CALGARY, ALBERTA--(Marketwire - Sept. 7, 2011) - Viterra Inc. (TSX:VT) (ASX:VTA) ("Viterra") today announced an increase in its third quarter financial results over the same period last year, reflecting strong contributions from its agri-products operations and continued solid performances from its grain handling and processing operations. Favourable weather across the Canadian Prairies resulted in good growing conditions for this year's crop and, when combined with healthy commodity prices, these factors motivated growers to invest in agri-products.

For the three months ended July 31, 2011, EBITDA increased 28% to $252 million compared to $197 million in the same quarter last year. On a year-to-date basis, EBITDA was up 56% to $591 million. All three business segments posted earnings improvements over the same period last year. Agri-products' year-to-date results have increased 55% on strong fertilizer volumes and pricing; Grain Handling and Marketing's EBITDA is up 49% due to record receivals and shipments in Australia as well as strong results from North American and International Grain; and Processing's earnings have risen 37% reflecting the new pasta and oat businesses acquired in the latter half of fiscal 2010.

Financial Highlights

(in thousands - except per share items) Three Months

ended July 31, Better

2011 2010 (Worse)

----------------------------------------------------------------------------

Sales and other operating revenues $ 3,554,061 $ 2,493,119 $ 1,060,942

Gross profit and net revenues from

services 485,691 392,667 93,024

EBITDA (1) 251,884 196,614 55,270

Net earnings 123,249 63,538 59,711

Earnings per share $ 0.33 $ 0.17 $ 0.16

Cash flow provided by operations (1) 147,857 162,221 (14,364)

Per share $ 0.40 $ 0.44 $ (0.04)

Free Cash Flow (1) 94,851 130,186 (35,335)

----------------------------------------------------------------------------

Financial Highlights

(in thousands - except per share items) Nine Months

ended July 31, Better

2011 2010 (Worse)

----------------------------------------------------------------------------

Sales and other operating revenues $ 8,726,458 $ 6,304,588 $ 2,421,870

Gross profit and net revenues from

services 1,221,634 938,656 282,978

EBITDA (1) 591,328 379,625 211,703

Net earnings 255,947 92,601 163,346

Earnings per share $ 0.69 $ 0.25 $ 0.44

Cash flow provided by operations (1) 426,947 273,229 153,718

Per share $ 1.15 $ 0.74 $ 0.41

Free Cash Flow (1) 291,689 188,867 102,822

----------------------------------------------------------------------------

(1) See Non-GAAP Measures in Section 11.0 of the attached Management's

Discussion and Analysis.

Net earnings for the quarter almost doubled, increasing to $123 million or $0.33 per share compared to $64 million or $0.17 per share generated in the same period last year. For the nine months ended July 31, 2011, net earnings have increased 176% to $256 million or $0.69 per share versus the $93 million or $0.25 per share in the same period last year.

Cash flow provided by operations for the quarter was $148 million and lower than the same quarter last year due to higher current income taxes and timing differences. On a year-to-date basis, cash flow provided from operations increased by 56% to $427 million reflecting higher EBITDA and lower cash financing costs offset in part by higher current taxes.

Mayo Schmidt, Viterra's President and Chief Executive Officer, commented, "Viterra has consistently delivered strong financial results for the first nine months of this fiscal year, far exceeding our earnings last year. Operationally, we also continue to perform well and in South Australia Viterra recently set a new record for grain shipped through our ports. We continue to strengthen our operational performance around the globe, which is generating higher returns for our shareholders. Looking forward, there is a lot of opportunity for Viterra with a promising harvest in both Western Canada and South Australia, and strong market fundamentals supporting our agri-business. To capitalize on these opportunities and drive value through our integrated worldwide pipeline, Viterra implemented a new global operating model around our three business lines of grain, agri-products and processing. This new model will strengthen and support our strategic vision now and into the future as Viterra continues to provide key agricultural ingredients to a growing world."

Consolidated sales and other operating revenues for the quarter increased 43% to $3.6 billion compared to $2.5 billion in the third quarter of fiscal 2010. For the nine months ended July 31, 2011, revenues increased 38% to $8.7 billion, compared to $6.3 billion in the same period of fiscal 2010. The sales improvement for both the third quarter and first nine months of fiscal 2011 was the result of increased revenues in all three business segments. Grain Handling and Marketing's revenues increased due to higher commodity prices, a more established International Grain group and higher Australian receivals and shipments following a record crop in South Australia. Agri-products' revenues increased as a result of robust fertilizer contributions and Processing's revenues increased due to solid contributions from the pasta and oat processing businesses, which were purchased in the latter half of fiscal 2010.

Segment EBITDA(1) Contributions by Geography

(in thousands) Three Months

ended July 31, 2011

---------------------------------------------

Grain

Handling and Agri-

Marketing Products Processing Total % Contribution (2)

----------------------------------------------------------------------------

North America $ 54,258 $158,579 $ 24,144 $ 236,981 80%

Australia 40,904 3,323 5,010 49,237 17%

International 9,075 - (102) 8,973 3%

-------------------------------------------- ------------------

Segment

EBITDA (1) $104,237 $161,902 $ 29,052 $ 295,191 100%

-------------------------------------------- ------------------

----------------------------------------------------------------------------

Segment EBITDA(1) Contributions by Geography

(in thousands) Nine Months

ended July 31, 2011

----------------------------------------------------------

Grain

Handling and Agri-

Marketing Products Processing Total % Contribution (2)

----------------------------------------------------------------------------

North America $162,854 $181,008 $ 71,648 $ 415,510 58%

Australia 220,728 11,162 21,618 253,508 36%

International 40,499 - (382) 40,117 6%

-------------------------------------------- ------------------

Segment

EBITDA (1) $424,081 $192,170 $ 92,884 $ 709,135 100%

-------------------------------------------- ------------------

----------------------------------------------------------------------------

(1) See Non-GAAP Measures in Section 11.0 of the attached Management's

Discussion and Analysis.

(2) Percentage Contribution based on Segment EBITDA, prior to Corporate

Expenses.

The Grain Handling and Marketing segment generated $104 million in EBITDA for the quarter compared to $101 million in the third quarter of last year. On a year-to-date basis, this segment's EBITDA was $424 million compared to $284 million a year earlier. The majority of the increase relates to Viterra's Australian operations that contributed $220.7 million (2010 - $129.0 million) for the first nine months of the fiscal year due to record receivals, shipments and additional storage and handling revenues. The remaining increase is attributable to strong results from the North American team and from the International Grain group which has generated year-to-date EBITDA of $41 million, after a solid third quarter contribution of $9 million. The year-to-date consolidated pipeline margin was $36.33 per tonne compared to $29.52 per tonne last year. In North America, margins benefited from increased merchandising and blending opportunities, additional pulse sales and increased earnings throughout the terminal operations. In South Australia, margins increased due to high volumes, increased storage and handling fees, solid blending contributions and lower costs. Viterra has implemented a number of initiatives throughout the region that have not only lowered its costs per tonne but have resulted in sustainable cost reductions throughout the operation.

In Viterra's Agri-products segment, EBITDA increased over 50% in the third quarter to $162 million compared to $106 million in the corresponding period a year earlier. These positive results were driven by robust fertilizer contributions and timing differences as a result of the late seeding in North America that moved earnings from the second quarter into the third quarter. Fertilizer contributions were robust as market fundamentals continue to support strong demand and pricing. High commodity prices and increased nutrient requirements caused by excess moisture in 2010 and 2011, continue to encourage farmers to maximize their fertilizer applications. As a result, North American fertilizer sales volumes increased 26% for the quarter. Australian sales volumes were also up 20% during the quarter and the Company's consolidated fertilizer gross margin improved to $143.92 per tonne versus $118.56 per tonne a year earlier. Strong third quarter results increased year-to-date EBITDA 55% to $192 million compared to $124 million in fiscal 2010.

