credit card loans at 31.2% in Q1 2014, up from 27.3% in the same period last year. In Q1 2007, the non-prime population represented 40.1% of all credit card originations for that quarter.

"Credit cards continue to perform well even with a higher percentage of non-prime consumers entering the market," said Toni Guitart, director of research and consulting in TransUnion's financial services business unit. "We also noted an increase in credit card limits, which points to lenders feeling they can take on more risk while giving consumers a bigger credit cushion."

This information is reported by TransUnion and is part of its ongoing series of quarterly analyses of credit-active U.S. consumers and how they are managing credit related to mortgages, credit cards and auto loans. To subscribe to TransUnion news releases, please click here.

Q2 2014 Credit Card Statistics - Consumer-Level Delinquency Rates

| Quarter over Quarter | Q1 2014 | Q2 2014 | Pct. Change |

| USA | 1.37% | 1.16% | (8.7%) |

| Year over Year | Q2 2013 | Q2 2014 | Pct. Change |

| USA | 1.27% | 1.16% | (15.3%) |

| Credit Card Consumer Delinquency Rates for Select States | Q2 2014 |

| California | 1.14% |

| Florida | 1.39% |

| Illinois | 1.00% |

| New York | 1.23% |

| Texas | 1.30% |

| Largest Year-over-Year Declines | Q2 2013 | Q2 2014 | Pct. Change |

| Massachusetts | 1.26% | 1.03% | (18.3%) |

| Wisconsin | 0.80% | 0.68% | (15.0%) |

| Arizona | 1.44% | 1.23% | (14.6%) |

| Largest Year-over-Year Increases | Q2 2013 | Q2 2014 | Pct. Change |

| Alaska | 1.13% | 1.19% | 5.3% |

Q2 2014 Credit Card Statistics - Credit Card Debt Per Borrower

| Quarter over Quarter | Q1 2014 | Q2 2014 | Pct. Change |

| USA | $5,164 | $5,234 | 1.4% |

| Year over Year | Q2 2013 | Q2 2014 | Pct. Change |

| USA | $5,226 | $5,234 | 0.2% |

| Credit Card Debt per Borrower for Select States | Q2 2014 |

| California | $5,293 |

| Florida | $5,229 |

| Illinois | $5,284 |

| New York | $5,396 |

| Texas | $5,465 |

| Largest Year-over-Year Declines | Q2 2013 | Q2 2014 | Pct. Change |

| Arizona | $5,349 | $5,241 | (2.0%) |

| Colorado | $5,718 | $5,643 | (1.3%) |

| Alaska | $6,851 | $6,765 | (1.3%) |

| Largest Year-over-Year Increases | Q2 2013 | Q2 2014 | Pct. Change |

| Vermont | $4,850 | $4,937 | 1.8% |

| West Virginia | $4,589 | $4,667 | 1.7% |

| Virginia | $5,866 | $5,964 | 1.7% |

About TransUnion

As a global leader in credit and information management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering comprehensive data and advanced analytics and decisioning. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion reaches businesses and consumers in 33 countries around the world on five continents. www.transunion.com/business

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail

Telephone (312) 985 3059