EAU CLAIRE, WI--(Marketwire - Jan 29, 2013) - Citizens Community Bancorp, Inc. (

Highlights

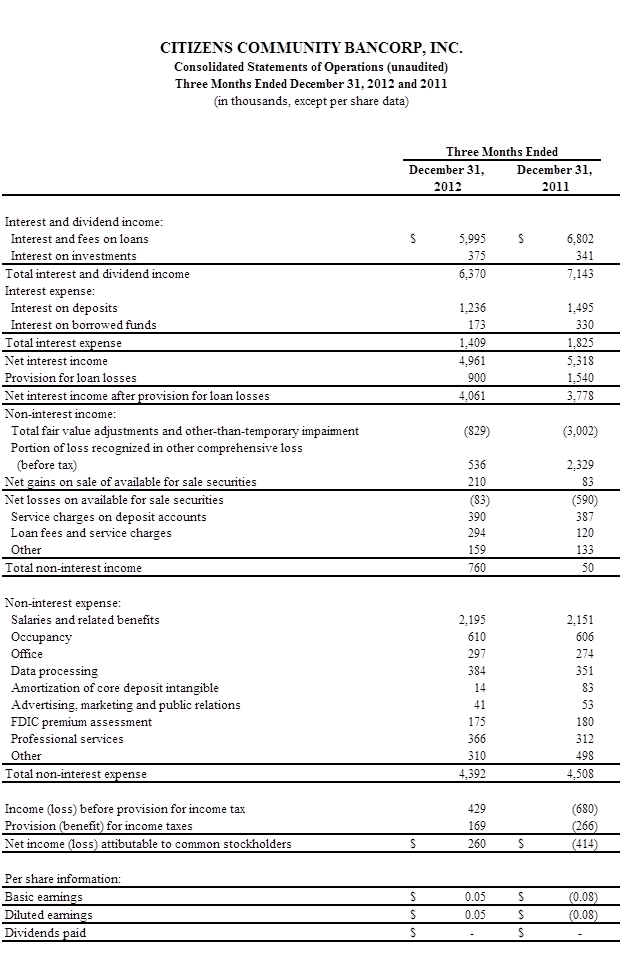

- Net income during the fiscal first quarter of 2013 was $260,000 or $0.05 per diluted share, compared with a net loss of $(414,000) or $(0.08) per diluted share during the fiscal first quarter of 2012. Company management believes the increase in net income during the quarter ended December 31, 2012 over the same period in the prior year reflects significant asset quality improvement for the Bank.

- The Company's provision for loan losses was $900,000 during the fiscal quarter ended December 31, 2012, compared with $1.54 million during the prior year's fiscal first quarter, which contributed to the Company's growth in its net interest income after provision for loan losses to $4.06 million during the fiscal first quarter of 2013, compared with net interest income after provision for loan losses of $3.78 million during the same period of fiscal 2012.

- Income from loan fees and service charges increased to $294,000 during the fiscal first quarter of 2013, compared with $120,000 during the fiscal first quarter of 2012. The primary driver of loan fee income growth between the periods was the sale of mortgage loans to the secondary market, a capability the Company added in March 2012.

- Total non-performing assets (NPAs) were $6.16 million at December 31, 2012, compared with $5.05 million at December 31, 2011, reflecting the Company's continued efforts in improving its balance sheet and removing problem loans from the loan portfolio.

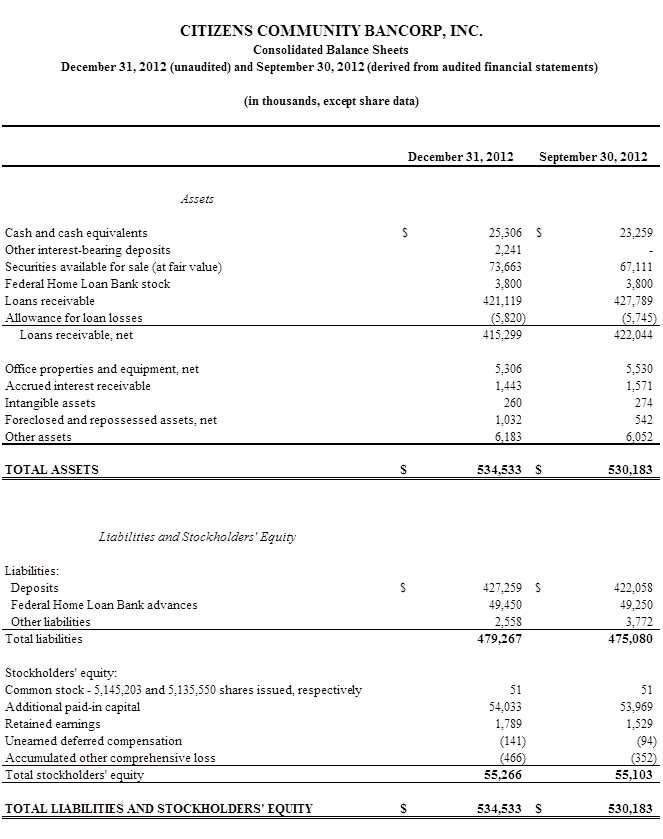

- The Company grew total assets to $534.53 million at December 31, 2012 from $530.18 million at September 30, 2012 and $530.81 million at December 31, 2011.