The Processing segment's EBITDA was $29 million for the third quarter compared to $22 million in the same period last year. The increase was due to the new oat processing business purchased in the fourth quarter of last year and stronger pasta margins. Viterra's North American food processing contributed $23 million (2010 - $17 million), while the Company's Australian malt and global feed operations contributed $6 million and $1 million, respectively. On a year-to-date basis, the segment's EBITDA was $93 million, compared to $68 million a year earlier. Year over year, the new pasta and oat processing businesses added $35 million while the Company experienced weaker results from canola processing and feed operations due to short-term challenges in both of these industries. Year to date, the Company's Australian malt operations have contributed $23 million to EBITDA, which is on par with the previous year.

New Crop Update

Across the Canadian Prairies, harvest is well underway and higher than average yields are expected from this year's crop due to favourable weather for much of the growing season. In its August 24, 2011 field crop reporting series release, Statistics Canada is predicting that western Canadian production of the six major grains will be 47.5 million tonnes, with an additional 2.5 million tonnes of lentils and other crops. This would represent an increase of 5.6% from the 45.0 million tonnes produced in the 2010 harvest, but a decrease from the 5-year historical average production of about 50.0 million tonnes. The quality of the crop in Western Canada looks promising, however, it is dependent on favourable harvest weather for the next couple of months.

In South Australia seeding finished in late June and good growing conditions exist throughout the majority of the state. The Australian Bureau of Agriculture and Resources Economics and Sciences ("ABARES") is predicting that the current crop will produce 7.6 million tonnes. This represents a 21% increase from the 10-year average for the state, but a decrease from the record 9.8 million tonnes produced last harvest. Based on current growing conditions, the Company believes there may be upside to ABARES's estimate. Crop quality in the state is good at this time. Approximately 80% of the crop is currently expected to be wheat and barley. Viterra's harvest preparations are well underway to ensure growers can deliver their grain in a timely and efficient manner during the next harvest.

Outlook

Grain Handling and Marketing

Viterra remains optimistic that the industry will see relatively strong volumes through the remaining portion of the fiscal year and into fiscal 2012, particularly if weather conditions are favourable into the fall. Strong demand and robust prices are expected to motivate farmers to actively market their grains through the next crop year. The Canadian Wheat Board ("CWB") is forecasting an export target of 18.0 million tonnes of wheat and barley out of Canada for the upcoming crop year compared to 15.8 million tonnes for the 2011 crop year.

The Company has increased its estimate for fiscal 2011 Canadian Grain Commission ("CGC") receipts for the six major grains in Western Canada to approximately 32.0 to 33.0 million tonnes, from its previous range of 31.0 to 32.0 million tonnes. As expected, producers have drawn down on-farm carryout stocks. For fiscal 2012, assuming production estimates hold, Viterra anticipates CGC receipts to be in the 30.0 to 32.0 million tonne range, which compares to the 32.0 million tonnes that is typically available.

For Viterra's South Australia grain handling operations, the Company expects shipments to remain strong into the last quarter of the fiscal year given the significant quantity of grain previously received into the system, the favourable commodity price environment and strong global demand. To complement the 8.5 million tonnes received into the Company's system during the first nine months of fiscal 2011, there were approximately 1.2 million tonnes of carry-in stocks from fiscal 2010. The Company currently estimates carry-over stocks into fiscal year 2012 for the Company's Australian system to range between 1.7 and 2.0 million tonnes, up from last year due to the record crop produced in the state.

The Company expects the global pipeline margin for fiscal 2011 to be at the high end of its guidance range of $33 to $36 per tonne.

From a regulatory perspective, the majority Conservative Government in Canada announced in May that it intends to provide western Canadian producers with marketing choice for wheat, durum and barley, which will eliminate the CWB's monopoly control as of August 2012. The federal government has created an industry working group to address transitional items and a report is expected in the fourth quarter. It is still early in the process and Viterra will await further details on how this new market will function before quantifying the benefits to the Company's operations. Viterra is supportive of the Government's direction and committed to working with the Government, industry, and the CWB, to ensure the Canadian grain industry remains a vibrant and competitive source for agricultural products.

In Australia, Viterra is in the process of renewing its accreditation from Wheat Exports Australia and has revised its access undertaking in response to feedback from the Australian Competition and Consumer Commission. The current accreditation and undertaking both expire on September 30, 2011 and renewals are required so that Viterra can continue to export bulk wheat out of Australia and operate its port terminals. Viterra remains confident that it will obtain these renewals by September 30, 2011, which will be effective from October 1, 2011 to September 30, 2014.

Agri-products

Looking to the remainder of the fiscal year, assuming good fall weather across the Prairies, demand for crop inputs in Western Canada is expected to remain favorable as producers undertake post harvest application work due to the following:

- strong commodity prices and market fundamentals that increase return prospects for farmers; and

- strong fertilizer demand as growers replenish soil nutrients following excess moisture this spring.

In Western Canada, fertilizer pricing remains high relative to historic levels. Given high commodity prices and significant nutrient requirements, the Company expects continued strong fundamentals for fertilizer pricing. For fiscal 2011, the Company expects its fertilizer margin to range between $110 to $130 per tonne, an increase from the previous guidance of $100 to $120 per tonne.

Processing

The Company remains focused on its diversification strategy to grow its portfolio of food and feed ingredients businesses. Looking forward, the Company expects similar contributions from the Processing segment during the last quarter of fiscal 2011 and into 2012 relative to prior periods as there are no significant near-term changes expected to the underlying fundamentals that support this business segment.

Strong demand for whole grain, nutritional food ingredients and healthy, economical pasta products, is expected to support continued solid results from the oat and pasta processing businesses.

Canola crush capacity in Western Canada has increased approximately 70% over the past 24 months and outpaced increasing demand. While this has resulted in short-term challenges, the Company believes the long-term outlook for canola processing is positive given ongoing demand for healthy oils.

Global malt markets remain challenged in the near term due to sluggish beer sales in North America and Europe causing excess capacity and margin pressure around the globe. For Viterra's malt operations in Australia, the Company believes that margins will remain compressed, below pre-recession levels, into the first half of fiscal 2012. However, the Company remains confident in the long-term outlook for this industry.

The Company expects the combined annual food processing margin for fiscal 2011 to range between $100 and $120 per tonne, an increase from its previous guidance of $90 to $110 per tonne.

Challenges in feed products are expected to continue due to excess capacity causing intense competition and margin pressure. The Company continues to take steps to mitigate the effects of these issues.

Third Quarter and Year-to-Date Segment Highlights

The following table provides various key financial highlights for the three and nine months ended July 31, 2011 compared to July 31, 2010. The Company's unaudited Consolidated Financial Statements and accompanying Management's Discussion & Analysis ("MD&A") for the three and nine months ended July 31, 2011 are incorporated fully into this news release. Readers are encouraged to review the following pages for a full description of the Company's current financial performance. Viterra will be hosting a conference call for interested parties on September 7, 2011 at 1:15 p.m. ET (11:15 a.m. MT) to discuss its third quarter and year-to-date financial results. Details are available on Viterra's website, under "Newsroom" at www.viterra.com.

