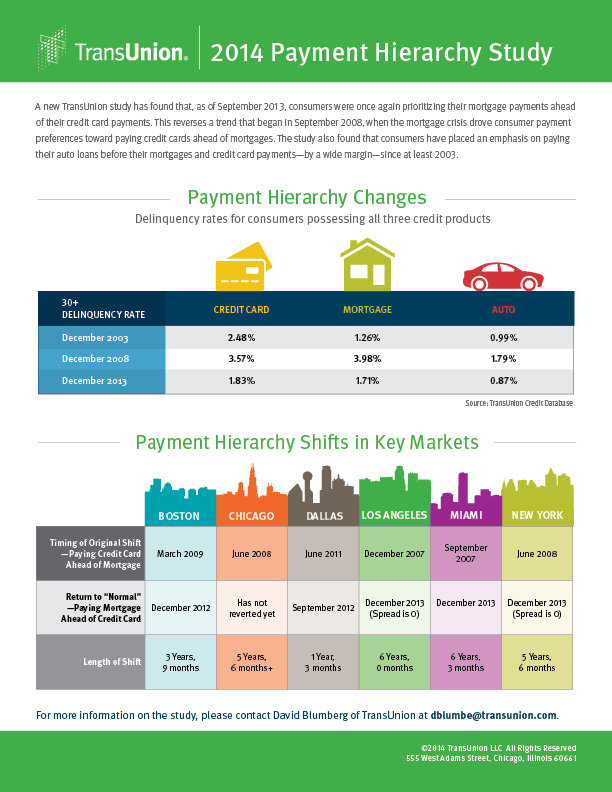

CHICAGO, IL--(Marketwired - Mar 19, 2014) - A new TransUnion study has found that, as of September 2013, consumers were once again prioritizing their mortgage payments ahead of their credit card payments. This reverses a trend that began in September 2008, when the mortgage crisis drove consumer payment preferences toward paying credit cards ahead of mortgages. The study also found that consumers have placed an emphasis on paying their auto loans before their mortgages and credit card payments -- by a wide margin -- since at least 2003.

"One of the biggest impacts of the Great Recession to the credit system was its influence on consumer payment patterns," said Ezra Becker, co-author of the study and vice president of research and consulting for TransUnion. "As unemployment rose and home prices cratered, increasingly more consumers were faced with financial constraints and had to make difficult choices -- and many chose to value their credit card relationships above their mortgages. This was a measurable result of the economic environment, wherein many consumers were underwater on their mortgages and at the same time needed the liquidity afforded by credit cards to make ends meet."

| 30-Day Delinquency Rates for Consumers Possessing Auto Loans, Credit Cards and Mortgage Loans (Delinquency rates only reflect consumers with all three credit products) |

||||||

| Year | Mortgage | Credit Card | Auto Loan | |||

| SEP 04 | 1.26% | 2.25% | 0.95% | |||

| SEP 05 | 1.24% | 2.24% | 0.89% | |||

| SEP 06 | 1.32% | 2.41% | 0.97% | |||

| SEP 07 | 1.71% | 2.51% | 1.01% | |||

| SEP 08 | 3.32% | 3.29% | 1.65% | |||

| SEP 09 | 4.92% | 3.99% | 1.62% | |||

| SEP 10 | 3.67% | 2.62% | 1.33% | |||

| SEP 11 | 2.94% | 2.24% | 1.04% | |||

| SEP 12 | 2.42% | 1.81% | 1.04% | |||

| SEP 13 | 1.79% | 1.86% | 0.89% | |||

| DEC 13 | 1.71% | 1.83% | 0.87% | |||

To determine how much of an impact housing prices had on the rate of payment of credit cards versus mortgages, TransUnion looked at the delinquency spread between mortgages and credit cards over the past decade, and compared that spread to the Standard and Poor's Case-Shiller 20-City Home Price Index (HPI). For instance, if the 30-day credit card delinquency rate was 1.50% and the 30-day mortgage delinquency rate was 2.25% at a given point in time, then there would be a 0.75% spread between the two variables.