- The Company's tier 1 capital to adjusted total assets ratio was 10.0% at December 31, 2012, compared with 10.1% at December 31, 2011. The Company's total capital to risk weighted assets ratio was 15.6% at December 31, 2012, compared with 14.9% at December 31, 2011.

"The first three months of the year demonstrated the continuing progress we have made to execute a strategic plan that includes improving asset quality, reducing loan delinquencies and managing interest and noninterest expense," said Edward H. Schaefer, President and CEO. "This translated to positive earnings performance during the first quarter of fiscal 2013. In fact, our net income for this recently completed quarter exceeded our total net income in all of fiscal 2012.

"We have more work ahead to move problem loans to final resolution, as evidenced by fluctuations in non-performing loans and owned real estate levels during the past several quarters. We are encouraged that downward adjustments to loan and asset values have slowed, giving us a level of confidence that we will see fewer adjustments and charge-offs in the coming months and quarters.

"Loans 30 to 90 days past due have trended down significantly year-over-year, which we believe is a positive sign that fewer loans are at risk of moving toward non-accrual or non-performing status in the future. We believe our improved credit and underwriting policies are supporting improved lending decisions, which we believe will result in improved loan quality going forward. Throughout this difficult but necessary process, Citizens' has maintained capital levels that exceed regulatory standards for a well-capitalized bank, positioning the bank to pursue lending opportunities and make investments to support new business."

Income Statement and Balance Sheet Overview

The Company reported total interest and dividend income of $6.37 million during the quarter ended December 31, 2012, compared with $7.14 million during the quarter ended December 31, 2011. This decrease was largely due to the decrease in the average balance of outstanding higher rate loans between the periods. Interest expense declined to $1.41 million during the fiscal first quarter of 2013, compared with $1.83 million during the fiscal first quarter of 2012. This decrease in interest expense from the prior year primarily reflected lower levels of higher-rate money market accounts and certificates of deposit, which the Company allowed to run off because of the current low interest rate environment as well as a reduction in interest on borrowed funds.

Net interest income before provision for loan losses was $4.96 million during the first quarter of 2013, compared with $5.32 million during the fiscal first quarter of 2012, reflecting the decline in interest income noted above, which was partially offset by our interest expense reduction during the current year.

Non-interest income increased to $760,000 during the quarter ended December 31, 2012, compared with $50,000 during the same period of the prior fiscal year, primarily as a result of the following factors: a reduction in other than temporary losses from non-agency mortgage-backed securities in the amount of $380,000 over the comparable prior year period; a $210,000 gain on sale of available for sale securities during the fiscal first quarter of 2013, compared to $83,000 during the same period of the prior year; and an increase in revenue from loan fees and service charges of $177,000 during the current quarter as compared to the same period in the prior year.

Total non-interest expense was $4.39 million during the quarter ended December 31, 2012, compared with $4.51 million during the quarter ended December 31, 2011, reflecting the Company's continued focus on expense control throughout the year. Net interest margin was 3.76% and the Bank's net interest spread was 3.65% at December 31, 2012, compared with net interest margin of 4.04% and interest rate spread of 3.91% at December 31, 2011, reflecting continuing pressure on margins in an extended low-interest rate environment.

The Company reported net loans receivable of $415.30 million at December 31, 2012, compared with $425.15 million at December 31, 2011 and $422.04 million at September 30, 2012. Schaefer explained the Company has continued to add new loans, particularly first mortgages and refinancings, which have been offset by problem loans being moved off the Company's balance sheet.

"We have experienced success in loan originations, some of which we have retained and others of which we have sold to the secondary market," he said. "We have trimmed our loan portfolio year-over-year, and as we continue to pursue quality lending opportunities, we anticipate once again seeing growth in our loan portfolio."

The Company's allowance for loan losses was $5.82 million at December 31, 2012, compared with $5.54 million at December 31, 2011 and $5.75 million at September 30, 2012. Non-accruing loans were $5.13 million at December 31, 2012, compared with $4.24 million at December 31, 2011 and $4.51 million at September 30, 2012. The increase in non-accruing loans as of the most recent quarter end primarily reflected regulatory changes in interpretation of bankrupt loans, so a number of loans that were not classified historically as non-accruing loans were reclassified during the quarter ended December 31, 2012 as non-accruing.