----------------------------------------------------------------------------

Third Quarter Segment Highlights

(in thousands - except margins) Three Months

ended July 31, Better

2011 2010 (Worse)

----------------------------------------------------------------------------

Grain Handling and Marketing

Segment

Gross profit and net revenues

from services $ 207,213 $ 181,748 $ 25,465

EBITDA (1) 104,237 100,853 3,384

Sales and other operating

revenues 2,186,810 1,469,073 717,737

Operating Highlights (tonnes) :

North American Shipments 4,156 4,382 (226)

Australian Receivals 20 6 14

Total pipeline 4,176 4,388 (212)

Consolidated pipeline margin (per N/A N/A N/A

tonne)

Agri-products Segment

Gross profit and net revenue from

services $ 229,184 $ 167,754 $ 61,430

EBITDA (1) 161,902 105,750 56,152

Sales and other operating

revenues 1,134,746 817,887 316,859

Fertilizer 535,503 342,914 192,589

Crop Protection 317,664 296,978 20,686

Seed 120,321 82,306 38,015

Wool 115,352 58,462 56,890

Equipment sales and other revenue 39,753 31,575 8,178

Financial Products 6,153 5,652 501

Fertilizer volume (tonnes) 876 699 177

Fertilizer margin (per tonne

sold) $ 143.92 $ 118.56 $ 25.36

Processing Segment

Gross profit and net revenue from

services $ 49,294 $ 43,165 $ 6,129

EBITDA (1) 29,052 21,943 7,109

Sales and other operating

revenues 387,683 329,791 57,892

Processing sales volumes (tonnes)

Malt (2) 131 140 (9)

Pasta 54 55 (1)

Oats 90 55 35

Canola 38 61 (23)

Combined food processing margin

(per tonne sold) $ 120.77 $ 83.45 $ 37.32

Feed sales volumes (tonnes)

North America 419 443 (24)

New Zealand 29 33 (4)

Combined feed processing margin

(per tonne sold) $ 25.66 $ 36.16 $ (10.50)

Corporate Expenses

EBITDA (1) $ (43,307) $ (31,932) $ (11,375)

----------------------------------------------------------------------------

Third Quarter Segment Highlights

(in thousands - except margins) Nine Months

ended July 31, Better

2011 2010 (Worse)

----------------------------------------------------------------------------

Grain Handling and Marketing

Segment

Gross profit and net revenues

from services $ 719,826 $ 537,211 $ 182,615

EBITDA (1) 424,081 284,121 139,960

Sales and other operating

revenues 6,174,685 4,230,374 1,944,311

Operating Highlights (tonnes) :

North American Shipments 11,282 11,993 (711)

Australian Receivals 8,529 6,206 2,323

Total pipeline 19,811 18,199 1,612

Consolidated pipeline margin (per

tonne) $ 36.33 $ 29.52 $ 6.82

Agri-products Segment

Gross profit and net revenue from

services $ 349,304 $ 277,329 $ 71,975

EBITDA (1) 192,170 123,806 68,364

Sales and other operating

revenues 1,861,058 1,471,475 389,583

Fertilizer 864,892 627,629 237,263

Crop Protection 340,686 338,787 1,899

Seed 233,064 205,934 27,130

Wool 339,821 215,929 123,892

Equipment sales and other revenue 68,363 65,596 2,767

Financial Products 14,232 17,600 (3,368)

Fertilizer volume (tonnes) 1,528 1,380 148

Fertilizer margin (per tonne

sold) $ 126.46 $ 93.97 $ 32.49

Processing Segment

Gross profit and net revenue from

services $ 152,504 $ 124,116 $ 28,388

EBITDA (1) 92,884 67,836 25,048

Sales and other operating

revenues 1,136,208 927,866 208,342

Processing sales volumes (tonnes)

Malt (2) 376 403 (27)

Pasta 164 55 109

Oats 284 163 121

Canola 118 180 (62)

Combined food processing margin

(per tonne sold) $ 122.70 $ 88.79 $ 33.91

Feed sales volumes (tonnes)

North America 1,305 1,494 (189)

New Zealand 104 100 4

Combined feed processing margin

(per tonne sold) $ 26.20 $ 33.24 $ (7.04)

Corporate Expenses

EBITDA (1) $ (117,807) $ (96,138) $ (21,669)

----------------------------------------------------------------------------

(1) See Non-GAAP Measures in Section 11.0 of the attached Management's

Discussion and Analysis

(2) Includes contributions from Viterra's 42% ownership interest in Prairie

Malt and its wholly owned Australian malt business

Forward-Looking Statements

Certain statements in this news release are forward-looking statements that reflect Viterra's expectations regarding future results of operations, financial condition and achievements and are subject to important risks and uncertainties. The words "anticipate", "expect", "believe", "may", "should", "estimate", "project", "outlook", "forecast" or other similar words are used to identify such forward-looking information. Forward-looking statements in this document are intended to provide Viterra security holders and potential investors with information regarding Viterra and its subsidiaries, including Management's assessment of Viterra's and its subsidiaries' future financial and operational plans and outlook. All statements included or incorporated by reference in this news release that address activities, events or developments that Viterra or its Management expects or anticipates will or may occur in the future, including such things as growth of its business and operations, competitive strengths, strategic initiatives, planned capital expenditures, plans and references to future operations and results, critical accounting estimates and expectations regarding future capital resources and liquidity of Viterra and other such matters, are forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the actual results, performance and achievements of Viterra to be materially different from any future results, performance and achievements expressed or implied by those forward-looking statements. The risks include, but are not limited to, those factors discussed in Viterra's MD&A for the year ended October 31, 2010 under the heading "Risks and Risk Management". This MD&A can be found on Viterra's website at www.viterra.com as well as on SEDAR at www.sedar.com under Viterra Inc.

About Viterra

Viterra provides premium quality ingredients to leading global food manufacturers. Headquartered in Canada, the global agri-business has extensive operations across Canada, the United States, Australia, and New Zealand. Our growing international presence also extends to offices in Japan, Singapore, China, Vietnam, Switzerland, Italy, Ukraine, Germany and India. Driven by an entrepreneurial spirit, we operate in three distinct businesses: grain handling and marketing, agri-products, and processing. Viterra's expertise, close relationships with producers, and superior logistical assets allow the Company to consistently meet the needs of the most discerning end-use customers, helping to fulfill the nutritional needs of people around the world.

VITERRA

MANAGEMENT'S DISCUSSION AND ANALYSIS

JULY 31, 2011

1.0 Responsibility for Disclosure

Management's Discussion and Analysis ("MD&A") was prepared based on information available to Viterra Inc. (referred to herein as "Viterra" or the "Company") as of September 6, 2011. Management prepared this report to help readers interpret Viterra's unaudited Consolidated Financial Statements for the three months and nine months ended July 31, 2011.

Please read this report in conjunction with the audited Consolidated Financial Statements and MD&A contained in the Company's Annual Financial Review for the year ended October 31, 2010, which is available on Viterra's website at www.viterra.com, as well as on SEDAR at www.sedar.com, under Viterra Inc.

This MD&A and the unaudited Consolidated Financial Statements for the three months and nine months ended July 31, 2011 have been prepared in accordance with Canadian Generally Accepted Accounting Principles ("GAAP") and are presented in Canadian dollars unless specifically stated to the contrary.

2.0 Company Overview

Viterra is a vertically integrated global agri-business headquartered in Canada. The Company was founded in 1924 and has extensive operations across Canada and Australia, with facilities in the United States ("U.S.") and New Zealand. Viterra has offices in Canada, the U.S., Australia, New Zealand, Japan, Singapore, China, Vietnam, Switzerland, Italy, Ukraine, Germany and India.

As a major participant in the value-added agri-food supply chain, the Company operates in three interrelated segments: Grain Handling and Marketing, Agri-products, and Processing. Geographically, Viterra's operations are diversified across Canada, Australia, New Zealand and throughout the U.S. Viterra wholly owns pasta production, malt production, oat milling, canola processing and livestock feed manufacturing operations. Viterra's North American operations also participate in malt production through a 42% ownership interest in Prairie Malt Limited ("Prairie Malt") and in fertilizer manufacturing through its 34% ownership in Canadian Fertilizers Limited ("CFL").

Viterra is involved in other commodity-related businesses through strategic alliances and supply agreements with domestic and international grain traders and food processing companies. The Company markets commodities directly to customers in more than 50 countries around the world.

On May 5, 2010, Viterra completed the acquisition of Dakota Growers Pasta Company, Inc. ("Dakota Growers"), a U.S.-based durum miller and leading producer and marketer of dry pasta products in North America. Dakota Growers' financial contributions are included in Viterra's results as of May 5, 2010.

On August 17, 2010, Viterra completed the acquisition of 21C Holdings, L.P. ("21st Century") a premier U.S.-based processor of oats, wheat and custom-coated grains. Contributions from this business are included in Viterra's results as of August 17, 2010.

Viterra's shares trade on the Toronto Stock Exchange ("TSX") under the symbol "VT" and its CHESS Depositary Interests trade on the Australian Securities Exchange ("ASX") under the symbol "VTA".