"This was an especially enlightening part of the study, because we found that home price appreciation and depreciation can impact mortgage and credit card payment patterns quite differently, depending on whether consumers consider the environment 'normal'," said Toni Guitart, co-author of the study and director of research and consulting in TransUnion's financial services business unit. "While we saw massive home value appreciation between 2003 and 2006, the spread between credit card delinquency and mortgage delinquency remained effectively the same; that is, the home value appreciation, while big, was expected and therefore not a driver of change. However, once home values experienced major declines in 2007 and 2008, the delinquency spread narrowed to the point where more people were opting to pay their credit cards before their mortgages -- something that was unimaginable just a few years prior."

Through all of 2006 the HPI was near its all-time high at just above 200, and the 30-day delinquency spread between credit cards and mortgages maintained a stable, negative level. For instance, in June 2006 the spread was -1.18%, which was derived by subtracting the credit card delinquency rate of 2.47% from the mortgage delinquency rate of 1.29%. The HPI was 206.31 at that time.

Over the following two years, the HPI dropped 21% to 161.82 by September 2008. This in part drove increasingly more consumers to pay their credit cards before their mortgages, causing the delinquency spread to move 122 basis points from -1.18% in June 2006 to +0.04% in September 2008. This new payment hierarchy trend -- with more consumers choosing to pay their credit cards and go delinquent on their mortgages -- continued for five years, with a peak delinquency spread in June 2010 of +1.18% when the HPI was 147.22. "When the market dynamic is what people expect, i.e., home values are increasing and unemployment is under control, then the payment hierarchy is stable. It's when an unexpected shock hits the market, like home value depreciation or major increases in unemployment, that the payment hierarchy is subject to change, as consumers reassess which loan relationships are more important to them at that time," continued Becker.

Major variances were found across the country, with cities such as Los Angeles -- which was greatly impacted by the mortgage crisis -- experiencing much different consumer payment patterns than cities such as Dallas, which had a more stable housing situation.

The credit card-mortgage delinquency spread "flipped" in December 2007 in Los Angeles, meaning that was the point at which more consumers in the study were going delinquent on their mortgages than on their credit cards. This pattern continued through the end of the study in December 2013, with the delinquency spread essentially remaining the same. In contrast, Dallas experienced the reversal in payment patterns much later -- beginning in June 2011 -- with that reversal only lasting through September 2012.

| Payment Hierarchy Shifts in Key Markets | ||||||

Market |

Timing of Original Shift - Paying Credit Card Ahead of Mortgage | Return to "Normal" - Paying Mortgage Ahead of Credit Card | Length of Shift |

|||

| Boston | MAR 2009 | DEC 2012 | 3 Years, 9 Months | |||

| Chicago | JUNE 2008 | (Has not reverted yet) | 5 Years, 6 Months+ | |||

| Dallas | JUNE 2011 | SEPT 2012 | 1 Year, 3 Months | |||

| Los Angeles | DEC 2007 | DEC 2013 (Spread is 0) | 6 Years, 0 Months | |||

| Miami | SEPT 2007 | DEC 2013 | 6 Years, 3 Months | |||

| New York | JUNE 2008 | DEC 2013 (Spread is 0) | 5 Years, 6 Months | |||

"It's been well documented that the Great Recession impacted different areas of the country to varying degrees," said Becker. "While unemployment generally went up throughout most of the country, some areas saw more job losses than others. Markets that experienced extreme housing value increases and declines also saw the biggest shifts in payment dynamics. As unemployment gradually improves and housing prices recover, we expect every major metropolitan city will revert to the traditional payment hierarchy."

About the Study

The study was completed using a series of monthly cohorts of anonymous consumer information from December 2002 through December 2012. Each cohort was composed of consumers who had at least one mortgage, auto loan and credit card open and in good standing as of the cohort definition month. The credit performance of each consumer was evaluated 12 months later using a 30 days past due or worse definition of delinquency -- thus the performance data span December 2003 through December 2013. Each monthly sample included approximately 2.5 million consumers.

About TransUnion

As a global leader in credit and information management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering comprehensive data and advanced analytics and decisioning. For consumers, TransUnion provides the tools, resources and education to help them manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion reaches businesses and consumers in 33 countries around the world on five continents. www.transunion.com/business

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail

Telephone 312 972 6646