Loans 30 to 90 days past due were $5.98 million as of December 31, 2012, compared with $8.57 million as of December 31, 2011. As a ratio to total loans, past due loans declined to 2.19% as of the end of the fiscal first quarter of 2013 from 2.98% as of the end of the fiscal first quarter of 2012.

"We believe the long-term trends in non-accruing and past due loans are an encouraging indication that we can look forward to improved loan quality throughout our loan portfolio in coming quarters," explained Schaefer. "We are also encouraged by the gains we have made in improving our coverage ratios and holding the line on the allowance for loan losses to total loans at 1.38% as of December 31, 2012 compared to 1.34% at our 2012 fiscal year end." The ratio of non-performing assets to total assets was 1.15% at December 31, 2012, 0.95% at September 30, 2012, and 0.99% at December 31, 2011.

Total deposits were $427.26 million as of December 31, 2012, compared with $444.13 million as of December 31, 2011, and $422.06 million at 2012 fiscal year end. The year-over-year decline in total deposits partially reflects a reduction in higher-rate money market accounts and certificates of deposit, which the Company allowed to run off due to the current low interest rate environment. New certificates of deposit, money market and demand deposit accounts contributed to the total deposit increase between September 30, 2012 and December 31, 2012.

At December 31, 2012, the bank's total capital to risk weighted assets was 15.6%, tier 1 capital to risk weighted assets was 14.4% and tier 1 capital to adjusted total assets was 10.0%. All ratios exceeded regulatory standards for a well-capitalized institution. Tangible book value per share was $10.36 per common share as of December 31, 2012.

Schaefer concluded: "We believe we are emerging from a challenging period as a leaner, stronger, well capitalized bank with opportunities to grow revenue and build shareholder value. We appreciate the loyalty our shareholders have demonstrated in supporting the Company, and the dedication our employees have shown in helping the bank tackle difficult problems while staying focused on serving customers and adding new business. We anticipate continued progress and look forward to communicating our progress to all stakeholders."

About the Company

Citizens Community Federal, a wholly owned subsidiary of Citizens Community Bancorp, Inc., is a full-service bank based in Eau Claire, Wisconsin, serving more than 50,000 customers in Wisconsin, Minnesota and Michigan through 25 branch locations, including 17 locations in Walmart Supercenters. The Company's stock trades on the NASDAQ Global Market under the symbol "CZWI."

Cautionary Statement Regarding Forward-Looking Statements

Certain statements contained in this news release are considered "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words or phrases such as "anticipate," "believe," "could," "expect," "intend," "may," "planned," "potential," "should," "will," "would" or the negative of those terms or other words of similar meaning. Such forward-looking statements in this news release are inherently subject to many uncertainties arising in the Company's operations and business environment. These uncertainties include general economic conditions, in particular, relating to consumer demand for the Bank's products and services; the Bank's ability to maintain current deposit and loan levels at current interest rates; competitive and technological developments; deteriorating credit quality, including changes in the interest rate environment reducing interest margins; prepayment speeds, loan origination and sale volumes, charge-offs and loan loss provisions; the Bank's ability to maintain required capital levels and adequate sources of funding and liquidity; maintaining capital requirements may limit the Bank's operations and potential growth; changes and trends in capital markets; competitive pressures among depository institutions; effects of critical accounting estimates and judgments; changes in accounting policies or procedures as may be required by the Financial Accounting Standards Board (FASB) or other regulatory agencies overseeing the Bank; further write-downs in the Bank's mortgage-backed securities portfolio; the Bank's ability to implement its cost-savings and revenue enhancement initiatives; legislative or regulatory changes or actions or significant litigation adversely affecting the Bank; fluctuation of the Company's stock price; the Bank's ability to attract and retain key personnel; the Bank's ability to secure confidential information through the use of computer systems and telecommunications networks; and the impact of reputational risk created by these developments on such matters as business generation and retention, funding and liquidity. Shareholders, potential investors and other readers are urged to consider these factors carefully in evaluating the forward-looking statements and are cautioned not to place undue reliance on such forward-looking statements. Such uncertainties and other risks that may affect the Company's performance are discussed further in Part I, Item 1A, "Risk Factors," in the Company's Form 10-K, for the year ended September 30, 2012 filed with the Securities and Exchange Commission on December 10, 2012. The Company undertakes no obligation to make any revisions to the forward-looking statements contained in this news release or to update them to reflect events or circumstances occurring after the date of this report.

Contact Information:

Contact:

Mark Oldenberg

CFO

715-836-9994