3.0 Summary and Analysis of Consolidated Results

Selected Consolidated Financial Information

(in thousands - except per share

amounts) Three Months

ended July 31, Better

2011 2010 (Worse)

----------------------------------------------------------------------------

Sales and other operating revenues $ 3,554,061 $ 2,493,119 $ 1,060,942

----------------------------------------------------------------------------

Gross profit and net revenues from

services $ 485,691 $ 392,667 $ 93,024

Operating, general and

administrative expenses (233,807) (196,053) (37,754)

----------------------------------------------------------------------------

EBITDA (1) 251,884 196,614 55,270

Amortization (50,671) (63,706) 13,035

----------------------------------------------------------------------------

EBIT (1) 201,213 132,908 68,305

Integration expenses (1,167) (1,059) (108)

Gain on disposal of assets 169 241 (72)

Acquisition derivative - 2,208 (2,208)

Financing expenses (28,802) (44,851) 16,049

----------------------------------------------------------------------------

171,413 89,447 81,966

Recovery of (provision for)

corporate taxes

Current (78,258) (577) (77,681)

Future 30,094 (25,332) 55,426

----------------------------------------------------------------------------

Net earnings $ 123,249 $ 63,538 $ 59,711

----------------------------------------------------------------------------

----------------------------------------------------------------------------

Earnings per share $ 0.33 $ 0.17 $ 0.16

----------------------------------------------------------------------------

Selected Consolidated Financial

Information

(in thousands - except per share

amounts) Nine Months

ended July 31, Better

2011 2010 (Worse)

----------------------------------------------------------------------------

Sales and other operating revenues $ 8,726,458 $ 6,304,588 $ 2,421,870

Gross profit and net revenues from

services $ 1,221,634 $ 938,656 $ 282,978

Operating, general and

administrative expenses (630,306) (559,031) (71,275)

----------------------------------------------------------------------------

EBITDA (1) 591,328 379,625 211,703

Amortization (149,670) (137,909) (11,761)

EBIT (1) 441,658 241,716 199,942

Integration expenses (2,468) (4,233) 1,765

Gain on disposal of assets 743 616 127

Acquisition derivative - (866) 866

Financing expenses (86,637) (112,437) 25,800

----------------------------------------------------------------------------

353,296 124,796 228,500

Recovery of (provision for)

corporate taxes

Current (82,446) (11,974) (70,472)

Future (14,903) (20,221) 5,318

----------------------------------------------------------------------------

Net earnings $ 255,947 $ 92,601 $ 163,346

----------------------------------------------------------------------------

----------------------------------------------------------------------------

Earnings per share $ 0.69 $ 0.25 $ 0.44

----------------------------------------------------------------------------

(1) See Non-GAAP Measures in Section 11.0

Consolidated sales and other operating revenues ("sales" or "revenues") for the third quarter of fiscal 2011 increased 43% to $3.6 billion compared to $2.5 billion in the third quarter of fiscal 2010. For the first nine months ended July 31, 2011, revenues increased 38% to $8.7 billion, compared to $6.3 billion in the same period of fiscal 2010. The sales improvement for both the third quarter and first nine months of fiscal 2011 was the result of increased revenues in all three business segments. Grain handling and marketing revenues increased due to higher commodity prices, a more established International Grain group and higher Australian receivals and shipments following a record crop in South Australia. Agri-products revenues increased as a result of robust fertilizer contributions and processing revenues increased due to solid contributions from the pasta and oat processing businesses, which were purchased in the third and fourth quarters of fiscal 2010, respectively.

Quarterly gross profit and net revenues from services ("gross profit") increased 24% to $485.7 million compared to $392.7 million in the same quarter last year due to a continued strong shipping program for the Australian operations and higher results from the agri-products operations. Improved commodity prices, increased nutrient requirements, and favourable seeding conditions throughout much of the Canadian Prairies, supported robust fertilizer demand and pricing into the third quarter, and more than offset the effects of unseeded acres in Western Canada. These factors, along with contributions from the pasta and oat operations acquired in the latter half of fiscal 2010, increased year-to-date gross profit 30% to $1,221.6 million versus $938.7 million in the comparable period of fiscal 2010.

Operating, general and administrative ("OG&A") expenses were $233.8 million in the third quarter compared to $196.1 million in the comparable period of fiscal 2010. For the first nine months of fiscal 2011, OG&A expenses were $630.3 million, compared to $559.0 million in fiscal 2010. The increases primarily reflect the additional seasonal labour required by Viterra's Australian operations to handle the record harvest earlier in the fiscal year, a full complement of costs for the International Grain group, which was not fully established by this time last year, new costs related to the pasta and oat businesses acquired last fiscal year and higher accruals for incentive and transformational programs.

In both the third quarter and first nine months of fiscal 2011, EBITDA (see Non-GAAP Measures in Section 11.0) contributions from all business segments increased relative to the prior year. EBITDA increased 28% to $251.9 million in the third quarter compared to the same period a year earlier while on a year-to-date basis, EBITDA increased 56% to $591.3 million compared to $379.6 million in the corresponding period of the previous fiscal year. Agri-products' EBITDA increased 55% on strong fertilizer volumes and pricing; Grain Handling and Marketing's year-to-date results increased 49% due to record receivals and shipments in Australia and strong results from North American and International Grain; and Processing's earnings have risen 37% reflecting the new pasta and oat businesses acquired in the latter half of fiscal 2010.

Viterra's Australian operations contributed $37.0 million to consolidated EBITDA for the quarter, compared to $37.8 million a year earlier. Quarterly contributions were affected by higher demurrage expenses. A significant increase in shipments resulted in some logistical challenges during this period. In addition, last year's third quarter results included contributions from the International Grain group and atypical merchandising margins from domestic sales as commodity prices increased sharply during that period. On a year-to-date basis, the Australian operations contributed EBITDA of $218.2 million, an increase of 65% from the corresponding period a year earlier. The year-to-date results reflect the benefits of record grain volumes received and shipped over the last nine months, as well as a number of initiatives that have resulted in operational improvements and sustainable cost reductions.

For further information on segment performance, see Section 4.0 Segment Results.

Amortization for the three months ended July 31, 2011 was $50.7 million and consistent with the first two quarters of the year. For the first nine months of the fiscal year, amortization was $149.7 million compared to $137.9 million in fiscal 2010. The increase for the year-to-date period relates to the finalization of the purchase price allocations for Dakota Growers and 21st Century.

EBIT (see Non-GAAP Measures in Section 11.0) was $201.2 million for the quarter, compared to $132.9 million in the third quarter of fiscal 2010. For the first nine months EBIT was $441.7 million compared to $241.7 million in fiscal 2010.

Financing Expenses

(in thousands) Three Months

ended July 31,

2011 2010 Change

----------------------------------------------------------------------------

Interest on debt facilities $ 28,100 $ 21,400 $ 6,700

Interest accretion 824 373 451

Amortization of deferred financing costs 1,361 1,039 322

----------------------------------------------------------------------------

Financing Costs $ 30,285 $ 22,812 $ 7,473

Interest income (983) (2,470) 1,487

CWB carrying charge recovery (500) (371) (129)

----------------------------------------------------------------------------

Net financing costs for debt facilities $ 28,802 $ 19,971 $ 8,831

Net investment hedge - - -

One-time Refinancing costs - 24,880 (24,880)

----------------------------------------------------------------------------

Total financing and associated expenses $ 28,802 $ 44,851 (16,049)

----------------------------------------------------------------------------

Financing Expenses

(in thousands) Nine Months

ended July 31,

2011 2010 Change

----------------------------------------------------------------------------

Interest on debt facilities $ 89,898 $ 87,337 $ 2,561

Interest accretion 2,085 2,217 (132)

Amortization of deferred financing costs 4,019 5,545 (1,526)

----------------------------------------------------------------------------

Financing Costs $ 96,002 $ 95,099 $ 903

Interest income (2,956) (6,270) 3,314

CWB carrying charge recovery (1,420) (1,272) (148)

----------------------------------------------------------------------------

Net financing costs for debt facilities $ 91,626 $ 87,557 $ 4,069

Net investment hedge (4,989) - (4,989)

One-time Refinancing costs - 24,880 (24,880)

----------------------------------------------------------------------------

Total financing and associated expenses $ 86,637 $ 112,437 (25,800)

----------------------------------------------------------------------------

As noted in the above table, net financing costs associated with the Company's debt facilities were $28.8 million in the third quarter, compared to $20.0 million a year earlier. On a year to date basis, net financing costs for debt facilities were $91.6 million, compared to $87.6 million a year earlier. The increase in both the three and nine-month periods was due to higher levels of non-cash working capital, primarily driven by higher commodity prices.

Total financing and associated expenses for the nine months ended July 31, 2011 include the recognition of a non-cash gain on a net investment hedge relating to working capital funds advanced to the Australian operations. In fiscal 2010, total financing and associated expenses for the third quarter and year-to-date periods included one-time refinancing costs of $24.9 million related to debt restructuring.

Viterra recorded a net corporate income tax provision of $48.2 million for the third quarter, representing an effective tax rate of 28.1%. The Company's year-to-date effective tax rate was 27.6%.

Net earnings for the third quarter were $123.2 million or $0.33 per share, almost double the $63.5 million or $0.17 per share recorded in the same three-month period last year. For the first nine months of fiscal 2011, net earnings were $255.9 million or $0.69 per share, a significant increase from $92.6 million or $0.25 per share in the comparable period of fiscal 2010.

3.1 Select Quarterly Information

----------------------------------------------------------------------------

Select Quarterly Financial Information

For the quarters ended

(in millions - except per

share amounts) July 31 April 30, January 31, October 31,

2011 Q3(1) 2011 Q2(1) 2011 Q1(1) 2010 Q4(1)

----------------------------------------------------------------------------

Sales and other operating

revenues $ 3,554.1 $ 2,701.9 $ 2,470.5 $ 1,951.7

Net earnings (loss) $ 123.2 $ 33.1 $ 99.6 $ 52.7

Basic earnings per share $ 0.33 $ 0.09 $ 0.27 $ 0.14

Diluted earnings per

share $ 0.33 $ 0.09 $ 0.27 $ 0.14

----------------------------------------------------------------------------

----------------------------------------------------------------------------

Select Quarterly Financial Information

For the quarters ended

(in millions - except per

share amounts) July 31, April 30, January 31, October 31,

2010 Q3(1) 2010 Q2(1) 2010 Q1(1) 2009 Q4(2)

----------------------------------------------------------------------------

Sales and other operating

revenues $ 2,493.2 $ 2,048.1 $ 1,784.5 $ 1,417.1

Net earnings (loss) $ 63.5 $ 18.4 $ 10.7 $ (0.9)

Basic earnings per share $ 0.17 $ 0.05 $ 0.03 $ -

Diluted earnings per

share $ 0.17 $ 0.05 $ 0.03 $ -

----------------------------------------------------------------------------

(1) Includes results for Viterra's Australian operations.

(2) Includes results for Viterra's Australian operations from September 24,

2009 to October 31, 2009.

A discussion of the factors that cause seasonal variations by quarter is found in Sections 6.1 and 6.2 of the MD&A for the fiscal year ended October 31, 2010 and in Section 4.0 Segment Results below. These sections discuss, among other things, the trends and seasonality of the Company's three operating segments: Grain Handling and Marketing, Agri-products and Processing.

4.0 Segment Results

4.1 Grain Handling and Marketing

The Grain Handling and Marketing operations accumulate, store, transport and market grains, oilseeds, pulses and special crops. This business includes grain storage facilities and processing plants strategically located in the prime agricultural growing regions of North America and Australia. In its North American operations, the Company has 82 storage and handling facilities located throughout Western Canada, 11 special crop facilities located throughout Western Canada and the northern U.S., as well as seven port export terminals (including one joint venture facility and one leased facility) located in major port locations throughout Canada. In southern Australia, the Company has 108 storage and handling facilities, which work in conjunction with its eight wholly owned port export terminals. The International Grain group, through its sales offices, handles the merchandising of grains and oilseeds between origination and offshore destination customers. In addition, the International Grain group sources commodities from locations where Viterra has no accumulation and storage assets.

Seasonality

Receipts and subsequent shipments in any given fiscal year are dependent upon production levels and carry-over stocks from the prior year. Grain flows can fluctuate depending on global demand, crop size, prices of competing commodities, as well as other factors noted in the following discussion on volumes and shipments. In North America, grain shipments are fairly consistent from quarter to quarter, as are port terminal activities off the West Coast of Canada and at the Company's Port of Montreal facility. At Thunder Bay, shipments through the Company's port terminals end in late December, when the St. Lawrence Seaway closes for the winter months, and typically resume near the beginning of April.

In South Australia, the majority of grain flows into the system during the first quarter as this is the harvest period, which begins in October and continues through until the end of January. During the remaining quarters, the operations typically receive the last of the grower grain deliveries, with the exception of a small amount that remains on farm. Viterra owns and operates approximately 95% of South Australia's storage and all of its port terminal capacity. The grain that is delivered into the Company's grain storage and handling facilities is classified and blended in preparation for export. Viterra and other marketers then buy these grains and oilseeds and market them directly to destination customers. Shipping from the Company's port terminals typically commences in harvest and continues throughout the year. Income is derived from storage and handling fees including receivals and monthly carrying and out-turn (shipping) fees. Additional income is derived through handling and shipping of non-grain commodities year-round from select port terminals.

In addition, the Company's International Grain group earns merchandising and trading margins for commodities that it acquires from Viterra's origination assets as well as third parties and sells those commodities to destination customers around the world.

Industry Shipments

In the third quarter, western Canadian industry shipments of the six major grains were 8.3 million tonnes compared to 8.7 million tonnes during the corresponding period of 2010. For the nine months ended July 31, 2011, industry shipments of the six major grains were 24.0 million tonnes, about 6% lower than the 25.6 million tonnes shipped by this time last year. The variances reflect the smaller production from the 2010 fall harvest, which was approximately 15% lower than the previous year.

Total wheat export shipments out of Australia for the period from October 1, 2010 to June 30, 2011 totaled 14.0 million tonnes, an increase of 36% from the corresponding prior period a year earlier. South Australian wheat shipments in this period of 2011 were about 30% of the total, compared to about 15% of the total in the corresponding nine-month period of 2010.

Viterra's North American Volumes

Viterra's North American shipments for the three months ended July 31, 2011, were 4.2 million tonnes compared to 4.4 million tonnes in the third quarter of fiscal 2010. For the nine months ended July 31, 2011, the Company shipped 11.3 million tonnes, compared to 12.0 million tonnes a year earlier. Viterra's shipments of the six major grains in the third quarter were in line with Management's expectations given the crop size this year. Viterra's split between CWB grains and open market grain shipments for the third quarter and first nine months of fiscal 2011 was 50/50 and 46/54 respectively. This compares to a 52/48 split in the third quarter and a 50/50 split in the first nine months of last year.

Viterra's port terminal receipts for the third quarter were 2.9 million tonnes compared to 3.0 million tonnes in the third quarter of 2010. For the first nine months, port terminal receipts were 7.5 million tonnes versus 7.6 million tonnes in fiscal 2010. For the quarter and year-to-date periods, over 70% of these volumes moved to West Coast port terminals to support continued strong demand from Asian-Pacific countries.

Viterra's Australian Volumes

----------------------------------------------------------------------------

Viterra's Australian Volume Three Months Nine Months

(in thousands of tonnes) ended July 31, Better ended July 31, Better

2011 2010 (Worse) 2011 2010 (Worse)

----------------------------------------------------------------------------

Total shipments 2,270 1,689 581 6,257 3,549 2,708

Merchandised volumes

South Australia 667 390 277 2,013 1,050 963

Rest of Australia 720 1,210 (490) 2,441 3,450 (1,009)

----------------------------------------------------------------------------

Total merchandised volumes 1,387 1,600 (213) 4,454 4,500 (46)

----------------------------------------------------------------------------

----------------------------------------------------------------------------

As of the end of the second quarter, the vast majority of the available crop in South Australia was received into Viterra's system. Aggregate receipts into the south Australian system for the first nine months of fiscal 2011 were 8.5 million tonnes, compared to 6.2 million tonnes in fiscal 2010.

From a shipments perspective, the strength of the Company's shipping program continued, with a total of 2.3 million tonnes moving through its south Australian port system in the third quarter, compared to 1.7 million tonnes in fiscal 2010. On a year-to-date basis, the Company shipped a record 6.3 million tonnes, compared to 3.5 million tonnes in the corresponding period of fiscal 2010. High commodity prices and strong demand have motivated industry participants to utilize Viterra's system to ship a significant amount of grain this year.

During the first nine months of fiscal 2011, Viterra purchased for its own account 32% of the grain shipped through its south Australian system. There are a large number of marketers competing for south Australian growers' grain and, of this number, more than 10 of them were responsible for the remaining 68% of grain shipped from the Company's port system in South Australia.

Viterra also originated and merchandised 0.7 million tonnes of grains and oilseeds from third-party facilities throughout the rest of Australia during the quarter. On a year-to-date basis, Viterra has merchandised 2.4 million tonnes from the rest of Australia, which is down from the prior year due to a smaller crop in Western Australia and logistical issues caused by wet weather and availability of freight in the eastern states.

Operating Results

Grain Handling and Marketing

(in thousands - except margins) Three Months

ended July 31, Better

2011 2010 (Worse)

----------------------------------------------------------------------------

Gross profit and net revenues from

services $ 207,213 $ 181,748 $ 25,465

Operating, general and

administrative expenses (102,976) (80,895) (22,081)

----------------------------------------------------------------------------

EBITDA (1) 104,237 100,853 3,384

Amortization (25,310) (37,259) 11,949

----------------------------------------------------------------------------

EBIT (1) $ 78,927 $ 63,594 $ 15,333

----------------------------------------------------------------------------

----------------------------------------------------------------------------

Total sales and other operating

revenues $ 2,186,810 $ 1,469,073 $ 717,737

North American Industry Statistics

(tonnes)

Canadian Industry Receipts - six

major grains 8,503 8,899 (396)

Canadian Industry Shipments - six

major grains 8,331 8,738 (407)

Canadian Industry Terminal

Receipts 6,607 6,676 (69)

Viterra - North American

Operations (tonnes)

Elevator receipts 4,135 4,254 (119)

Elevator shipments 4,156 4,382 (226)

Port terminal receipts 2,906 2,959 (53)

Viterra - Australian Operations

(tonnes)

Shipments 2,270 1,689 581

Receivals 20 6 14

Consolidated Global Pipeline

(tonnes)

North American shipments 4,156 4,382 (226)

Australian receivals 20 6 14

----------------------------------------------------------------------------

Total pipeline 4,176 4,388 (212)

Consolidated pipeline margin (per N/A N/A N/A

tonne)

Grain Handling and Marketing

(in thousands - except margins) Nine Months

ended July 31, Better

2011 2010 (Worse)

----------------------------------------------------------------------------

Gross profit and net revenues

from services $ 719,826 $ 537,211 $ 182,615

Operating, general and

administrative expenses (295,745) (253,090) (42,655)

----------------------------------------------------------------------------

EBITDA (1) 424,081 284,121 139,960

Amortization (76,596) (72,884) (3,712)

----------------------------------------------------------------------------

EBIT (1) $ 347,485 $ 211,237 $ 136,248

----------------------------------------------------------------------------

----------------------------------------------------------------------------

Total sales and other operating

revenues $ 6,174,685 $ 4,230,374 $ 1,944,311

North American Industry

Statistics (tonnes)

Canadian Industry Receipts - six

major grains 24,420 25,887 (1,467)

Canadian Industry Shipments - six

major grains 24,033 25,615 (1,582)

Canadian Industry Terminal

Receipts 17,772 18,267 (495)

Viterra - North American

Operations (tonnes)

Elevator receipts 11,111 11,656 (545)

Elevator shipments 11,282 11,993 (711)

Port terminal receipts 7,483 7,648 (165)

Viterra - Australian Operations

(tonnes)

Shipments 6,257 3,549 2,708

Receivals 8,529 6,206 2,323

Consolidated Global Pipeline

(tonnes)

North American shipments 11,282 11,993 (711)

Australian receivals 8,529 6,206 2,323

----------------------------------------------------------------------------

Total pipeline 19,811 18,199 1,612

Consolidated pipeline margin (per

tonne) $ 36.33 $ 29.52 $ 6.82

----------------------------------------------------------------------------

(1) See Non-GAAP Measures in Section 11.0

Gross profit for the Grain Handling and Marketing segment totaled $207.2 million in the third quarter compared to $181.7 million in the comparable period of fiscal 2010. The strong third quarter results brought gross profit to $719.8 million for the first nine months of fiscal 2011, compared to $537.2 million in the previous year. A significant portion of both the third quarter and year-to-date increases were due to the performance of Viterra's Australian operations. South Australia harvested a large crop this year, which resulted in significant volumes moving into Viterra's system in the first quarter and record shipments year to date.

On a consolidated basis, the year-to-date pipeline margin per tonne was $36.33 compared to $29.52 last year due to stronger margins in both the North American and Australian operations as well as the incremental contributions from the International Grain group, which was not yet fully established in the comparable period of the preceding year. North American margins have benefited from increased merchandising and blending opportunities, additional pulse sales and increased earnings throughout the terminal operations, which includes the Company's interest in the Prince Rupert port terminal. In South Australia, margins increased due to high volumes, increased storage and handling fees, solid blending contributions and lower costs. Viterra has implemented a number of initiatives throughout the region that have not only lowered its costs per tonne but have resulted in sustainable cost reductions throughout the operation. The Company believes its fiscal year 2011 global pipeline margin will come in at the higher end of its guidance range of $33 to $36 per tonne.

OG&A expenses for the Grain Handling and Marketing segment were $103.0 million in the third quarter of fiscal 2011 compared to $80.9 million in the third quarter of last year. This brings OG&A expenses for the first nine months to $295.7 million compared to $253.1 million a year earlier. The increase primarily relates to additional seasonal labour hired in Australia during the first quarter to handle the record crop, a full complement of costs for the International Grain group, which was not fully established by this time last year, and costs associated with new operations added during the quarter.

The Grain Handling and Marketing segment generated $104.2 million in EBITDA for the quarter compared to $100.9 million in the third quarter of last year. The third quarter results include $40.9 million in contributions from the Australian grain handling and marketing operations (2010 - $42.9 million). Australia's quarterly contributions were affected by higher demurrage expenses as a significant increase in shipments resulted in some logistical challenges during this period. In addition, Australia's third quarter results last year included contributions from the International Grain group and atypical merchandising margins from domestic sales as commodity prices increased sharply during that period. On a year-to-date basis, Grain Handling and Marketing's EBITDA was $424.1 million compared to $284.1 million a year earlier. The significant year-over-year increase in EBITDA is attributable to Viterra's Australian operations that generated $220.7 million (2010 - $129.0 million) for the first nine months of the fiscal year, along with strong results from the North American operation.

The International Grain group generated EBITDA of $9.1 million in the quarter, bringing its year-to-date contribution to $40.5 million. The positive third quarter and year-to-date contributions are a result of this group utilizing the Company's integrated grain pipeline model and prudent risk management strategies to successfully manage through adverse geopolitical and macro events. In the corresponding periods of fiscal 2010, the International Grain group was not fully established and its contributions were included within North American and Australian results. This group's activities are driven by opportunities that arise in the market and therefore results can fluctuate quarter to quarter depending upon varying market dynamics.

EBIT for the segment was $78.9 million in the third quarter of fiscal 2011, compared to $63.6 million in the third quarter of fiscal 2010. On a year-to-date basis, EBIT was $347.5 million compared to $211.2 million a year earlier.

Outlook

The Company has increased its estimate for fiscal 2011 Canadian Grain Commission ("CGC") receipts for the six major grains in Western Canada to approximately 32.0 to 33.0 million tonnes, from its previous range of 31.0 to 32.0 million tonnes. As expected, producers have drawn down on-farm carryout stocks.

Across the Canadian Prairies, harvest is well underway and higher than average yields are expected from this year's crop due to favourable weather for much of the growing season. In its August 24, 2011 field crop reporting series release, Statistics Canada is predicting that western Canadian production of the six major grains will be 47.5 million tonnes, with an additional 2.5 million tonnes of lentils and other crops expected. This would represent an increase of 5.6% from the 45.0 million tonnes produced in the 2010 harvest, but a decrease from the 5-year historical average production of about 50.0 million tonnes. The quality of the crop in Western Canada looks promising, but is dependent on favourable harvest weather for the next couple of months.

For fiscal 2012, assuming production estimates hold, Viterra anticipates CGC receipts for the six major grains in Western Canada to be in the 30.0 to 32.0 million tonne range, which compares to the 32.0 million tonnes that is typically available.

Viterra remains optimistic that the industry will see relatively strong volumes through the remaining portion of the fiscal year and into fiscal 2012, particularly if weather conditions remain favorable into the fall. Strong demand and robust prices are expected to motivate farmers to actively market their open market grains through the next crop year. The CWB is forecasting an export target of 18.0 million tonnes of wheat and barley out of Canada for the upcoming crop year compared to 15.8 million tonnes for the 2011 crop year.

For Viterra's South Australia grain handling operations, the Company expects shipments to remain strong into the last quarter of the fiscal year given the significant quantity of grain previously received into the system, the favourable commodity price environment and strong demand. To complement the 8.5 million tonnes received into the Company's system during the first nine months of fiscal 2011, there were approximately 1.2 million tonnes of carry-in stocks from fiscal 2010. The Company currently estimates carry-over stocks into fiscal year 2012 for the Company's Australian system to range between 1.7 and 2.0 million tonnes, up from last year due to the record crop produced in the state.

In South Australia, seeding finished in late June and good growing conditions exist throughout the majority of the state. The Australian Bureau of Agriculture and Resources Economics and Sciences ("ABARES") is predicting that the current crop will produce 7.6 million tonnes. This represents a 21% increase from the 10-year average for the state, but a decrease from the record 9.8 million tonnes produced last harvest. Based on current growing conditions, the Company believes there may be upside to ABARES's estimate. Crop quality in the state is good at this time. Approximately 80% of the crop is currently expected to be wheat and barley.

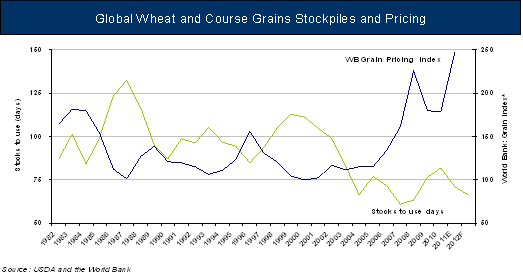

The last few months have seen upward revisions in global production and export volume forecasts, particularly for the Black Sea region where growing conditions have vastly improved since last season's drought. Fundamentals for agri-commodity pricing and trade remain strong. The United States Department of Agriculture ("USDA") is predicting that, despite significant volumes from upcoming harvests in several key growing regions, by the end of July 2012, global stocks-to-use days for wheat and coarse grains are to be below 70 days, a sharp reduction from 82 days in 2010. Pricing trends are driven largely by global stockpiles of essential grains.

To view the Global Wheat and Course Grains Stockpiles and Pricing graph, please visit the following link: http://media3.marketwire.com/docs/907vt1.jpg.

{kind=link}

From a regulatory perspective, in Canada the majority Government announced in May that it intends to provide western Canadian producers with marketing choice for wheat, durum and barley, which will eliminate the CWB's monopoly control. The federal government has also indicated it expects measures to be taken to allow for a redefined CWB to continue functioning as a voluntary marketing agency. To this end, the federal government has created an industry working group to address transitional items such as:

- access to elevators, rail and ports;

- access to producer cars;

- organizing and funding market development and research activities for wheat and barley;

- delivery of an advance payment program; and

- any other business related transition issues concerning the grain marketing and transportation systems as well as the supply chains.

The industry working group is consulting with interested parties, including the members of the Western Grain Elevator Association. A report is expected in the fourth quarter and will be submitted to the Minister of Agriculture. It is still early in the process and Viterra will await further details on how this new market will function before quantifying the benefits to the Company's operations. It is anticipated that legislation to repeal the CWB Act, along with associated transitional measures, will be introduced during the fall session of Parliament, with these legislative changes taking effect as of August 2012.

Viterra is supportive of the Government's direction and is confident in the Company's ability to operate effectively in an open wheat and barley market, to serve the needs of farmers, other industry participants, and the redefined CWB. Viterra believes it has the necessary expertise today to provide these additional services to the industry. The Company is committed to working with the Government, industry, and the CWB, to ensure the Canadian grain industry remains a vibrant and competitive source for agricultural products. Viterra continues to participate in the process to promote an orderly transition with positive, sustainable change for the benefit of the western Canadian agricultural industry.

In order for companies such as Viterra to export bulk wheat from Australia, they must retain accreditation from Wheat Exports Australia ("WEA") under Australian law. Viterra currently holds accreditation until September 30, 2011 and is in the process of attaining renewal from WEA for the period October 1, 2011 until September 30, 2014. Companies that own or operate port terminals are required by WEA to also have in place an access undertaking approved by the Australian Competition and Consumer Commission ("ACCC"), relating to the provision of access to its port terminal services to other accredited wheat exporters. The current undertaking expires on September 30, 2011 for all operators.

In December 2010, Viterra lodged a proposed access undertaking for the period October 1, 2011 to September 30, 2014. The ACCC has not yet made a final decision on whether to accept the proposed undertaking. However, as outlined in its draft decision on August 11, 2011, the ACCC's preliminary view is that an auction system would address its main areas of concern. As part of its regulatory approval process, the ACCC is engaging in public consultation on its draft decision. Viterra continues to work with the ACCC to ensure a timely decision is made and has issued a revised undertaking, which includes the implementation from mid-2012 of an auction system for managing the allocation of bookings on the shipping stem. Viterra remains confident that it will gain approval for its revised undertaking by September 30, 2011, in order to attain renewal of its bulk wheat export accreditation from WEA as of October 1, 2011.

In Australia, Viterra is currently participating in two separate parliamentary inquiries relating to the grain industry, in both the House of Assembly of the Parliament of South Australia (state) and the Senate of the Australian Parliament (federal). The state inquiry is focused on the efficiency of grain handling operations in South Australia, while the Federal inquiry is centered on grain export capabilities within the country. As a major stakeholder in the Australian grain industry, Viterra is committed to working with governments and industry and has appeared before the inquiries and provided public written submissions.

In South Australia, Viterra has been pro-actively implementing enhancements to its service delivery model as a result of a post-harvest review that the Company conducted after the January 2011 harvest. A number of issues arose during that time given the record crop production, coupled with widespread rain during harvest. Viterra established a Post Harvest Review working group consisting of industry, government, senior company employees, and farm group representatives and launched a full performance review. Viterra released the recommendations of the review in June and is implementing enhancements in the areas of grain grading, logistics, infrastructure investment, safety and skills development.

4.2 Agri-products

North America

Viterra operates a network of 261 agri-products retail locations throughout Western Canada, which are geographically dispersed throughout the growing regions of the Canadian Prairies. Retail locations offer fertilizer, crop protection products, seed and equipment to growers. The Company's operations in Western Canada represent an approximate 34% share of the market.

For fertilizer, Viterra has a 34% investment in CFL, a nitrogen fertilizer manufacturing plant in Medicine Hat, Alberta. The Company is entitled to receive 34% of approximately 1.4 million tonnes of merchantable product, split between granular urea and anhydrous ammonia. The Company also buys and sells fertilizer from third-party manufacturers.

Viterra offers a comprehensive line of crop protection and seed products through its western Canadian retail network. The Company offers a line of 22 private label crop protection products as well as third-party products in conjunction with leading manufacturers. For seed, the Company has a network of research facilities and is involved in various collaborative agreements, which result in an extensive offering of proprietary and exclusive varieties, as well as third-party varieties.

The Agri-products segment includes contributions from the Company's financial products business. As an agent for a Canadian chartered bank, Viterra FinancialTM, extends unsecured and secured trade credit at competitive rates to the Company's agri-products and feed products customers.

Australia

In Australia, Viterra operates 16 agri-products depots and six fertilizer warehouses in South Australia and Victoria, through which it sells and distributes seed, fertilizer and crop protection products.

Viterra also operates a domestic wool network extending across the agricultural areas of Western Australia, South Australia and Victoria and is the largest buyer of Australian wool, exporting to key international markets such as China, India and Italy. Viterra recently expanded its wool export business to New Zealand.

Seasonality

North America

Retail sales of agri-products are seasonal and correlate directly to the life cycle of the crop. About 60% of Viterra's annual agri-products sales are typically generated during the third quarter as producers purchase crop inputs such as seed, fertilizer and crop protection products. Prior to seeding, Viterra receives prepayments from farm customers who want to order a portion of their agri-product requirements for the spring. Actual sales are recorded when product is delivered. Prepayments, seed bookings, and discussions with customers provide Viterra with an early indication of seeding intentions.

Australia

In Australia, most crop inputs are purchased during the seeding period, which begins in April and extends into June. Additional sales occur throughout the growing season to support crop development.

Operating Results

Agri-products

(in thousands - except margins) Three Months

ended July 31, Better

2011 2010 (Worse)

----------------------------------------------------------------------------

Gross profit and net revenues from

services $ 229,184 $ 167,754 $ 61,430

Operating, general and administrative

expenses (67,282) (62,004) (5,278)

----------------------------------------------------------------------------

EBITDA (1) 161,902 105,750 56,152

Amortization (11,381) (11,832) 451

----------------------------------------------------------------------------

EBIT (1) $ 150,521 $ 93,918 $ 56,603

----------------------------------------------------------------------------

----------------------------------------------------------------------------

Operating Highlights

Sales and other operating revenues $ 1,134,746 $ 817,887 $ 316,859

Fertilizer 535,503 342,914 192,589

Crop Protection 317,664 296,978 20,686

Seed 120,321 82,306 38,015

Wool 115,352 58,462 56,890

Equipment sales and other revenue 39,753 31,575 8,178

Financial Products 6,153 5,652 501

Fertilizer volume (tonnes) 876 699 177

Fertilizer margin (per tonne) $ 143.92 $ 118.56 $ 25.36

----------------------------------------------------------------------------

----------------------------------------------------------------------------

Agri-products

(in thousands - except margins) Nine Months

ended July 31, Better

2011 2010 (Worse)

----------------------------------------------------------------------------

Gross profit and net revenues from

services $ 349,304 $ 277,329 $ 71,975

Operating, general and administrative

expenses (157,134) (153,523) (3,611)

----------------------------------------------------------------------------

EBITDA (1) 192,170 123,806 68,364

Amortization (30,189) (34,388) 4,199

----------------------------------------------------------------------------

EBIT (1) $ 161,981 $ 89,418 $ 72,563

----------------------------------------------------------------------------

----------------------------------------------------------------------------

Operating Highlights

Sales and other operating revenues $ 1,861,058 $ 1,471,475 $ 389,583

Fertilizer 864,892 627,629 237,263

Crop Protection 340,686 338,787 1,899

Seed 233,064 205,934 27,130

Wool 339,821 215,929 123,892

Equipment sales and other revenue 68,363 65,596 2,767

Financial Products 14,232 17,600 (3,368)

Fertilizer volume (tonnes) 1,528 1,380 148

Fertilizer margin (per tonne) $ 126.46 $ 93.97 $ 32.49

----------------------------------------------------------------------------

(1) See Non-GAAP Measures in Section 11.0

Sales and other operating revenues ("sales" or "revenues") for the Agri-products segment rose significantly during the third quarter of fiscal 2011 to $1,134.7 million versus $817.9 million for the same three-month period last year due to strong fertilizer pricing and sales volumes in Western Canada as well as higher wool sales in Australia. In addition, late seeding across the Canadian Prairies moved a portion of the Company's agri-product sales from the second quarter into the third quarter. On a year-to-date basis, Agri-products segment sales were up $389.6 million over the prior year due to higher volumes and pricing for both fertilizer and wool.

---------------------------------------------------------------------------- Consolidated Fertilizer Volumes by Quarter (in thousands of tonnes) For the quarter ended Fiscal year 31-Jan 30-Apr 31-Jul 31-Oct Total ---------------------------------------------------------------------------- 2011 373 279 876 - 1,528 2010 310 371 699 370 1,750 ----------------------------------------------------------------------------

Over the last nine months ended July 31, fertilizer demand has been strong due to high commodity prices and increased nutrient requirements caused by excess moisture in 2010 and 2011, which encouraged farmers to maximize their fertilizer applications. As a result, North American fertilizer sales volumes increased 26% for the quarter and 10% year-to-date relative to the corresponding periods in fiscal 2010. Similar fundamentals have also driven strong Australian fertilizer demand, with sales increasing 20% to 55,000 tonnes for the third quarter compared to 46,000 tonnes a year earlier, bringing its year-to-date volumes to 106,000 tonnes versus 89,000 tonnes in fiscal 2010.

Crop protection product sales were $317.7 million in the third quarter, an increase of 7% from the corresponding period in the previous year. This increase was primarily attributable to a shift in sales from the second quarter following the delayed seeding in North America due to cool and wet weather across the Canadian Prairies. On a year-to-date basis, crop protection product sales were $340.7 million, on par with the previous year as devalued herbicide prices were offset by increased sales volumes due to higher seeded acreage. Statistics Canada estimates that about 18.5 million acres of canola were planted in Western Canada this year, compared to 16.7 million acres a year earlier. This also increased seed sales 46% and 13% respectively for the third quarter and first nine months of the fiscal year. Third quarter seed sales also benefited from late seeding in North America that pushed sales forward.

According to Statistics Canada the total seeded area for Western Canada this year is estimated at 54.9 million acres. This compares to the 10-year historical average of approximately 60.0 million acres in the region.

Wool sales increased 97% in the third quarter and 57% in the first nine months of fiscal 2011 relative to the corresponding periods a year earlier. These increases resulted from an expansion of domestic market share for these operations as well as strong export demand from key markets such as India and China.

Gross profit increased $61.4 million to $229.2 million in the third quarter, compared to $167.8 million in the corresponding period of fiscal 2010. On a year-to-date basis, gross profit rose to $349.3 million, from the $277.3 million generated in the corresponding period of fiscal 2010. These increases relate primarily to higher fertilizer sales volumes and consolidated margins that have risen to $126.46 per tonne in the first nine months of fiscal 2011 compared to $93.97 per tonne a year earlier. Higher average selling prices and lower natural gas costs on manufactured product have generated this increase.

For fiscal 2011, the Company expects its fertilizer margin to range between $110 to $130 per tonne, an increase from previous guidance of $100 to $120 per tonne. Quarterly margins per tonne can vary outside of this range due to product mix and timing of purchases for manufactured versus resale tonnes. Maintaining the guidance range of $110 to $130 per tonne, beyond fiscal 2011, will be dependent upon North American commodity markets, weather conditions and crop mix.

OG&A expenses for the third quarter were $67.3 million compared to $62.0 million in the prior year. The majority of the increase is attributable to the timing of expenses as late spring seeding moved a portion of the agri-products business from the second quarter to the third quarter as well as higher costs related to the Company's short-term incentive programs. On a year-to-date basis OG&A expenses were $157.1 million, compared to $153.5 million a year earlier.